Spotify ($SPOT): Great Expectations with an Unclear Path to Success

Spotify ($SPOT): Great Expectations with an Unclear Path to Success

Introduction

I think there is little controversy about Spotify (SPOT) as product: Spotify is a leading music streaming service that provides access to over 100 million tracks and much more audio content, with a great user experience and all over the world. Of course there are many people that prefer other apps (indeed millions of its peers’ subscribers), but it is rather common to hear people praising the wonders of this streaming service. However, as often happens, a great product is not always the same as a good business, much less a good investment.

Being said that, the main objective of this article is to look at the (far) future of the business and specifically through the lens of the recent 2022 Spotify Investors Day. During this event the Company presented its current roadmap and future growth opportunities, and communicated its ambitious long-term financial objectives (for 2030). Those financial objectives revolve mainly around revenue growth and margin expansion, and I will try to critically assess with a long-term perspective if those might be considered realistic.

Before starting, let me also make clear what NOT the purposes of this article are. This article is not intended to explain Spotify’s business model. There are plenty of articles out there talking about Spotify history and business model (e.g. Not Boring, GARP Businesses, FourWeekMBA). I will not deep dive on these issues, making just short references in case of being necessary for the understanding of this article. Additionally the idea is not to analyze last results presentation or to provide a forecast about how could the stock perform in the following months. This article aims to look to a more distant future and analyze if there is a clear path to success.

Being made those caveats, let’s start with the first financial objective: revenue growth.

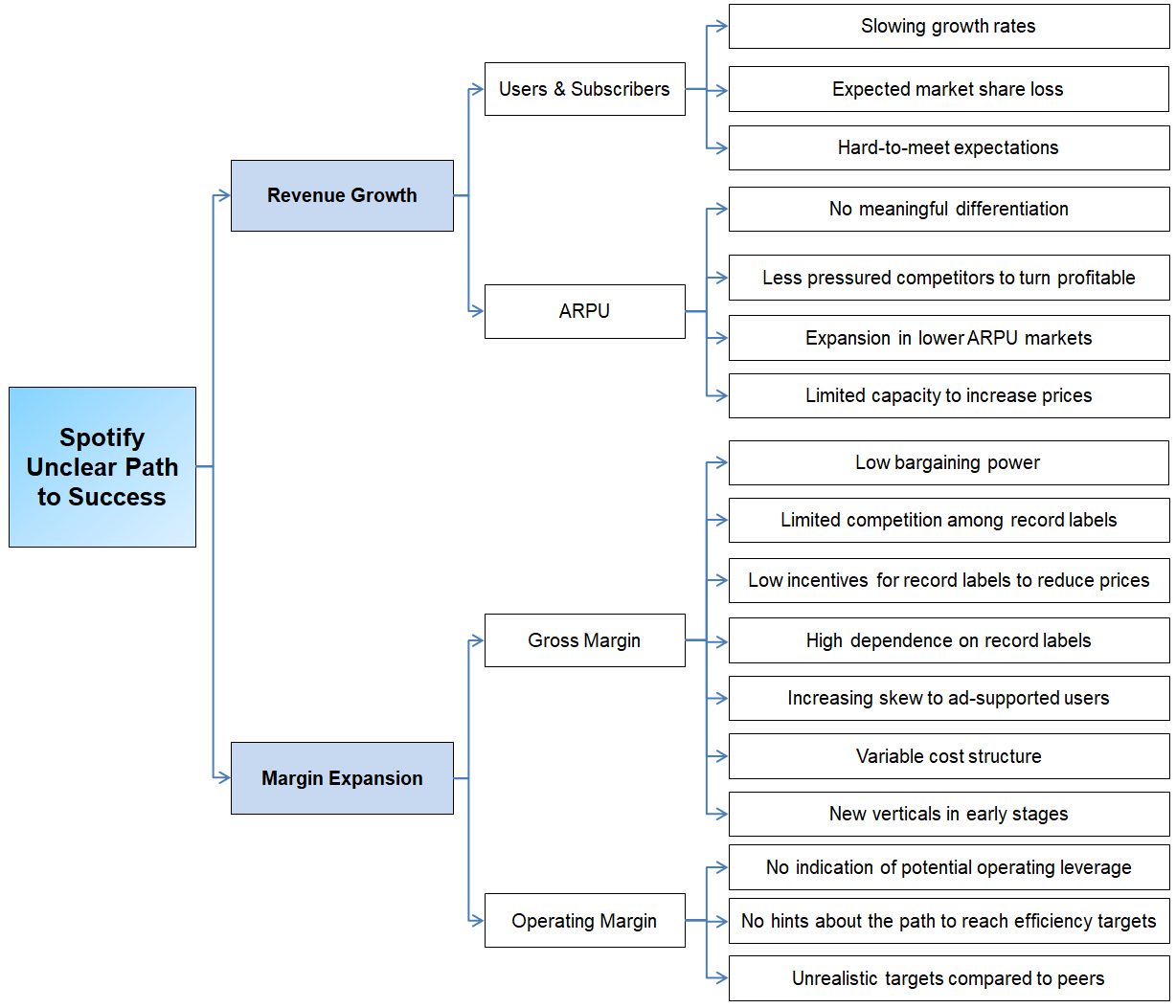

Revenue Growth

There are basically two metrics that determine revenue growth in the case of SPOT: users and subscribers and average revenue per user (ARPU).

