Sleep Number ($SNBR): Perfect Example of Growth at a Reasonable Price

Sleep Number ($SNBR): Perfect Example of Growth at a Reasonable Price

In a nutshell

SNBR is a premium-mattress company specialized in “smart” beds and focused on technology innovation.

The Company has been steadily growing (well above industry levels and gaining market share) during the last 12 years, expanding 4x its stores fleet while maintaining its profitability.

The Company exhibits strong pricing power, being able to continuously increase its units sold while constantly increasing its ARPU.

SNBR produces strong FCF (>10% FCF yield) and keeps a healthy financial position (financial debt ~2x EBITDA).

SNBR promotes a shareholders-friendly capital-allocation policy and has been enhancing its ROIC year by year (with ROIC>30%).

Additionally, it enjoys many tailwinds and optionality that will probably make this positive trajectory to continue.

SNBR is trading at very reasonable levels (10x EV/FCF and 8x EV/EBITDA) and might have a relevant upside even under rather-conservative assumptions.

(it is recommended to read this post directly in Substack since it is too long for email and might be truncated)

What makes SNRB an interesting company?

Sleep Number (SNBR or the Company) defines itself as a company with the “mission of improving lives by individualizing sleep experiences” and whose “purpose is to improve the health and wellbeing of society through higher quality sleep” (Form 10-K). First impression: SNBR sells mattresses, bedding and pillows, and this means that belongs to a commoditized industry with price-sensitive customers looking for bargains, deals with low-frequency-transaction durable goods and has low customer engagement. First feeling: forget it and move on.

However, there are some specific aspects that invite to dive a little bit deeper on SNBR’s business model and that ultimately make the Company stand out among its peers:

SNBR is a premium-mattress company specialized in “smart” beds and focused on technology innovation.

SNBR seeks to capitalize on the increasingly popular health-and-wellness consumer trend and, specifically, on the ever-more-widespread consciousness about the connection between health and good sleep. In that sense, the Company has based its strategy since the very beginning on product innovation and in 2016 started its transition from a manufacturer of adjustable-firmness beds to an exclusive provider of “smart” beds. These “smart” beds provide an individualized and totally different sleeping experience as they automatically adjust its characteristics on real time depending on current sleeping conditions and thanks to its incorporated sleep tracking technologies.

Besides, the Company has created the SleepIQ technology platform, which tracks a person’s sleep (each morning users receive a score that reflects the quality of their rest), offers sleeping insights and makes suggestions for achieving a better sleep and overall health.

SNBR bets on lifelong customer relationships.

Historically, mattress companies, selling durable goods, tend to exhibit low customer engagement. SNBR is trying to disrupt this traditional flaw by increasing customer interaction and cultivating a strong brand relationship, and do that mainly through its SleepIQ platform. The seamless and long-lasting communication that this platform provides creates highly engaged and retained customers, and helps to boost satisfaction and increase sales by repeats, referrals and upgrades.

Indeed these customer relationships help to create a kind of flywheel effect. SNBR, with more than a million sleep sessions and billions of biometric data added daily, is creating a huge sleep database. This database, through AI and analytics, allows the Company to provide personalized insights and better sleep to its customer, and to create new software features. This continuous interaction and improvements of SleepIQ platform is expected to increase customers’ engagement and happiness, which in the end should mean more customers and more data.

SNBR operates with an exclusive direct-to-consumer approach.

This is a rather different approach with regard to most mattress companies. There are basically two kind of mattress companies: on the one hand, traditional companies that mostly sell through other third-party retailers, and, on the other hand, online retailers with no or little physical presence (i.e. bed-in-a-box brands).

SNBR may be considered the only one with an exclusive direct-to-consumer approach. The Company takes care of the whole manufacturing process and sells directly and exclusively to its customers through its own physical stores (together with the online channel). This approach enables higher engagement and interaction, brand and customer-experience control and ultimately highly productive stores.

SNBR operates with a vertically-integrated business model.

As anticipated in the previous point, SNBR controls the whole process, from sourcing, product design and production through fulfillment, sales and delivery. This characteristic allows the Company to control quality, cost, price and product deployment, and is helping to mitigate the impact of the current supply chain constraints.

