Watsco ($WSO): The Beauty of a Virtuous Cycle

Introduction

I’ve recently asked for help in Twitter to find companies carrying out consolidation or roll-up processes. I’ve received a lot of ideas (that were gathered in this article) but one of the most repeated companies was Watsco (WSO). I had already heard many positive comments about this company before but I’ve never decided to analyze it. After the overwhelming mentions, I think now it is the time. Let’s start from the beginning.

WSO was incorporated in Florida in 1956 and started as a manufacturer of parts, components and tools used in the air conditioning, heating and refrigeration equipment (HVAC/R) industry, growing slowly to reach $25m in revenues by 1988. In 1989 the Company decided to shift from manufacturing to distribution and this movement changed everything. In 1989 it earned $64m in revenues and since then it have increased almost 100-fold to more than $6 billion, becoming the largest distributor in the HVAC/R distribution industry in North America. Nowadays WSO operates more than 670 locations in 42 US States, Canada, Mexico, and Puerto Rico with additional operations on an export basis to portions of Latin America and the Caribbean.

WSO is a one-stop-shop for the contractors: they don’t just sell equipment, but also they take care of all the supplies needed to complete the whole installation. This means basically providing everything else that goes into the house other than just the systems themselves such as ductwork, copper tubing or insulation products (which means also bigger tickets and higher margins).

Business model

WSO’s business model reminds me a lot of Pool Corporation’s one. WSO has also been able to position itself as some sort of hub within the supply chain, playing a prominent role that is increasing its importance as the Company grows. The beauty of this model lays in its capacity, within a fragmented supply chain, of making the distribution process much more efficient for all the stakeholders, helping manufacturers and contractors to sell their products/services and providing all the players in the sector with many incentives to work with the Company:

The reason for this model to thrive is the multiple advantages that WSO provides to its suppliers and customers, and the incentives that other independent distributors have to join its network:

With regard to OEMs/suppliers:

WSO is able to provide immediate access to a nationwide network of branches. The HVAC industry is very local and smaller distributors usually operate with few locations and within limited geographic areas, and cannot provide WSO’s capillarity of branches and final customer reach.

WSO saves OEMs/suppliers the costs and complexity of maintaining and managing a distribution business.

WSO is capable of carrying out large purchases, making for manufactures easier to manage their supply chain and reduce transportation costs thanks to freight consolidation.

In order to reduce cost and shorten lead times for their customers, a large distributor like WSO can warehouse significant volumes of products throughout the year, reducing inventory management risk and costs for manufactures.

WSO helps manufacturers to deal with final customers (technical support, warranties, rebates, training, queries, etc.), avoiding them many burdensome tasks and saving costs.

WSO is able to provide OEMs/suppliers with huge amounts of customer data that can be leveraged with advanced analytics

With regard to customers (contractors/technicians):

WSO provides a one-stop shopping experience thanks to its extensive product assortment, while smaller independent distributors have historically offered a narrow range of products requiring contractors to source their needs from more than one distributor in a local market. This diversity of brands and products is one of the most relevant WSO’s competitive advantages, making easier for contractors to serve its final customers with different price points and in any economic environment, and providing a more successful shopping experience compared to manufacturers’ direct sales channels, that are usually restricted to sale just their own equipment regardless of the best solution.

The capillarity of WSO’s location network is hard to match and it provides with the most convenient, cheapest and fastest service for contractors that usually need everything fast.

WSO’s vendor and supplier relationships imply many exclusive distributions contracts, making contractors rather difficult to access specific products other way.

WSO provides technology and many resources to its customers in order to make their businesses much more efficient and increase their productivity (e.g. mobile apps, ecommerce platforms, order fulfillment functionality and supply chain optimization). WSO promotes the growth of its customers’ businesses following pretty simple but powerful motto: “when our customers win, we win”.

WSO is able to get vendors rebates and purchase discounts and offer better conditions thanks to its scale (i.e. contractors can obtain better conditions than going directly to the manufacturer).

WSO can extend credit and favorable payment terms to its contractors to purchase goods and pay them later.