Users and Subscribers

The targets outlined during 2022 Investors Day in terms of users are rather ambitious: the Company expects to hit over 1,000M users globally by 2030 (from 489M by end 2022). There are no specific targets in terms of paid subscribers, but taking into account that the current ratio of ad-supported MAUs to paid subscribers is 1.4x and that it would be expected this ratio to keep growing in the future (see below), we could hypothesize that, out of these 1,000M users, there might be approximately 350-400M paid subscribers (from 205M by end 2022). While those are apparently rather ambitious targets, let’s try to figure out should we consider these goals are realistically achievable.

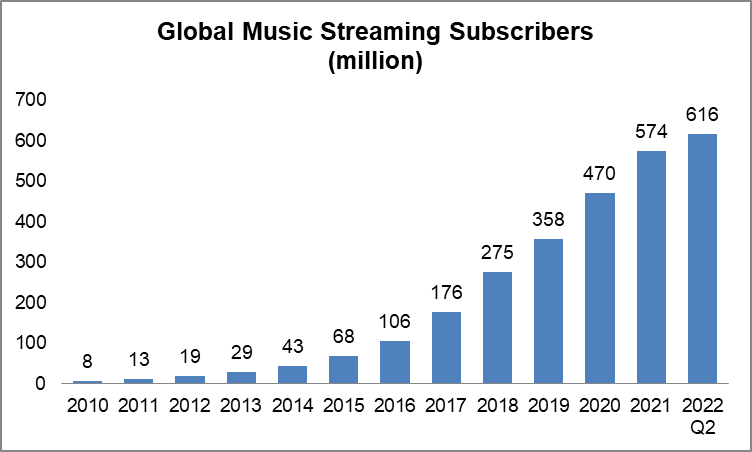

First of all, let´s have a look to the recent evolution of the industry and what can be expected in the future:

As it can be observed the evolution in the last decade has been impressive. After some years of “early adopters”, the industry entered in the period of mass adoption (at least in the developed markets) with an accelerated growth since 2017. Despite this impressive evolution, it is considered that music streaming is “still in early stages of global adoption and penetration” and there are many tailwinds that invite to think that this positive evolution will continue in the future:

While the current figure of paid subscribers is huge, “it still represents less than 14% of the 3.9 billion smartphone users globally in 2021, according to Newzoo” (data from other sources point to penetration levels even lower than 10%) and it’s been steadily growing during the last years:

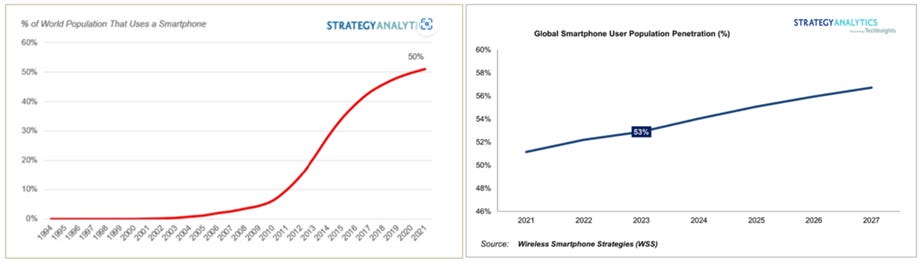

The accretion of streaming users/subscribers and the development of streaming services are considered to be mainly “driven by improvements in mobile internet, broadband and the range of consumer devices across mobile, web, smart speakers and smart TV platforms”. Both broadband wireless and smartphone users penetration are expected to keep growing, with predictions of over 5 billion people using smartphones worldwide by 2030:

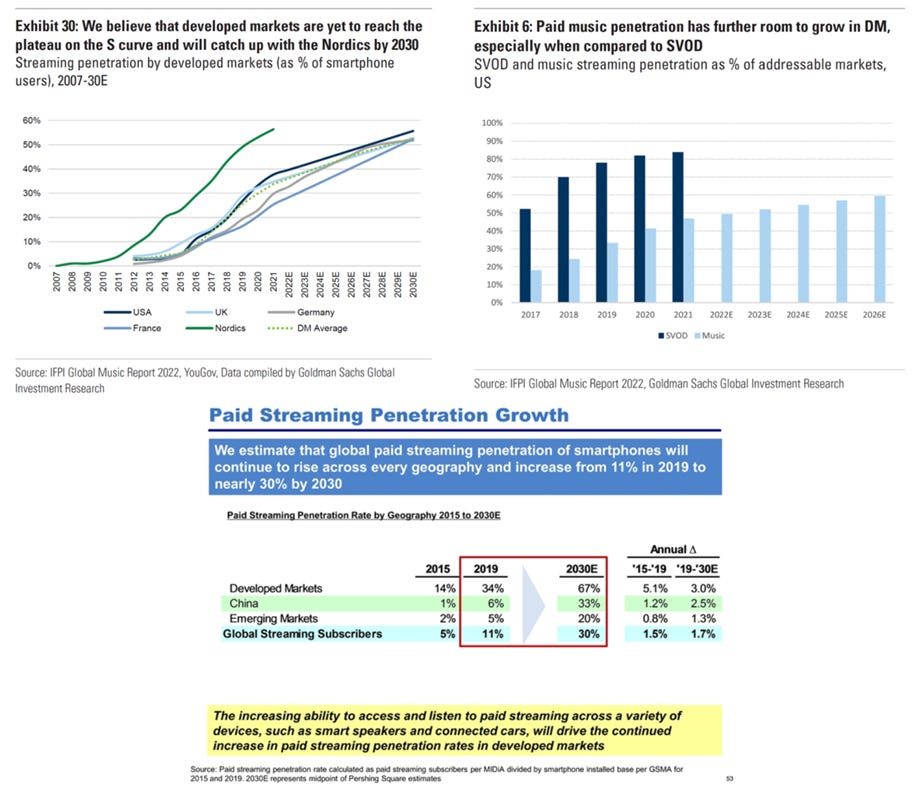

Looking at the music streaming penetration rates in early-adopter markets (i.e. Nordic countries) and in other subscription services (e.g. SVOD), it seems that paid music penetration has further room to grow in developed markets:

In the case of emerging markets (as it can be observed also in the previous chart), the opportunity remains substantial, with countries such as Brazil and India where paid streaming penetration is low compared to developed markets: “according to Goldman Sachs, paid streaming penetration for Brazil and India in 2021 was 12% and 1%, respectively”. The Asia-Pacific region alone will have 0.5 billion subscribers by 2030, according to Midia Research and Europe and North America will represent just 23% of subscriber growth between 2021-2030.

Even if we just look at SPOT’s evolution itself, there are reasons to be rather optimistic:

The Company has been able to steadily increase its users and subscribers base during the last years by both penetrating in its existing markets and opening new ones.

However there are some circumstances that invite to be also cautious with the data regarding SPOT:

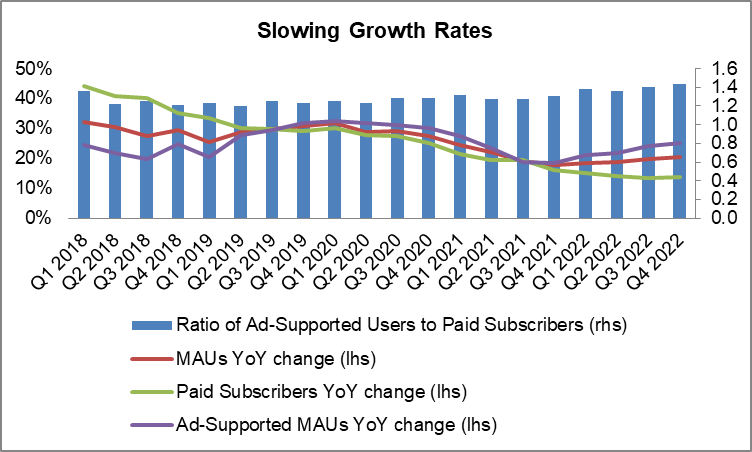

Despite its continue increase in terms of users and subscribers, the trend is slowing:

Although this deceleration is rather expected as the base increases, the slowing growth in the case of paid subscribers is being significant. The Company has been able to revert the tendency in the case of ad-supported MAUs, but as it starts to increase its growth in emerging markets and reduces its capacity to grow in more mature markets, we will probably continue to observe this tendency of an increasing ratio of ad-supported MAUs to paid subscribers.

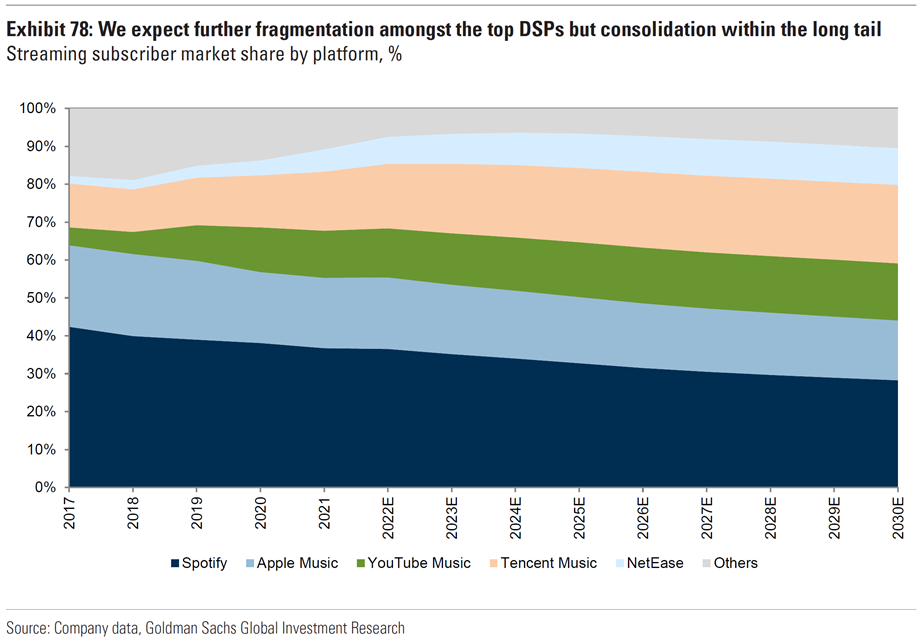

SPOT is losing market share and it is expected this tendency to continue as niche apps or local apps in emerging markets gain market share. Goldman Sachs expects Spotify to retain its leadership over time but with a 26% share of subscribers in 2030 (instead of the 34.4% in 2021):

Should we consider the number of smartphone users predicted by 2030 (5 billion users), SPOT target would basically imply seizing 20% of them and this would mean an impressive increase from the current ~12% (489M MAUs of approximately 4 billion smartphone users).