Besides, the modular design of its beds works with a “just-in-time, build-to-order production process” which requires minimal inventory and results in reduced working capital levels (see next paragraph’s point 5).

What else?

Apart from all these points that differentiate SNBR from its peers, there are many other aspects related with its performance and projections that makes the Company really attractive. Let’s have a look to all these aspects:

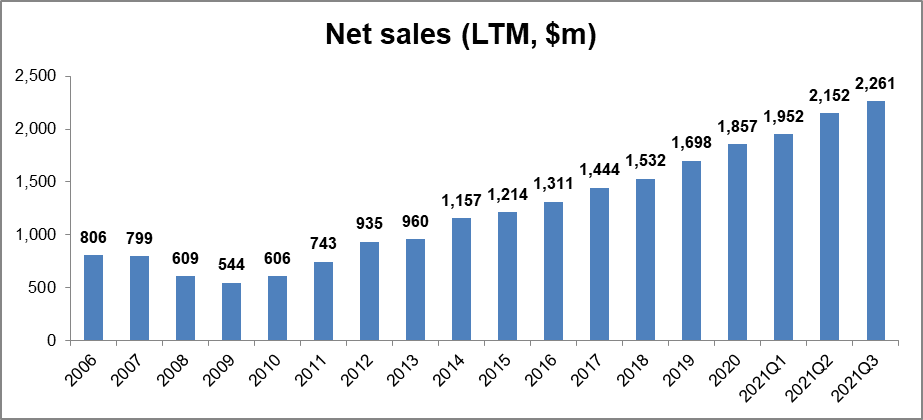

SNBR has had an impressive revenue evolution during the last fifteen years.

The Company has been steadily increasing its revenues and has quadrupled its net sales since its lows in 2009:

This means basically 7%+ CAGR during this 15-year period and 12% CAGR since 2009 lows, and well above the 4% industry level (see below the industry paragraph). Moreover, the Company expects to keep a annual mid-to-high single-digit growth at least in the foreseeable future (see SNRB Investor Presentation October 2021).