With regard to independent distributors (potential acquisition targets):

WSO provides capital and resources for business leaders to accelerate growth and develop scale in their businesses.

WSO guarantees access to favorable vendor relationships and better conditions. Due to its scale, WSO is able to get specific conditions that are no available for independent distributors.

WSO also provides access to exclusive OEM’s contracts. There are many exclusive agreements within the industry and independent distributors are frequently banned for selling specific products.

WSO provides acquired distributors with technology and digital capabilities that will be rather difficult for them to get outside the network (over 200 people working on technology initiatives). WSO scale allows the company to deploy many resources on technology innovations and that situation increases the pressure over smaller players.

WSO allows acquired businesses to keep running as separate businesses, with a completely decentralized approach: keeping intact the management team, the employee base, the brand and the day-to-day decision making process. WSO acquisition strategy is based on acquiring well-run companies and let their own teams to keep building the company.

WSO provides equity consideration and equity incentives. In order to reinforce this culture of trust, consideration paid by WSO for its acquisitions is composed of a mix of cash and shares, with the idea of aligning as much as possible corporate and local teams.

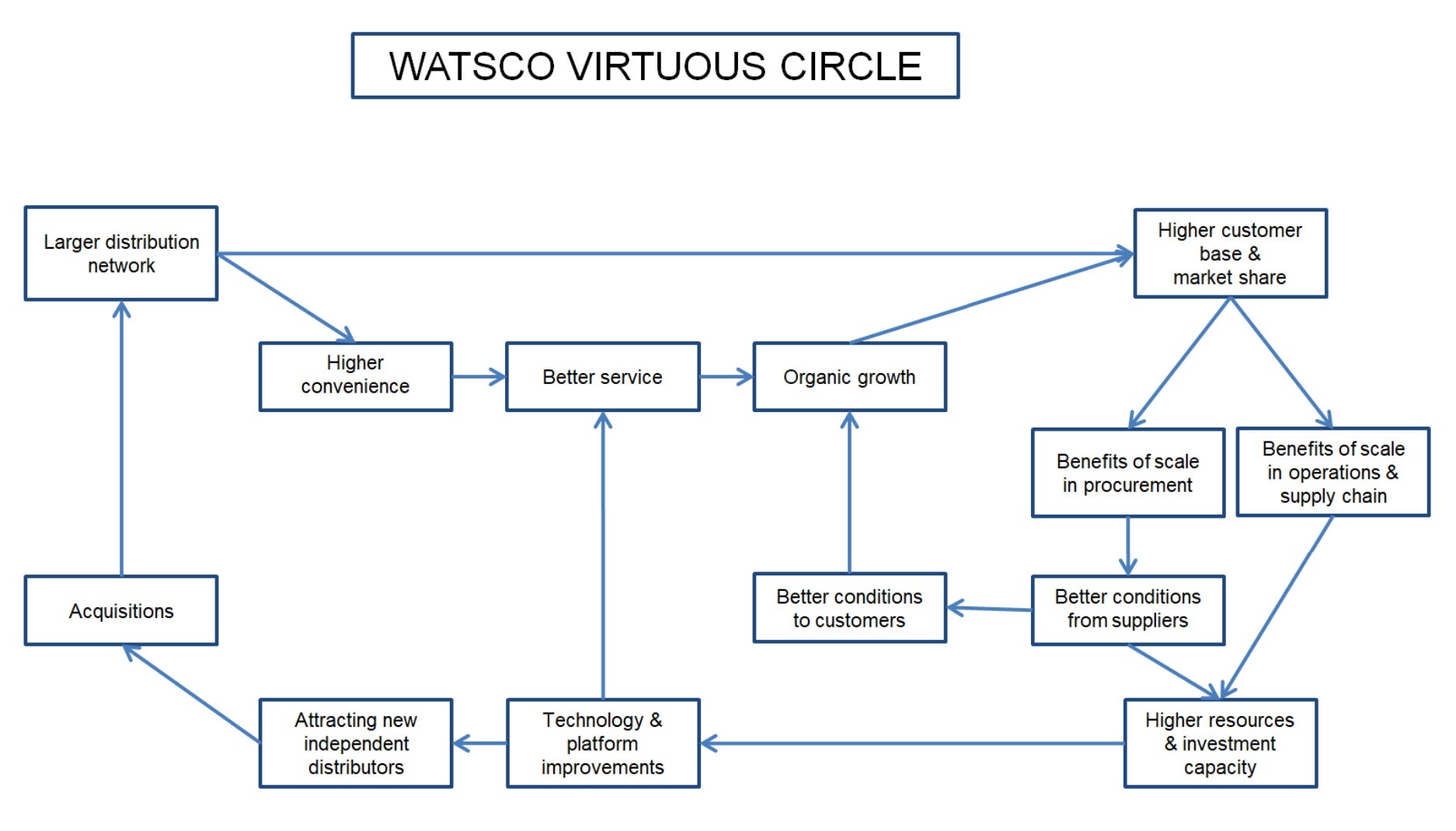

All these advantages create some sort of virtuous circle:

In few words, the larger the distribution network, the higher the customer base, but also the higher the convenience for contractors and the customer service for the whole network, which in the end benefits organic growth. The bigger the customer base, the better the conditions that the Company gets from its suppliers, which can be passed through to its customers, reinforcing again organic growth and customer base. This situation also improves WSO’s resources and its capacity to reinvest in the business, and these reinvestments suppose a constant improvement of its platform. Technology improvements help contractors and distributors to operate more efficiently and this serves as center of attraction for new independent distributors, which realize the benefits of working under WSO’s umbrella and the difficulties to compete with them. This circumstance steadily feeds WSO’s acquisition strategy and keeps its distribution network expanding.

The Acquirer’s Checklist

Apart from the wonderful business model presented in the previous paragraph, WSO possesses many other additional characteristics that make them to be an amazing business.

I’ve recently written an article trying to gather the best traits or practices identified after analyzing many of the best companies involved in acquisition activities. In order to analyze WSO, I will follow the checklist included in that article that contains 9 specific characteristics of a “good acquirer”. Let’s have a look if WSO matches all those characteristics:

Fragmented markets with a relevant pipeline

As commented in the article, serial acquirers need a fishing ground of potential acquisitions to deploy their strategy over time. Analysts must understand how big and fragmented the landscape is, how the market share is distributed within the industry and the intensity of the competition. The bigger and more fragmented the playing field, the longer the time the company will be able to apply its strategy and compound returns over time; and the lower the competition, the better the acquisition prices.

