The misinterpretation of Jeremy Siegel’s chart

The misinterpretation of Jeremy Siegel’s chart

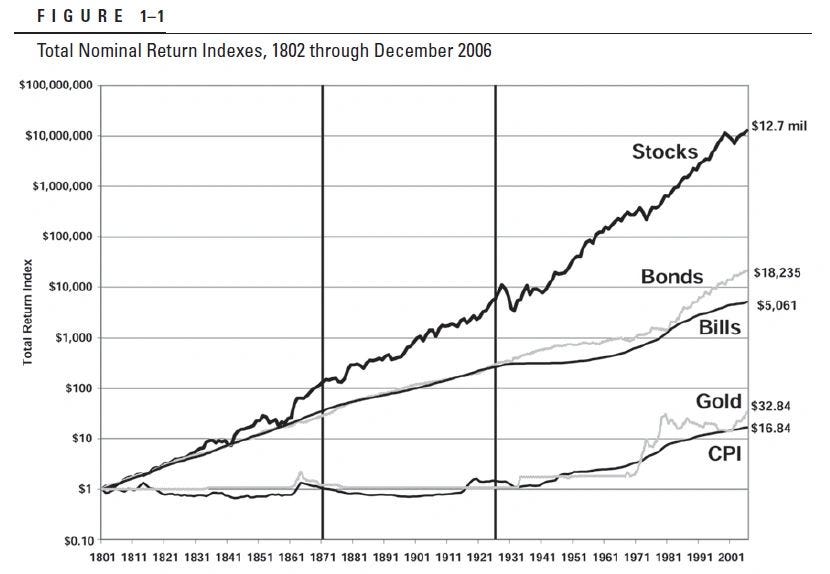

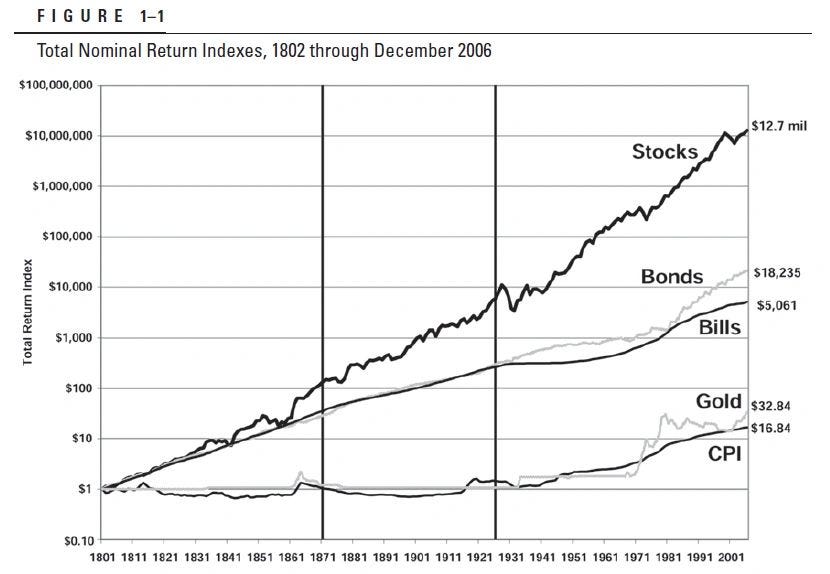

I have recently read the article “Do Global Stocks Outperform US Treasury Bills?” (by H. Bessembinder, T. Chen, G. Choi and K.C. J. Wei). This interesting article made me (re)think about one of the most, in my opinion, misleading dogmas about investing: stocks always outperform in the long run. To the dispersion of this misleading statement has broadly contributed the widespread misinterpretation of the famous Jeremy Siegel’s chart (included in his book “Stocks for the long run”):

First of all I would like to make clear that I profoundly admire Jeremy Siegel and his contribution to the investment world. It is not the case of this writing to discredit him (I couldn’t even if I wanted to). Indeed Siegel’s chart is of course perfectly correct and the abovementioned article is in line with the chart in the sense that it specifically states that its findings don’t “contradict the evidence that returns to broad stock markets handily outperform returns on Treasury instruments”.

So where is the misinterpretation? The misinterpretation lies in the extrapolation of Siegel’s chart, which refers to a specific strategy with stocks (i.e. exposure to the broad US stock market), to individual stocks (or to other strategies that don’t imply exposure to the broad stock market). Let me briefly explain this point.