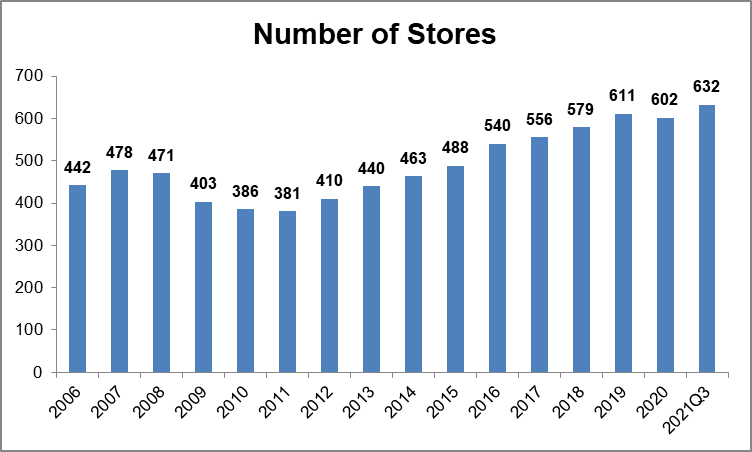

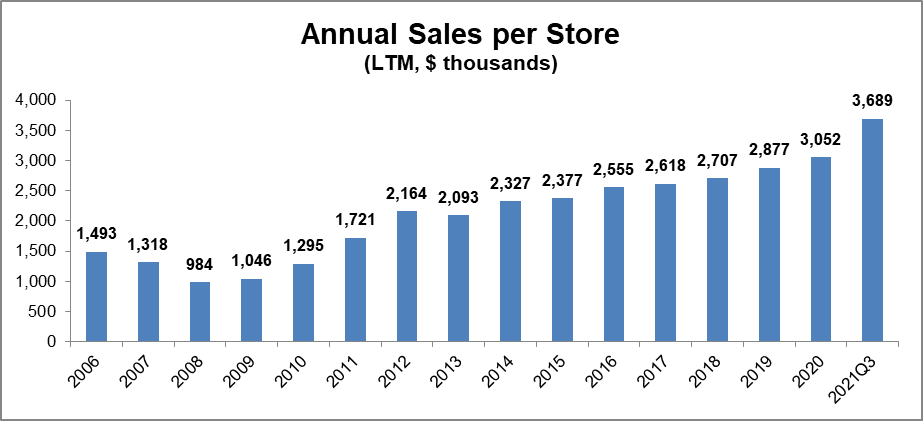

SNBR’s revenue performance is the result of a healthy mix of store fleet growth and revenue per store improvement.

The Company has been able to steadily expand both its store fleet and its revenue per store (see also point 3 below):

In addition, the Company expects to keep growing its store fleet by 4-5% CAGR through 2025 (see SNRB Investor Presentation October 2021).

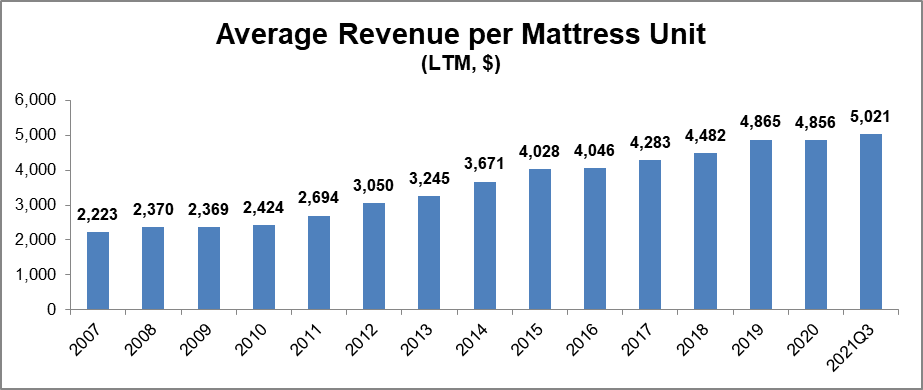

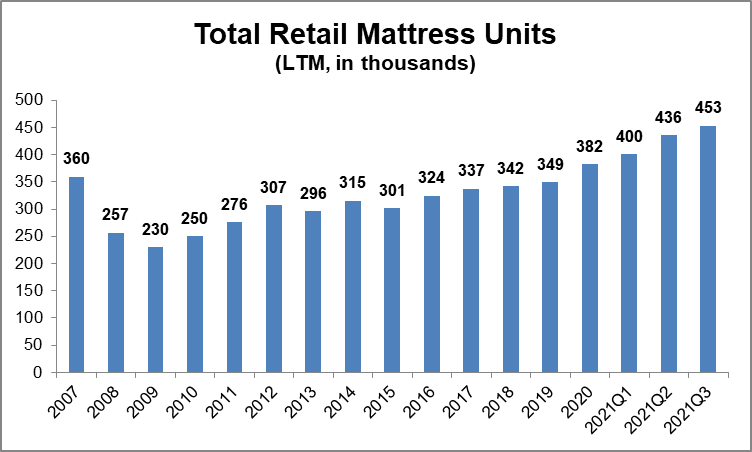

SNBR has a strong pricing power.

During the last years the Company has been able to steadily increase the price of its products without negatively impacting either its customers’ base…

… or the number of mattress units sold:

Within the current inflationary environment, pricing power is one of the most relevant features in a company.

SNBR is being able to transfer this top-line improvement to the bottom line, leveraging its cost and capital structures.

The Company has been able to convert this 7%+ CAGR in revenues during the period 2006-2021Q3 into a 7.2%, 8.7%, 10.3% and 15.9% CAGR in terms of gross profit, operating profit, net income and diluted EPS, respectively:

After the Great Financial Crisis, the Company had some bumpy years due to investments and transitional costs (e.g. new ERP system, 360 smart beds, supply chain improvements…), but since 2016 it has been improving all its operational metrics.