In summary, despite all these caveats, it is expected the industry and the Company to keep enjoying a healthy growth in terms of users and subscribers. Acknowledging that SPOT’s targets are rather ambitious, these might be considered the most achievable of all the ones presented during the Investors Day (as we will see in the following paragraphs). Reaching 1,000M users and 350-400M subscribers by 2030 would imply a 12% and 10% CAGR, respectively, compared with the current annual growth of 19.7% and 13.4%. Besides, this is rather in line (slightly above) Goldman Sachs estimate, which expects 1,260M global paid subscribers by 2030 and assigns to SPOT a market share of 26% (~330M subs).

Average Revenue per User (ARPU)

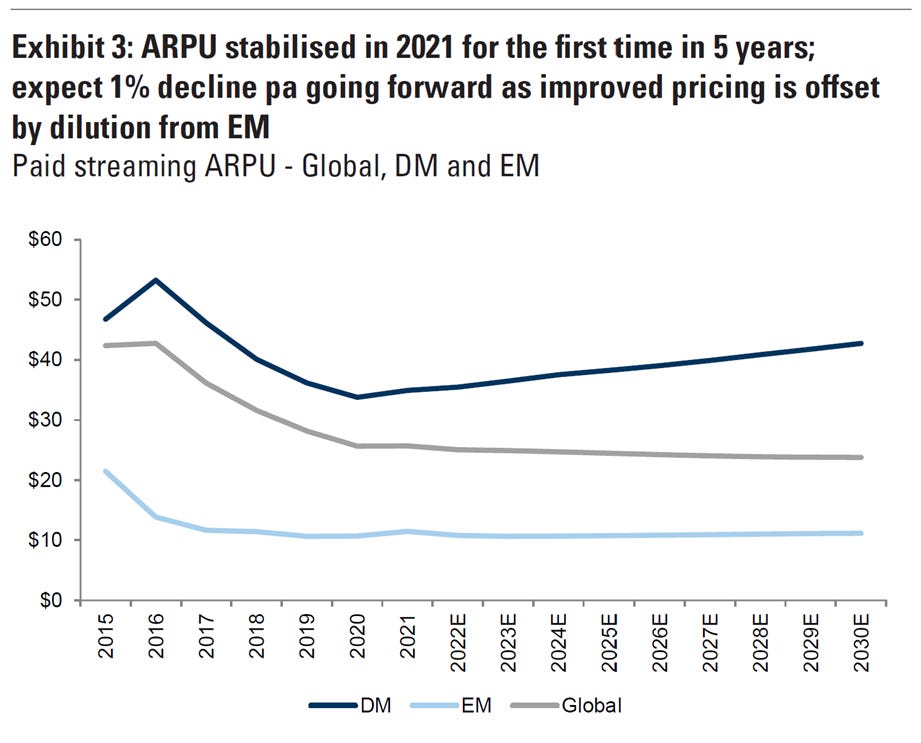

In terms of ARPU the goals are even more ambitious than in the case of users. SPOT expects to quadruple its current ARPU levels by 2030, doubling the ARPU of its core business (including podcasting) and adding 2x ARPU from new verticals:

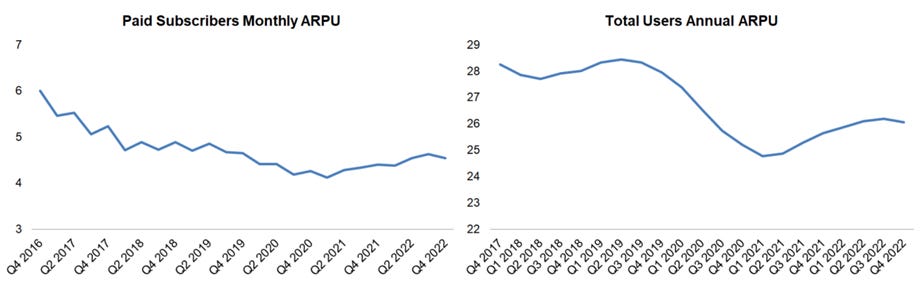

In order to have a better contextualization, let’s have a look first to the recent evolution of the ARPU within the Company:

As it can be observed, the ARPU has been steadily declining until the first quarter of 2021. This decline was mainly due to the growth of multiusers plans (i.e. Family and Student Plans) launched in 2014. Being true that those Plans have helped improve retention and churn reduction, the ARPU has been seriously affected. Price increases in the Family Plan implemented in 2021 in some markets have been able to revert slightly this tendency, but anyway we can acknowledge that the starting point to think about a skyrocketing ARPU from here is not the most promising.