Siegel profusely explains in his book how the chart was created. It is not the case of this article to dive deeper on its construction, so, just to summarize, the idea was to include all US stocks and then compare with “long- and short-term bonds, gold, and commodities from 1802 through 2006”. So in the end the chart depicts a comparison among total return indexes for different assets. Nothing more, nothing less. The interpretation of this chart should be that, in the period analyzed, a very specific group of stocks (i.e. all US stocks) outperformed other specific groups of assets (i.e. long- and short-term bonds, gold, and commodities). And the key word here is “specific” because it refers to a group composed of concrete stocks and to how they behaved all together.

The problem is that this interpretation is commonly (and inappropriately) extended to all the stocks (individually considered or in different combinations) in order to support investing in stocks. So it is rather common to show this chart in order to convince investors that they should skew their investment strategies to stocks (to the detriment of all other investable assets) because, in the long run, stocks (regardless of choosing them individually or in any combination) outperform all other assets. But this is not necessarily true or at least Siegel’s book is not demonstrating this. The book demonstrates empirically that in the long run a specific basket of stocks (which represents the whole US stock market) have outperformed other specific assets (or baskets of assets) but this is completely different to the generic statement of “stocks outperform in the long run”. Siegel’s book didn’t help because just below the chart it states that “it can be easily seen that the total return on equities dominates all other assets”.

The popularization of this believe has contributed to create the false perception that if someone invests in individual stocks or combinations of stocks, whatever the strategy, he/she will outperform if waits time enough. But this is far from true: the “buy-and-hold” strategy per se (or, more specifically, the “buy-and-forget” strategy) doesn’t guarantee success at all.

Fortunately, Bessembinder’s article provides empirical evidence about the wrongness of this misperception and this is perfectly summarized in its two key findings:

The overall stock markets outperform Treasury Bills in the long run, but most individual stocks don’t.

The article indeed specifically states that “only 40.5% of global common stocks, including 43.7% of US stocks and 39.3% of non-US stocks, have full-sample buy-and-hold return that exceeds the accumulated return to one-month US Treasury Bills over matched time horizons”. This basically means that most US stocks, individually considered, underperform one-month US Treasury Bills in the long run (let alone the market!).

The excess return for the broad stock market is driven by very large returns of relative few stocks.

"We show that the five firms (0.008% of the total) with the largest wealth creation during the January 1990 to December 2018 period (Apple, Microsoft, Amazon, Alphabet, and Exxon Mobile) accounted for 8.27% of global net wealth creation and 5.56% of global gross wealth creation. The best performing 306 firms (0.5% of total) accounted for 73.03% of global net wealth creation and 49.08% of global gross wealth creation. The best performing 811 firms (1.33% of total) accounted for all net global wealth creation, and 67.20% of gross global wealth creation."

This finding implies that it is not just difficult to outperform US Treasury Bills in the long run by picking stocks individually, but also making combinations of different stocks. As the excess return is driven by few stocks, any combinations of stocks that don’t include any of those “winners” will have a lot of difficulties to outperform

Indeed, in that sense, the article provides a good explanation for the active investing underperformance: should the excess return for the market is driven by few stocks, stock-picking becomes a rather difficult activity and few active managers will be able to outperform. In other words, should an active manager is able to select these scarce winners, the reward will be huge, but this is against the odds, as it is consequently outperforming the market (and even the US Treasury Bills).

Does this mean that we should reject active investing (or stock picking) and blindly flight to passive strategies? I wouldn’t conclude that. It is important to eradicate false investing dogmas in order to make more informed decisions, but making clear that active investing is against the odds doesn’t invalidate the strategy per se. Indeed there are many professional fields where returns are highly skewed (e.g. professional sporting; film/music/entertainment industries; many liberal arts; etc.) and this doesn't justify to not participate in. Stock pickers who are capable to select “the few stocks that will create the most wealth” will be highly rewarded. However it is important for them to be conscious about the relevance of stock picking for the final investing results and that the odds are against them.

All in all, investors should get rid of this idea that stocks always outperform in the long run. This is not true as Bessembinder's article has been able to demonstrate. And, more broadly speaking, investors should be willing to question all investment dogmas.