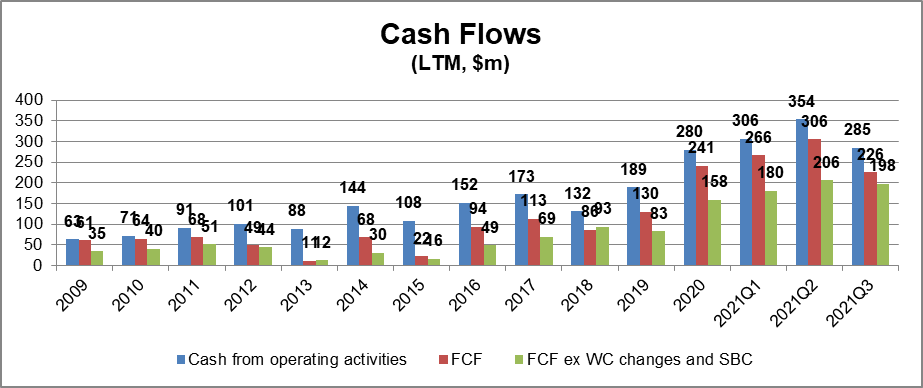

SNBR presents a (rather) strong financial position and is able to generate strong and increasing FCF.

In line with the previous point, cash flows have been also steadily improving during the last years (even using different metrics):

Apart from “Cash from operating activities”, this chart depicts two different FCF metrics: 1) FCF defined as Cash flow from operations minus CapEx (purchases of property, equipment and intangibles) and 2) FCF before Working Capital changes and Stock Based Compensation, which is the same metric but eliminating the impact of WC changes and SBC. This second measure is a more stable cash flow metric that eliminates the effect of short-term jumps in current assets/liabilities and that takes into account the impact of stock based compensation.

In any case, whatever the FCF metric, it is clear that SNBR has been able to steadily generate FCF and has been clearly improving its cash generation during the years. It is true that it is still early to see what will be the impact of eliminating the disruptions caused by the COVID pandemic and all the stimuli provided during this period, but SNBR’s growth trajectory invites to be optimistic.

Additionally, thanks to this stable FCF generation and its efficient just-in-time model (see point 3 in previous paragraph), the Company is able to operate under a negative working capital condition (i.e. it can use the money of its vendors to fund its inventory):

SNBR promotes a shareholders-friendly capital-allocation policy.

SNBR basically follows two guidelines for its capital-allocation policy: 1) invest in the business as long as shareholder value can be created (i.e. ROIC over WACC) and 2) return the remainder of the capital to the shareholders (mainly through stock buybacks).

In that sense, the Company has been steadily investing in the business (see point 2 above related with the store growth) with a clear positive impact on its return on capital (see below point 7), and increasing the amount devoted to stock buybacks, to the point that in the last year this amount even exceeded the cash generated by operating activities:

As it can be observed, the Company has been aggressively reducing its shares count. This is the appropriate policy whenever SNBR’s stock price is below its intrinsic value and has helped to boost EPS (see point 4 above). However, during the last years the Company has been increasing the amount of debt in order to keep up with the stock repurchases (“given the strong growth in the business and currently favorable banking conditions”). They mentioned in the last conference call that “still, (they) are maintaining a relatively conservative leverage stance and ended Q3 with a debt-leverage ratio of 2.2 times EBITDAR. Longer term, (they) expect to operate with leverage of 2.5 to 3 times EBITDAR”, however, this is something that needs to be carefully monitored, as this might be considered a somewhat aggressive approach.

SNBR has been enhancing its ROIC year by year.

During the last years, and as a result of the shareholders-friendly capital-allocation policy mentioned in the previous point, the Company has been able to keep its invested capital rather stable and simultaneously increase its NOPAT, making the ROIC to soar:

SNBR prioritizes innovation and R&D expending.

SNBR is convinced that one of its main competitive advantages it to be the leader in sleep innovation and allocates a relevant amount of its resources to R&D activities:

SNRB has been steadily increasing R&D expenses, both in absolute terms and as a percentage of revenue. Nowadays the Company assigns 2.5% of its revenue to research and sleep science, compared to its main competitors that allocate less than 1% (e.g. Tempur Sealy International or Purple Innovation).