However, as I mentioned at the beginning of this article, the idea is to look forward and think about how the ARPU could evolve in the future. The problem is that it is exactly when I think about the future that much more uncertainties appear and invite to be really cautious:

The first doubt in terms of ARPU is related with the core music business. Regardless of SPOT’s diversification efforts, music is still by far the most relevant part of its business and it’s starting to become some sort of commodity, which is offered by most of its major competitors and that makes rather difficult for the Company to increase prices based only on this. SPOT is pretty conscious about this issue (indeed it realized many years ago) and this is probably the main reason for the pivot that is carrying out to open new verticals. It is urgent for the Company to differentiate its offering, but this requires investments and time.

This situation reminds the one experienced by the SVOD industry some years ago. The players in that industry were aware of the importance of differentiation and started to meaningfully increase the investment in proprietary content, making the offer from each SVOD platform to be significantly different (and being able to lift their prices). In the case of Spotify there is currently “no meaningful content differentiation from its competitors” within the music business.

Additionally it may be rather difficult for SPOT to increase prices because most of its competitors can keep their music-arm unprofitable. Spotify is much more pressured to turn a profit, while virtually all the other big music streaming services can continue making losses as they are part of bigger organizations that can subsidize the music business (e.g. Apple, Amazon, Google/Alphabet).

As established markets matures and growth skew to emerging markets this will probably imply progressively more global growth coming from lower ARPU markets, pressing down ARPU and making increasingly difficult to translate users/subscribers growth into a proportional revenue growth (“for example, Spotify Premium costs around a tenth as much in India as in Denmark”).

Besides, the conversion rate from ad-supported to paid subscribers within these emerging markets is also expected to be lower than in the case of established ones, so regardless of the potential success in adding users to its service, the rate of generating paying users might deteriorate, with the correlative impact in terms of ARPU.

Price increases need to be managed carefully because the higher the price of paid subscriptions, the more attractive the ad-supported version and peers’ offers become (“competing with free is always very difficult because consumers have a choice to move to free”). In case of subscribers switching to another service, the impact wouldn’t only affect paid subscriptions but also to ad-funded revenue, as “advertisers would switch too as they seek more listeners to their ads”. So even admitting that the Company could enjoy some pricing power, it seems nowadays rather difficult for them to quadruple its ARPU without a relevant impact on its subscribers’ base (both in terms of users and business mix).

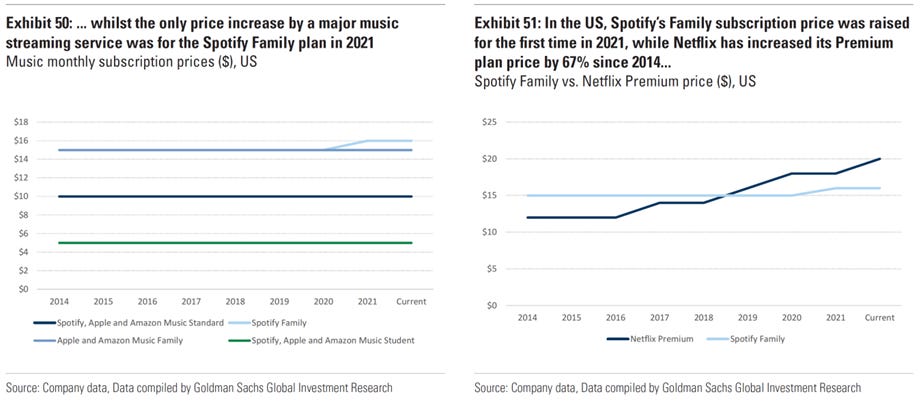

Most of the music streaming companies offering premium services charge broadly identical price and this has remained almost unchanged during the last decade. This situation could perfectly respond to a specific pricing policy more focused on growth than in profitability, but at the same time could provide some hints about the limited capacity of these companies to meaningfully increase its prices and also makes rather difficult to infer what could be the reaction of their subscribers in case of price increases.

The existence of free alternatives may help also to “depress the value that consumers are willing to pay for paid streaming services”. The most relevant example is the case of UUCs platforms like Youtube, which represents a relevant part of global music streams. Even free providers like TikTok are rumored to be planning the launching of a music streaming service.

I do believe that SPOT have pricing power in some markets and it may be able to increase its prices, thanks specifically to the many improvements that has made in terms of content and user experience, and to the stickiness of its product. The problem is that due to all the issues mentioned above, any increase in price will probably be rather limited and potential ARPU improvements in some markets will be probably offset by the expansion into lower-ARPU markets. Anyway, even accepting the possibility of higher ARPU levels, it seems rather unlikely achieving the levels outlined in the Investor Day.

In my opinion, the next chart from Goldman Sachs, though it refers to the whole industry, better exemplifies the potential ARPU evolution that the Company might experience in the following years:

This doesn’t mean that SPOT won’t necessarily be able to increase its ARPU but at least invites to strongly reduce the Company’s optimism and to think that achieving the 4x ARPU depicted in the Investors Day will be really difficult.

Margin Expansion

Gross Margin Expansion

There are basically two different ways for Spotify to expand its gross margin: expanding the gross margin of its core music business or entering new activities or verticals with higher margins.