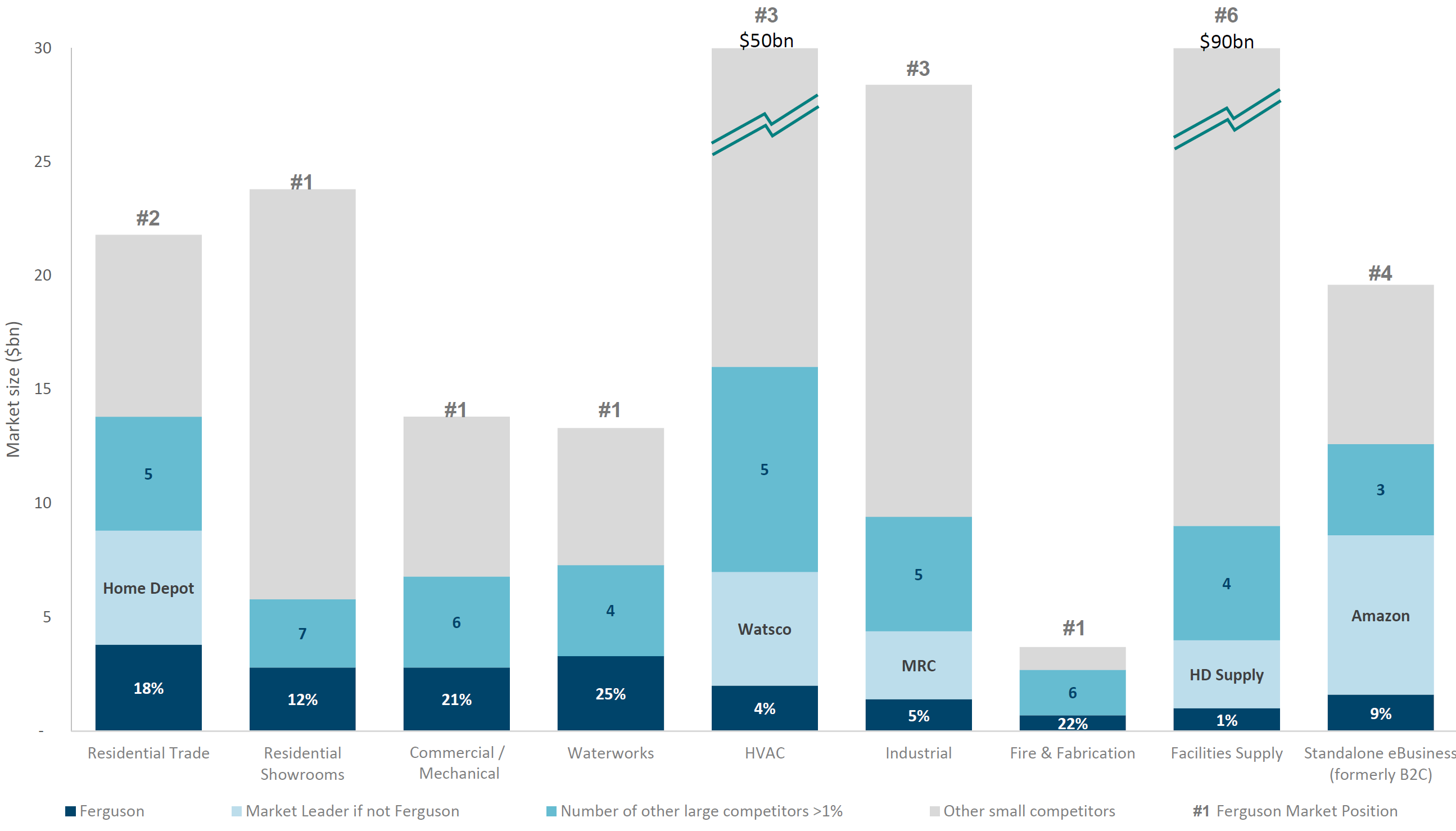

HVAC distribution is a highly fragmented market with few large operators and more than 1,300 independent players.

Besides, although there are (few) other big players competing for the consolidation process, the competition is rather limited due to a unique aspect of this market which is that OEMs have to allow their distribution rights to be transferred to someone else. This specificity keeps a lot of capital out the industry, as is the case of private equity or people outside the HVAC/R world, that have much more difficulties to access because in some sense OEMs do actually decide who can operate.

Evidence of real synergies and economies of scale

The best acquirers are those that are able to add value to the target company. WSO, as part of its “buy and build” strategy (see point 5 below), provides many advantages to the acquired companies that for them would be rather difficult to obtain or would require huge resources. Those companies that become part of the distribution network will have access to capital, technology, vendor relationships, exclusive OEMs programs, etc. WSO looks for well-run companies and helps them grow their businesses and broaden their product lines. WSO have repeated several times that they are not interested in cost synergies, their intention is not to take some costs out. Growth and scale are ultimately what will make acquired businesses to expand their operating margins.

Purchasing and pricing power

In close relation with the previous point, as a result of the economies of scale, best serial acquirers tend to enjoy some power within their supply chains. Those are cases where there is a relevant fragmentation among the acquirer’s customer and supplier bases, or when the position that the acquirer holds within the supply chain is so important that it is able to exert some power over its suppliers and/or customers.

In the case of WSO, its customer base is highly fragmented, with the Company serving more than 120,000 contractors and tecnicians, and none of them representing more than 2% of its revenues. This situation makes rather easy for the Company to pass any cost increase coming from the OEMs to its customers.

The supplier base is not so fragmented. The Company works with more than 1,200 manufacturers, but the reality is that its top ten suppliers accounted for 83% of its purchases in 2021, including 61% from Carrier and 10% from Rheem. However, due to the importance and scale of the Company (for instance WSO represents more than 25% of Carrier’s HVAC revenue), WSO is able to exert also some purchasing power over its suppliers.