SNBR’s customers love its products.

Analyzing products and stores reviews through Internet is always something to take with a grain of salt. However, looking through many sources and gathering information through different websites is something that at least can provide some feeling about how customers think about a company’s products.

In the case of SNBR, and after reading many of the reviews from its more than 600 stores, most of the comments highlight that stores’ staff is helpful and knowledgeable, making the customer experience to be great, and that their beds are expensive but absolutely wonderful and worth the money.

SNBR enjoys many tailwinds and optionality.

Apart from all the positive aspects mentioned above, there are additionally many issues that can help the Company keep this positive trajectory in the following years:

Awareness about the importance of sleep quality for a healthy life is on the rise and this structural shift in consumer attitudes and behaviors related to sleep health is likely to continue (within the more broad health and wellness movement that have been accelerated by COVID-19).

Elderly population along with rising prevalence of sleep disorders are unquestionable facts. Aging population is a relevant factor for the Company as “health-related challenges are the primary purchase trigger” for 55+ age group to purchase a new bed “in the hopes that it will help them manage health issues”.

Consumers are adopting digital products and connected services at a much faster and higher rate (which have been also accelerated by COVID-19). The rising penetration of smartphones and high-speed internet will keep boosting the demand for connected devices.

SNBR has captured and tracked more than 11 billion hours of sleep data gathered from more than 1.4 billion sleep sessions through its SleepIQ technology. This huge database might help the Company to pursue new adjacencies and opportunities in the sleep health economy (e.g. connected sleep health, connection with integral health treatments, integration with insurance initiatives).

Internationalization. Till now, SNBR has basically circumscribed its business to the United States (with shipping to some other North American areas). However, they have mentioned in some conference calls that their “vision is to become one of the world's most-beloved brands by delivering an unparalleled sleep experience, and that's certainly much broader than the U.S. and an important part of (their) growth strategy over the next few years”. Should the Company finally decides to pursue this objective, the opportunity would be huge.

What about the mattress industry?

As commented in point 3 of first paragraph above, there are basically two kinds of mattress companies: traditional manufacturing companies distributing through third-party retailers and online retailers with no/little physical presence. According to SNBR’s February 2019 presentation, this is roughly the composition of the industry:

Within the group of traditional manufactures, the US industry is highly concentrated among few players, with Serta Simmons Bedding and Tempur Sealy International ($TPX) enjoying over 30% market share each one of them (Tempur has gained some market share since 2019 at the expense of Serta Simmons).

Online retailers is a much more fragmented group with numerous direct-to-consumer companies offering “bed-in-a-box” products, primarily through online distribution (e.g. Casper Sleep, Purple Innovation, Saatva, Leesa Sleep) though many now partnering with traditional mattress retailers (e.g. Tuft & Needle with Serta Simmons or Nectar Sleep with Mattress Firm). This group represents around 8%/10% of the industry.

SNBR, according to its Form 10-K, has an “estimated 8% market share of industry retail revenue” and ranks “as the 5th largest mattress manufacturer and 2nd largest U.S. bedding retailer”.

Additionally, within these groups, it deserves special mention the subgroup of smart mattress companies. This group comprises all the companies that, one way or another, are focused on or are moving to sleep-tech solutions. The smart mattress market is rather concentrated among few companies, some of them tech-natives (e.g. Eight Sleep, Naturaliterie, ReST) and other more-mature companies (e.g. Serta Simmons Bedding, Sleep Number, Tempur Sealy International).

But what about the financial health of the industry? According to the International Sleep Products Association (ISPA), the industry has grown approximately 4% annually over the last 20 years, including 4% annually, on average, over the past five years (SNRB 2020 Form 10-K). Besides, as commented in the ISPA’s latest report, the growth is expected to continue by healthy percentages over the next few years. This Association projects growth in mattress and foundation value of 8.5% for this year, and 4.5% for 2022 and 2023. In the report they mention many indicators that invite to be optimistic: increase in disposable income, rebound in economic activities from the pandemic, strong growth in the housing market and GDP… Even as they also comment some expected cooling down and lower stimulus, this should not sour the growth trajectory.