With regard to the potential increase of the music gross margin, the Company’s target is to reach 30% in the next 3 to 5 years and 35% in the long-term (from the 28.3% at the end of 2021):

Being music the lion’s share of its revenues, expanding its gross margin is absolutely key to achieve higher margins at consolidated level. The problem is that there are some forces that make rather difficult for the Company to increase its gross margins in the music business and that have prevented SPOT from materially increase them during the last years. Indeed I think that the decision to “move beyond music” and become “the world’s leading audio platform”, more than an ambition, it is a necessity. The Company seems to have realized that it may be rather difficult to really achieve a profitable and scalable business just working in the music business and it is imperative for them to open new verticals.

Let’s have a look to some of the forces that make rather difficult for the gross margins in the music business to increase:

The value proposition of music streaming services like Spotify is “based on offering a wide range of music to consumers, covering all the content from the majors and most other record companies”. As different record labels provide a different repertoire, this “full catalogue” model forces in some way music streaming services to cover as much music content as possible and makes rather difficult for them to drop any of the major record labels. This in turn provides record labels with a lot of bargaining power and makes difficult for streaming services to renegotiate their contractual terms.

In the same vein, given the importance of offering a “full catalogue”, a music streaming service unable to reach an agreement with a major record label and “losing a significant portion of its catalogue could face substantial risks of deterring prospective customers and of many existing customers switching (even in the context of some barriers to switching)”. This situation places streaming services in a weaker negotiating position than the record labels.

This situation also creates an environment where record labels have limited incentives to compete on price with each other and reduce its tariffs (streaming services need the whole catalogue of all record companies), making rather difficult for companies like SPOT to meaningfully increase their music gross margins.

Additionally, there are many clauses in the agreements that have the effect of protecting the position of the (major) record labels. Most Favored Nation or non-discrimination clauses prevent record labels from obtaining terms that are worse than those being offered to others. This in the end reduces the incentives of record labels to compete among them and so makes even more difficult for streaming services to improve their margins.

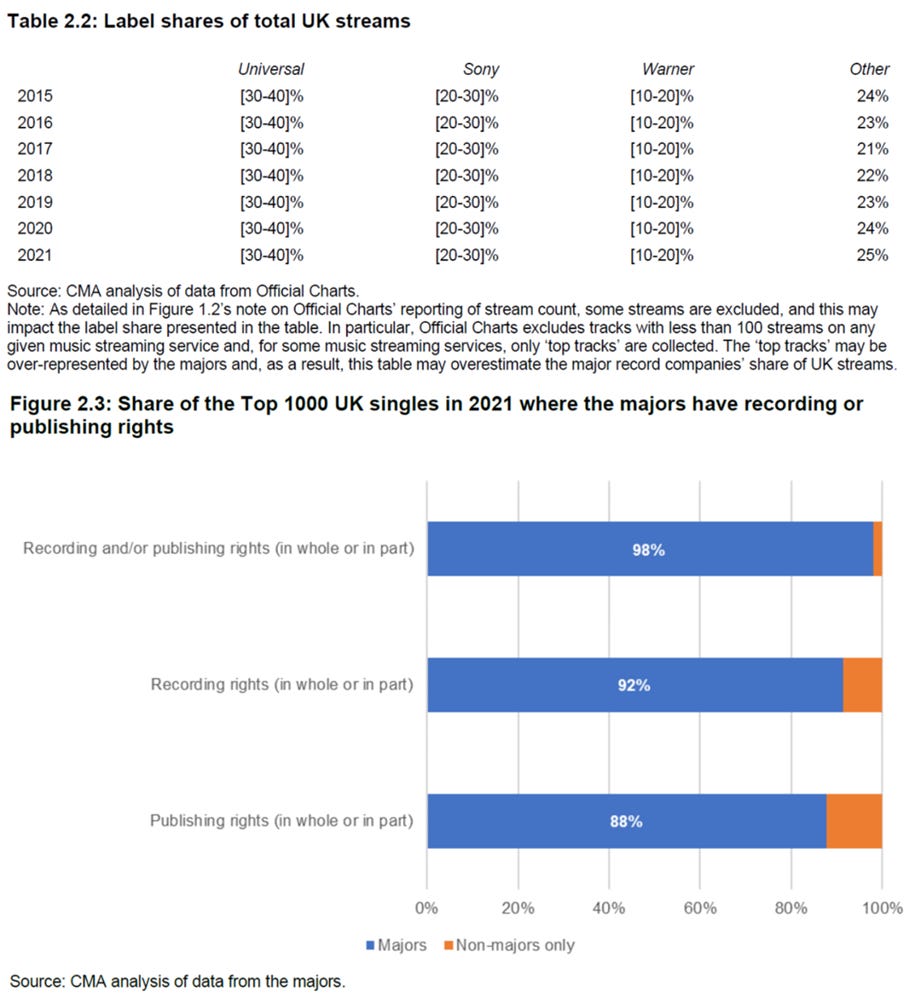

Apart from the dependence derived from the “full catalogue” model, SPOT is also rather dependent in terms of content on the major record labels: “In 2020, roughly two-thirds of Spotify's global streamshare came from music distributed by the major record labels”. It is rather telling for instance the share of streams that major record labels represent for streaming services (and how stable it has remained over time) and the share that they represent in terms of recording or publishing rights in the top hits (the chart below refers to UK but is likely translatable):

As the importance of streaming revenues increases, there are fewer incentives for record labels to reduce its prices, as those reductions will have little or no effect on demand (in opposition to the case of physical sales) and will not ultimately “led consumers to listen to more of that record company’s repertoire”.