Strategic financing and financial strength

In terms of financing strategy there are two relevant issues: the financial strength and the strategic finance of the acquisition strategy. With regard to the first point, WSO’s “long-standing goal is to maintain a conservative, risk-averse financial position”. The Company seeks to keep its leverage ratio well under control in order to be able to invest in new growth opportunities and have access to low-cost capital.

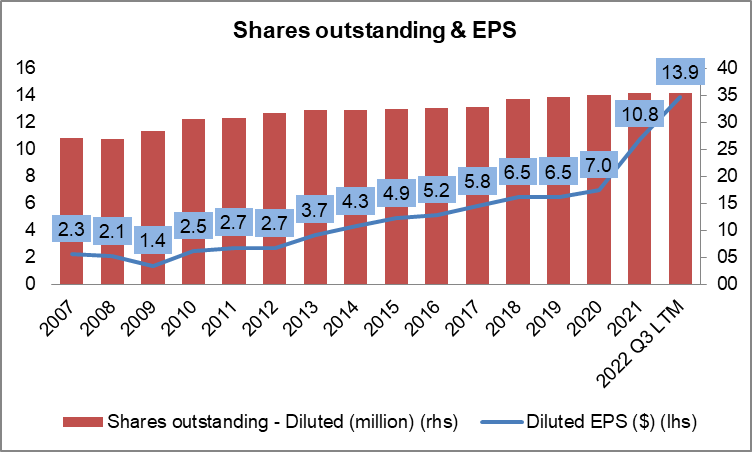

With regard to the finance of its acquisition strategy, acquirers must have a clear understanding of the different implications of the use of cash, debt and equity to carry out the acquisitions. Best acquirers tend to avoid dilutive acquisitions and to use the right mix of cash and debt. However, WSO is an outlier on this specific aspect. The Company places much more importance on the commitment that equity ownership represents, regardless of the potential dilutive effect, and tends to make acquisitions with a mix of cash and shares. Although the issuance of additional shares may have a dilutive effect, actually the result has been extremely successful throughout the years:

Well-defined acquisition strategy and disciplined approach

WSO acquisition strategy is perfectly defined and time-tested, but the most interesting characteristic is that it is rather unusual. WSO follows what they call a “buy and build” strategy: “the “buy” component of the strategy focuses on acquiring market leaders and the “build” component focuses on implementing a growth culture at acquired companies by adding products and locations to better serve customers”. The uniqueness of this model lays on its extreme decentralized approach: WSO has no intention of disrupting acquired companies, change their cultures or replace their leadership, quite the opposite. WSO encourages a growth culture at those companies, supports their leadership teams and deploys capital and a comprehensive suite of technologies, all aimed at fostering growth.

In terms of discipline, WSO has acquired 66 HVAC distribution businesses since 1989, typically paying 4-6x EBITDA, while WSO itself traded at double digit EBITDA multiples. This seemingly simple strategy has yielded incredible results: WSO have returned 20+% compounded TSR over the last 30 years by buying at those favorable prices and then integrating and growing a large number of businesses in its niche.

High employee and management team retention

As commented in the previous point, WSO doesn’t intend to disrupt acquired companies or change their leadership. There is a rather telling comment in one of its conference calls that perfectly explain the Company’s culture:

“We have a long track record of respecting the legacy of the companies that we buy. We don’t change their names, we don’t manage them. They manage it themselves. We’re in the background. We provide financial support, technology support, whatever they call that they need. We’re not about to even start to disassemble what they have already accomplished. Quite the contrary. We just wanted to go and get bigger and support it. That’s a very big deal for people that have created great companies and don’t want to see their legacy destroyed”.

WSO’s approach is to let the teams operate their business, providing just support and guidance when needed, but steeping back the rest of time. This kind of approach can only be successful with high employee and management team retention.

Strong alignment

Even though this is applicable to every company and not only to acquirers, those acquirers showing better results tend to be companies where there is a strong alignment between management and shareholders. Analysts must deep dive into executive compensation and insider ownership looking for hints of strong alignment, like preference for equity-based and performance-based compensations, long vesting periods for time-based compensations, and high levels of executive ownership.