Notwithstanding, as I will comment in the risks’ section below, there are some concerns that deserve specific attention, as are the uncertainties created by the pandemic (inflationary pressures, supply chain disruptions, etc.) or the cyclical condition of the industry, but nowadays there are no specific factors that suggest this indsutry should be discarded.

What about the risks?

Till now I have mentioned a lot of positive aspects with regard to the Company and to its industry as a whole. However, it is important to highlight that of course this company is not risk free and there are many issues to take into account before jumping into this investment opportunity:

Cyclicality and macroeconomic factors.

SNBR is a cyclical company and this means that macroeconomic factors play a key role in its evolution. Housing market, consumer confidence, consumer spending or household formations are some of the factors highly correlated to the bedding industry. These are factors that are outside the company’s control and that could have a relevant impact on its performance. As mentioned when I talked about the industry, there are no specific concerns about these economic factors in the near term, but these are issues to follow closely.

Inflationary pressures.

Nowadays, within those macroeconomic factors affecting the industry, inflation might be the most relevant. SNBR is not immune to this economic phenomenon and is being impacted by rising commodity, labor and freight costs. However, it is under those circumstances when the relevance of pricing power shows up. There is no doubt that SNBR is being affected by inflationary pressures, but it is being able to transfer part of these price increases to the customers, helping to absorb the impact (see point 3 of second paragraph).

Supply chain disruptions and electronic supply shortages.

SNBR, as many other companies across many industries, is suffering supply chain disruptions and shortages of semiconductors and other electronic components. As they commented in the last conference call, “this is creating uncertainty in fulfillment, timing and costs”. However, they consider these constraints to be temporary and they are “utilizing multiple levers across sourcing, product design, fulfillment, sales and service operations” to mitigate the impact.

Increasing debt levels.

Historically SNBR has operated without financial debt. However, since 2017/2018 the Company decided to take advantage of favorable banking conditions and start to use its cash available under a revolving credit facility, accelerating simultaneously its stock repurchase program. Currently the Company bears $359m in outstanding borrowings, which is perfectly manageable and within its targeted leverage of 2.5-3x EBITDAR. However, this is something to closely monitor, specifically taking into account that the FED is taking steps towards rate hikes and it is expected a higher-interest-rate scenario in the near future.

High competition.

The retail bedding industry is considered highly competitive and there are many players in the sector. Each and every day new companies appear in the market, specifically in the online bed-in-a-box subsector, which presents rather low entry barriers (indeed it is considered that there are almost 200 companies in this specific segment). However, in general terms, SNBR’s situation within the industry is rather favorable, with a differentiated business model and a healthy and growing market share.

What about valuation?

SNBR is a company steadily growing and profitable during the last 12 years; it is expected to keep growing above industry levels and improving its profitability metrics; it is producing strong FCF and keeps a healthy financial position; it enjoys many tailwinds and has a lot of optionality; it is taking care of its shareholders and is beloved by its customers… and it is currently trading at approximately 10x LTM FCF and 8x LTM Adj. EBITDA. In general terms, it doesn´t seem really expensive, but let’s make some (rough) calculations and comparisons in order to confirm (or discard) this first impression.

Let’s start with a Discounted Cash Flows approach (DCF). I don’t really believe in making big and complicated models, full of data and hypothesis, when I think in terms of DCF. My intention is not to achieve the most accurate figure, but just to be sure that the Company is not overvalued and to have a rough idea of its potential upside using conservative inputs. In the case of SNRB I have made the following assumptions:

FCF of $198m as starting point, which is the LTM FCF in Q3 2021 (ex WC changes and SBC). The Company plans to keep growing and there are no specific reasons to think that this won’t be the case, so this should not be an aggressive starting point. Besides, this figure is lower than the “official” FCF of $266m (which includes WC changes and SBC).

WACC of 7%, which is the figure the SNBR internally uses.

Three different scenarios:

Scenario 1: no FCF growth.

Scenario 2: 4% FCF growth, in line with historical Industry growth. This growth applies just for the first 5 years and then it is assumed no growth.