Major labels and rightsholders are expanding their opportunity landscape and doing a great diversification work, and becoming less and less reliant on music streaming services. The importance of new platforms like TikTok, Twitch, Triller and other social networks are reducing its dependence on music streaming services and so damaging the bargaining power of music streaming services even more. Those emerging platforms have contributed just 5% to the global music industry revenues in 2021 but it’s predicted to reach 12% by 2030.

As commented in previous paragraphs, SPOT’s growth is expected to be skewed to ad-supported users and this could also negatively affect long-term gross margins, as “premium gross margins are higher than the free business gross margin”. The Company has made clear many times that the advertising business “should be north of 20% and possibly even higher than that over time” (from the current ~12%).

Finally the cost structure of the music business is rather variable for music streaming services (like SPOT) and costs increase as revenues grow. The deals between rightsholders and streaming platforms are commonly revenue share arrangements: record labels get a percentage of both subscription and advertising revenues. This makes rather difficult for gross margins to improve as the business scale (in contrast to the case of the agreements between record labels and publishers with songwriters and performers where fixed costs represent the most relevant part).

As music streaming services grow in scale and become a more important source of revenues to record companies, there might be some scope to negotiate contractual terms and improve gross margins. However, competition is increasing and the range of music streaming services is growing. All these factors point to the difficulties for Spotify to meaningfully expand the gross margin of its core music business.

Being said that, what about launching new activities or verticals? SPOT has clearly stated its intention of developing its marketplace business, which according to the Company “isn't helping margins, it's actually helping margins a lot”. Additionally, SPOT has made rather clear its ambitions in terms of new verticals, with the increasing focus that is devoting to podcasting and the recent launch in September 2022 of its audiobooks vertical. Besides they announced in the Investor Day that “in the next ten years, there are additional markets and verticals that (they) believe are natural fits for (their) platform and audience” in fields like news, sport or education. All these new verticals are expected to significantly improve its margin profile to finally achieve its targeted 40% gross margin.

This increasing focus outside the core music business is encouraging. As it can be observed in the chart at the beginning of this paragraph, verticals like podcasting and “other” are much more attractive in terms of margin profile. Those are verticals where it is more common independently produced and user-generated content and where, specifically in the case of podcasts, Spotify is starting to produce and acquire more original content, which offers better margins.

The problem with all these new activities and verticals is that nowadays represent a tiny part of SPOT business (e.g. podcasting represented just ~2% in 2021) and most of them are show-me initiatives that requires much more investment and evidence about their future trajectories. In the case of podcasting, for instance, many investments have been made during the last years, acquiring companies and content, but during 2022 there have been also many layoffs and shows cancellations. This doesn’t mean that Spotify won’t thrive in this business, but that there is still a lot to prove and that the road is rather unclear. SPOT’s expectations imply podcasting opportunity increasing almost 7x (from $3bn to $20bn) and this requires a huge expansion in terms of listeners, content and monetization. In general terms a relevant part of its expectations are based on those verticals that nowadays provide zero or little revenue to the business and markets that barely exist (e.g. audiobooks).

In conclusion, taking into account the relevant difficulties to increase its music gross margins and the early stage of the other verticals, I would be rather skeptical with SPOT’s gross margin targets.

Operating Margin Expansion

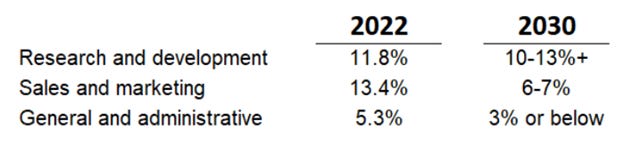

In terms of operating margin, at first glance the goals might seem again achievable:

In the case of R&D, now SPOT establishes an objective a little bit more optimistic than the previous long-term guidance (i.e. 12-15%), but rather in line with the current levels. The Company doesn’t expect meaningful reductions (in percentage terms) as they continue to invest in the business. They have made clear several times that their intention is to continue “making product improvements or product innovation” and “to continue to invest aggressively there”.

The operating leverage is expected to arise from the side of sales, marketing, general and administrative expenses (SG&A). As the Company keeps growing and entering new markets there will be little leverage. Once the Company has reached sufficient scale and can better calibrate its infrastructure needs, they expect to start seeing some operating leverage. However, there is little information about how the Company expects to reach those target levels. The objective is more based on the generic idea that during the growing phase of a company it is common to prioritize growth in order to achieve scale and not efficiency, with the hope that there should be a “natural” operating leverage in more mature stages. In other words, it is expected the Company to keep expending substantial resources as it expands the business, but over time this variable cost structure to become more fixed and this to create a relevant amount of operating leverage.