WSO is a good example:

The Company’s long-term incentives program is mainly composed of restricted stocks that vest toward the end of the employees’ career (“this means our key leaders do not know and cannot realize the value of their restricted share awards until they have spent their respective careers with the Company”) and indeed, with regard to their Named Executive Officers (NEOs), they boast about “none of (their) restricted share awards have ever vested”.

In terms of ownership, there is also a strong alignment, as the CEO owns more than 11% of the Company (~$1,100m) and all the Directors and Executive Officers combined almost 14%.

Diversification

Best acquirers tend to use the acquisition strategy to create stronger structures through diversification. Acquisition strategies allow them to penetrate into new or adjacent markets and expand their presence into the existing ones, broadening their product offerings. Those strategies usually create stronger organizations that are much more resistant under downturns.

In my opinion, this is maybe one of the weakest points of WSO. The Company is completely focused on the HVAC/R industry. This is perfectly fine in terms of specialization, but also exposes the Company in case of any negative event specifically affecting this sector. There are other competitors (e.g. FERG) that try to avoid this excessive concentration by looking for adjacent businesses as home improvement, plumbing, waterworks or project management services.

Besides, as have been also commented, the Company’s top ten suppliers accounted for 83% of its purchases in 2021, including 61% from Carrier and 10% from Rheem. Though WSO assures that in case of any problem there would be substitute products readily available, any interruption by any of the key manufacturers would have a relevant impact.

In terms of segments, more than 80% of WSO business is residential and this means certain dependency on the housing market and home equity. Being fair, it is true that more than 65% of its business is in the replacement market (and not new construction), which is less cyclical, but in any case declining home prices would affect the Company.

Finally, in terms of geographic concentration, WSO generates 90% of its business in the US and almost everything in North America. Besides, the Company is rather concentrated across the Sun Belt with Florida and Texas combined containing almost 30% of its locations. Of course makes sense to be concentrated in those geographic areas, taking into account that we are talking about air conditioner, but this doesn’t mean that this is not a risk for the Company.

WSO has been historically operating this way and there is no doubt that rather successfully, but any adverse situation affecting specifically its industry, segments or geographic areas could harm the business.

Seasoned management

Last but not least, one of the main common denominators of the best acquirers is that they tend to be companies led by executives who have run this playbook before and show a proven track record of acquisitions. WSO has acquired and integrated 66 HVAC distribution businesses since 1989, all of them with the same management at the helm.

Industry Tailwinds & Megatrends

I think it is rather clear that WSO business model is really powerful and that the company plays a key role within the industry. But what about the prospects of the industry itself? As it will be discussed in the next point, there are some risks that could have a negative impact on the industry (possibly in the short term), but fortunately there are many factors that will probably more than offset them in the years ahead. Let’s have a look to some of these positive trends:

Environmental concerns & energy efficiency

Customers are increasingly worried about environmental issues and this is pushing regulators and industry stakeholders to take specific actions to respond to these concerns. As HVAC systems are one of the most energy consuming building services, demand trends are shifting towards high performance equipment and HVAC manufacturers are moving rapidly to provide innovative solutions that drive energy efficiency and emissions reductions for commercial buildings and homes.

In the last conference call, WSO comments that they “see a strong movement towards electrification of heating systems through the use of more heat pumps” (“which generally come at a higher price; higher margins; and in the long run, a shorter replacement cycle”).

All this sustainability movement creates a tailwind for the industry as, in general terms, this kind of initiatives bring the development of new environmentally sustainable and energy-efficient products, that in the end are accretive to the HVAC industry, increasing replacement levels, improving the product mix and bringing higher average selling prices.

Regulatory mandates

In close relation with the previous point, HVAC industry is highly regulated and regulatory mandates are one of its main drivers. Regulation tends to foster investments in the energy efficiency market and to boost equipment replacements and upgrades, benefiting HVAC market performance. Historically, energy efficiency mandates materialize in better sales mix of high-efficiency systems.

