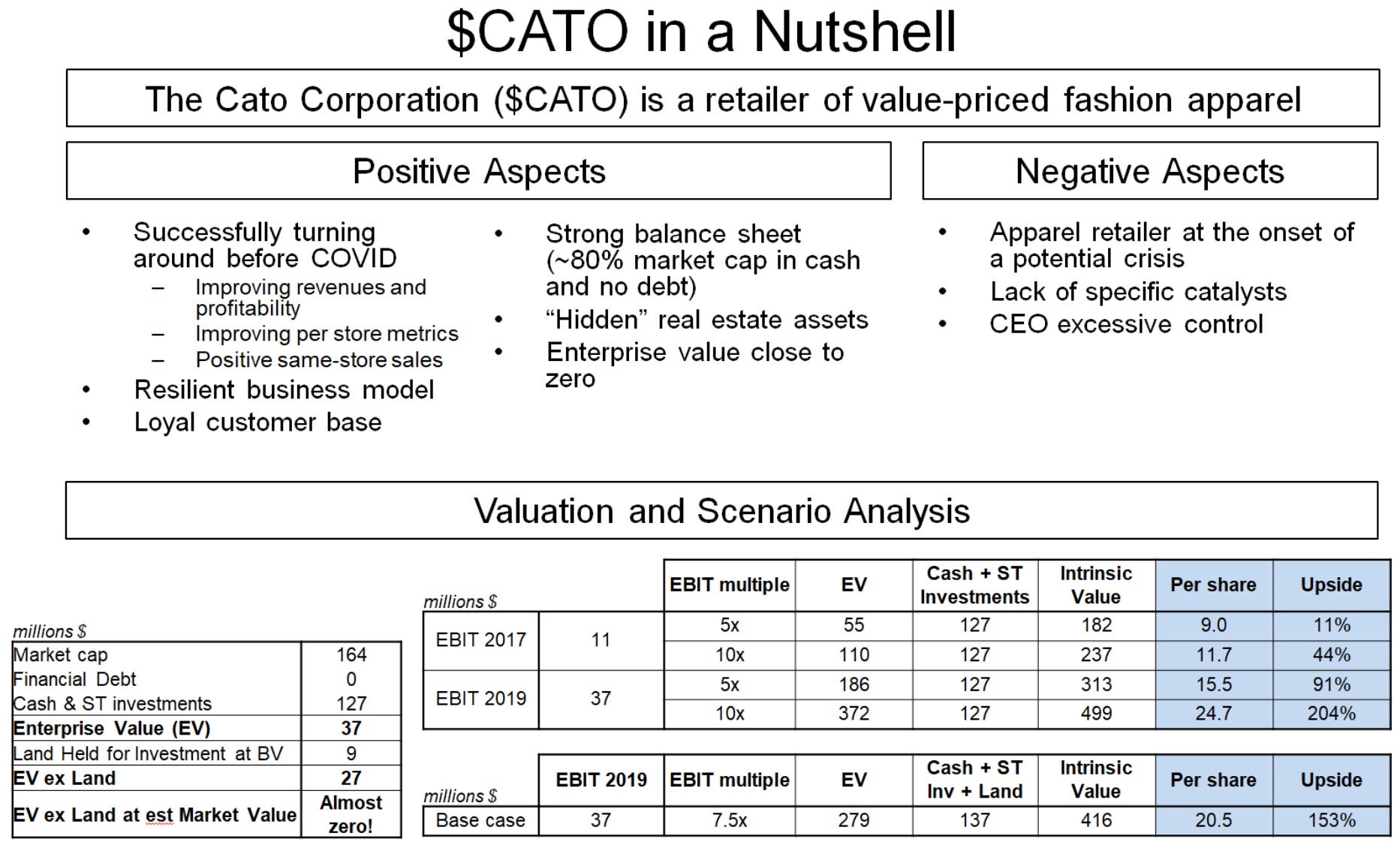

The Cato Corporation (CATO): a Value Play

The Cato Corporation is an apparel retailer whose successful turnaround was interrupted by the pandemic.

In 2019 they were gradually recovering from a period of underperformance, with more favorable trends in terms of same-store sales and merchandise margins, inventory control and profitability.

The potential upside is huge in case of the Company being able to recover pre-pandemic levels (150%+ upside under conservative assumptions)

Additionally the Company presents a strong balance sheet, with excess cash, no financial debt and “hidden” assets; and a business profile that could help to better overcome a potential crisis.

The Opportunity

The Cato Corporation (CATO) is a retailer of value-priced fashion apparel and accessories. I do know that this may be enough for many people to stop reading this article. Don't be discouraged! This is a really interesting risk/reward opportunity (and in any case the article is reasonably short).

In that sense, let me be clear from the very beginning and rei…

Keep reading with a 7-day free trial

Subscribe to JustValue to keep reading this post and get 7 days of free access to the full post archives.