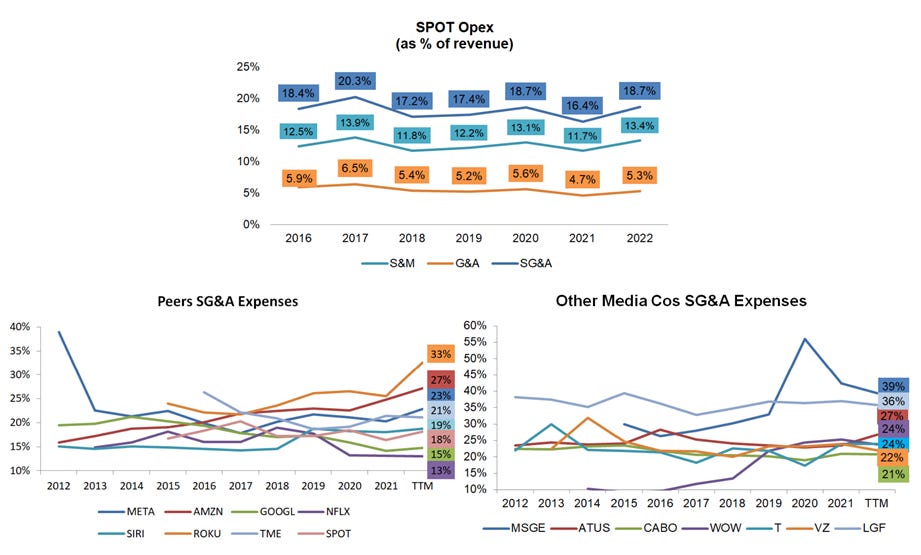

However, in order to have a better idea about the potential evolution of SG&A expenses, let’s have a look to recent SPOT data and other companies that could provide some hints:

Making clear that looking at a company that is in its growing phase like SPOT may be misleading, as it can be observed, the reality is that almost during a decade the Company has not provided any indication of potential operating leverage.

With regard to its peers and other media companies, with the caveat that those data need to be taken with a grain of salt due to different business models and potential differences in terms of calculation, at least they can provide some ideas about the future of SG&A. First of all, it is rather clear that there is not a “natural” tendency downwards, even in companies that could be considered in more mature phases than SPOT (e.g. SIRI or AMZN). So entering in a more mature phase with lower growth doesn’t per se guarantee operating leverage and, in that sense, it would be great for SPOT to provide any hint about how they expect to reach its efficiency targets (besides the mere slowing growth).

Secondly, none of the companies depicted in the chart have been able to achieve SPOT’s 10% SG&A target any of the years (NFLX is the closest one with a 13%). This doesn’t mean that SPOT will not be able to achieve those levels, but reflects the difficulty of that goal.

All in all, we are again in front of good intentions but without any hint that this could be reached and with no clear path to achievement.

Final Thoughts

There is no doubt that Spotify is a wonderful application and a fantastic product, and the Company is doing a great job creating a virtuous cycle of improving the user experience, increasing the engagement and stickiness of its product, reducing the churn and lengthening the LTV of its users, and increasing its resources to keep improving.

The problem is that there are some issues that invite to be really cautious with its ambitious goals. First of all it is rather unclear how the Company will keep increasing its revenue at the current rates. Most of its established markets have room to keep growing, but they are starting to be in a mature stage where most of the people interested in this technology have already adopted it and those that haven’t are not expected to massively change their mind. In that sense growth will probably keep decelerating.

In the case of emerging markets the capacity to grow is much bigger and it is expected to explode in the following years. The penetration is really low in many of the most populated regions around the world and this will probably change with the continuous adoption of smartphones. The problem with those regions is not about growth, but about ARPU, and this leads us to the second problem.

Despite the expected growth in terms of users, mainly thanks to emerging markets, it will be rather difficult for the Company to meaningfully increase its ARPU. In the established markets the Company will need to make a much harder effort of differentiation in order to justify a meaningful increase in the price of its services. Nowadays its core music business is rather similar to the one offered by its competitors and so, despite the stickiness of its product, the Company would have serious difficulties to really increase its prices. Being true that the many new verticals that plans to exploit could create a unique user experience, but this would require, in my opinion, much more evidence. Nowadays most of these new initiatives are tiny parts of the business or just elucubrations. Besides its main competitors have little pressure to increase their prices as they have other businesses that can subsidize their music businesses and this creates even more pressure to keep prices contained.

In the case of emerging markets, subscription prices will be much lower than in established markets and there will be much more ad-supported users. All this will probably put even more pressure on ARPUs.

In terms of margins, the situation is also worrying. Gross margins in the core music business will be rather difficult to increase due to the power of the major record labels. The objective is to increase gross margins through new verticals but again this is something the Company is far from reaching and nowadays those are mainly show-me initiatives. With regard to operating leverage, SPOT expects to heavily improve its SG&A levels, but again the path to reach the objective is rather unclear and looking to some peers is easy to realize how difficult achieving those targets will be.

All in all, regardless of considering Spotify a great product, I don’t think the business provides a compelling opportunity. There is no doubt that if the Company finally succeeds the prize will be huge, but in my opinion the path to reach its ambitious targets is nowadays rather unclear.