In the last conference calls, the Company mentioned some specific regulatory changes that will take place in the following years and are expected to have a positive impact:

The minimum federal SEER standards will increase in 2023 across the entire United States. The price points associated with these new products will be higher and should benefit 2023.

There is a Federal mandate to reduce the current high Global Warming Potential (GWP) refrigerants. Nowadays the mandate is a 10% reduction in these refrigerants but it is scheduled a 30% for 2025 and an additional 30% by 2030. All these measures are expected to again foster the replacement of older systems.

The Inflation Reduction Act (IRA), that will take effect on 2023, that is expected to foster equipment replacement through tax credits and incentives for homeowners (with the uncertainty of the pending the definition of qualifying products).

As long as the concern about the impact of HVAC systems on climate persists, regulatory changes aimed to reach higher efficiency levels will keep being a consubstantial part of the industry and fostering its future growth.

Migration toward southern United States

Migration patterns are causing economy and population to grow in many Sunbelt states:

Though this year there has been some slowdown in state-to-state moves compared with the early months of the pandemic, there are no yet signs this trend to start reversing and is expected to continue in the following years.

Sunbelt states are the main WSO markets and this should provide a relevant tailwind for the Company.

Healthcare and Aging population

There is no doubt that the population is aging. As stated by the Census Bureau “by 2030, all baby boomers will be older than age 65” and “this will expand the size of the older population so that 1 in every 5 residents will be retirement age”. Besides “older people are projected to outnumber children for the first time in U.S. history” and this trend is expected to keep going in the following years:

This is creating a megatrend for the healthcare industry and, specifically with regard to the HVAC industry, an increasing concern about air quality. People spend ~90% of our time indoors, where air can be 3-5x more polluted than outdoor air and this is specifically worrisome for the elderly. This is generating a shift towards high performance equipment to meet indoor air quality and is expected to bolster the demand for this kind of products in the future, with the correlative positive impact in terms of unit volume and mix.

Risks

Recessionary period

As is the case of almost every company, WSO is not at all immune to economic downturns and an additional deterioration of the current economic conditions could affect the company. The most relevant impacts usually come from consumer confidence and consumer spending.

Apart from the impact through the housing market (see next point), the most common effect materializes through the rate of replacement. During downturns consumers try to repair more often than typical, postpone as much as possible the replacement of their equipment and focus more on replacement parts. Besides there is usually a trading down effect and customers tend to buy the minimum efficiency they can buy (which is the cheapest).

During the GFC the Company was able to stay profitable, but the impact was severe:

Fortunately for the Company, the products that it provides may be considered necessities and there is a relevant part of its business that is less cyclical. Besides, in my opinion, nowadays we are in different situation (see next point) but anyway further negative evolution of the economy will probably impact the Company (at least in the short term).

Housing market

There is part of WSO’s business that is linked to the housing market evolution. Demand related to the new construction sectors (10-15% of the business) depends largely on new housing starts and completions. The remainder residential business (65-70% of the total business) may be not so dependent on the housing market, but existing homes sales are for sure a relevant variable.

Besides, it is not only about transactions but also about prices. Home equity could affect consumer confidence and consumer willingness to carry out a HVAC project. It is still uncertain how deep could be the slowdown in the US housing market, although probably not like the one on the GFC as this deceleration could be cushioned by a relative lack of available homes in the U.S. and the still strong job market and household finances. However, in case of a sharp deterioration, the impact might be relevant.

Price realization and FIFO accounting

This is a short-term risk that could temporarily affect the Company. During the last quarters WSO has been positively affected by inflation and price realization. Under inflationary environments, FIFO (First-in, First Out) will result in higher profit margins: the cost of older goods will be lower than the cost of newer goods, so selling off older goods first will result in a higher profit margin. The problem arises when these inflationary dynamics change, which is expected to happen sometime in the future, and this may produce the opposite effect, negatively impacting its margins and results.

Additionally, there is also a part of gross profits that depends on how and when the Company pays to its vendors (i.e. discounts, rebates, incentives, etc.) and this feature has had a relevant positive impact during this period of high activity. In case of some normalization/reduction of purchasing activity, specifically taking into account management plans to take inventory down, this positive impact would be expected to lower.