Scenario 3: 10% FCF growth, looking for a figure below but closer to the FCF growth CAGR of the Company during the last 12 years (16%). Again, this growth applies just for the first 5 years and then it is assumed no growth.

As it can be observed, even taken the most-conservative Scenario 1, which assumes zero growth from now on, the Company might present an upside of 43% from the current levels. If we look to more optimistic scenarios (but well below the Company’s recent history) the upside might be over 100%.

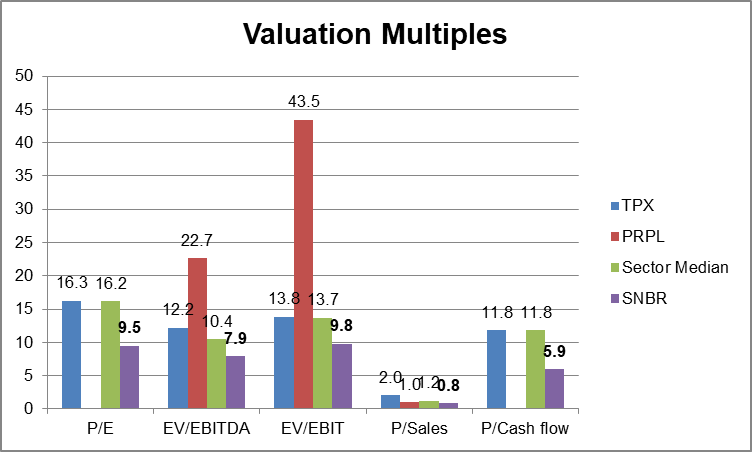

Let’s now compare SNBR with some of its peers, though making this comparison in the case of SNRB is not an easy task due to its specific business model and the lack of comparable public companies. There are basically just three US public pure-mattress companies: Tempur Sealy International ($TPX), Purple Innovation ($PRPL) and Casper Sleep ($CSPR). I discarded Casper Sleep because the absence of profitability makes its metrics useless. Let’s see the comparison with the other two companies (and the sector median):

Looking at the chart, SNBR seems to be the most inexpensive company among its (few) peers and whatever the multiple.

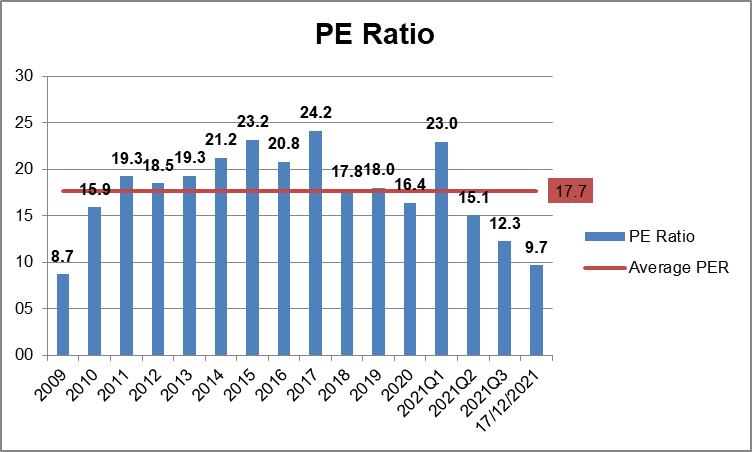

We can also have a look to the historical valuation of the company, at least to have an idea about how SNBR has been valued during the past. Let’s look at the evolution of its PE ratio:

Again, the company seems to be trading at an attractive valuation compared with its historical figures.

So this is a company that seems to present a relevant upside and that is trading at reasonable multiples, below its peers and sector levels, and well below its historical valuation. All in all this seems to be the perfect example of a quality company at a reasonable price.

Thanks for this. How do you feel about the class action lawsuit related to the supply chain disruption of 2021? I noticed a flurry of press releases from Dec 30 accusing SNBR of material misrepresentation of steps it took to address foam supply. I like everything else about the company and support your thesis, but litigation is no fun. I know there's a whole industry devoted to suing companies in America, so many of these suits are frivolous.