Supplier concentration

This was a point already commented in the previous paragraph (point 8). WSO has been historically concentrated in different aspects (by suppliers, by geographies, by segments, etc.) but it has been able to operate extremely successfully. However, this doesn’t mean that this is not a risk for the Company and should be monitored.

Credit risk

One of the key WSO’s competitive advantages and that differentiate them from smaller distributors is its capacity to provide funding to its customers. The Company tends to keep the level of its account receivables rather stable and well under control:

However, as it can be observed in the chart, during recessionary periods the level of impairments may increase and, despite not being significant amounts, could have a negative impact on the Company .

Disintermediation

The distribution activity, whatever the sector, is always under the sword of Damocles of being disintermediated by manufacturers/OEMs. These companies try to look for direct-to-consumer (D2C) strategies to improve their financial performance and enhance direct connections with consumers, and, nowadays, with the digital revolution and the expansion of e-commerce, this possibility is more real than ever. Indeed there are many examples within the HVAC industry of companies pursuing this D2C approaches (e.g. Johnson Controls, Daikin, Carrier, etc.).

The problem is that distribution plays a really valuable role and many times this disintermediation makes no sense. The key is the capacity (or lack of) of the distributors to add value to the customers.

As I think it has become clear throughout this article, WSO provides many advantages to all the stakeholders within the industry and plays a key role in the supply chain. This is the reason why I consider this is not a peremptory risk, at least in the short-to-medium run, but of course is something to not disregard.

Valuation and Final Thoughts

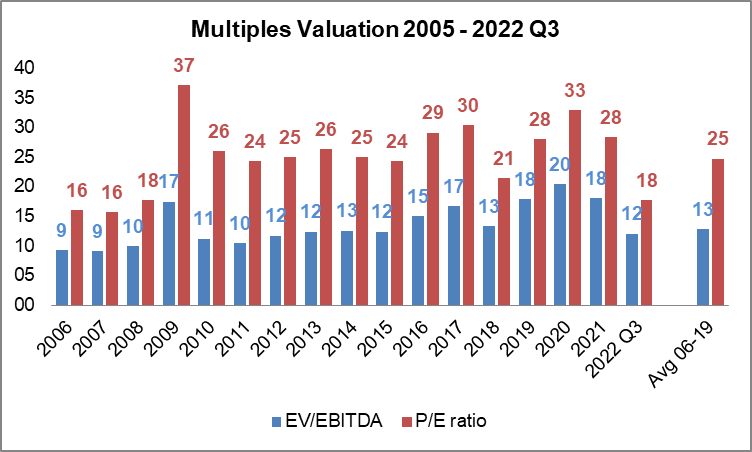

WSO reminds me a lot POOL in the sense of WSO begin also the kind of company that, at first glance, always seems expensive, with multiples well above the ones that could be considered as “reasonable” for an average company. However, this is a rather common characteristic of those exceptional companies that, due to their quality and trajectory, are usually trading with a premium over the market. In that sense, it is sometimes much more useful to compare the company with the historical levels of the company itself in order to have an idea of its current valuation:

As it can be observed, the Company is currently trading below the last years multiples but rather in line with the average of the period 2007-2019 (which includes the GFC and excludes the potential distortion of the period 2020-2022). Besides, the multiples don’t take into account potential earnings normalization that could take place in the near future. WSO has clearly benefited during the post-COVID recovery and its multiples might be “artificially” low.

Anyway, in order to have a more comprehensive view, let’s compare also with other specialty distributors:

The Company is rather in line with its peers and with the average. This is a slightly heterogenic list of companies, but in any case it doesn’t seem WSO to be extremely under or overvalued compared with them.

As commented throughout this article, there are some uncertainties in the short-term that could affect the company and its sector. Besides there is a non-negligible part of the HVAC industry that is linked with the evolution of the real estate market and the general economy and this could affect the Company valuation in the near future. However, from a longer term perspective, this is a company with many tailwinds and with much room to keep deploying its strategy. In my opinion, there are no specific circumstances that could make think that this company will not keep thriving in the future and, in that sense, it is for sure a company to keep in the watchlist and maybe look for attractive entry points.