Kirkland’s, Inc. ($KIRK): A Turnaround Story In The Making

Kirkland’s, Inc. ($KIRK): A Turnaround Story In The Making

In a Nutshell

Kirkland’s (KIRK) is the perfect example of a turnaround in the making: heading in the right direction but still in progress.

Coming from years of steady deterioration, since 2018 a new management is making a really good job trying to reverse this situation: improving product assortment; rationalizing the store footprint and employee base; expanding gross margins; reducing operating costs; and optimizing the logistic structure and supply chain.

However, KIRK is in the eye of the storm of this macroeconomic environment (low-income customers and home furnishing sector) and, maybe more importantly, is not being able to revert its customer traffic problem and find the market niche for a successful long term.

Many work ahead, but if the company is finally able to complete the transformation, the opportunity might be huge.

Introduction

Let me start being rather clear with this company. KIRK is a company within my watchlist (and not yet in my portfolio) because I do like its recent evolution and management skillset, but at the same time I think it is still a company pending to demonstrate that it is able to keep the good job that has been doing during the last years. Additionally, it is one of those companies that is in the eye of the storm of this macroeconomic situation as its customer target is composed mainly of low-to-mid income customers and it is part of the home furnishing sector, one of the sectors that is suffering the most. If that were not enough, this is a turnaround story still in progress and so a high-risky business where it is probably wiser to stay in the sidelines.

Anyway, I am really interested in these successful stories where there is a struggling company, someone new takes the helm, starts to fix the problems and finally is able to reverse the situation. This is a perfect example of this kind of companies (though still pending to complete the rescue operation). Besides, as we will we see, there is a huge opportunity should the management is finally able to hit the nail on the head and complete the whole transformational process.

What was the situation in 2018?

By 2018 KIRK was a company facing many challenges. KIRK wasn’t able to find its place within the market and was lost in the mare magnum of big box value players, against which it was losing market share. The company was not being able to attract a loyal customer base and its store traffic and awareness were declining. Trying to reverse this trend, it was carrying out inefficient promotional activities and it was damaging its bottom line. It offered a narrow variety of products and it was highly dependent on seasonal assortment. Besides, it was rather inefficient from an operational point of view with a lot of room to lower product cost and to improve its supply chain.

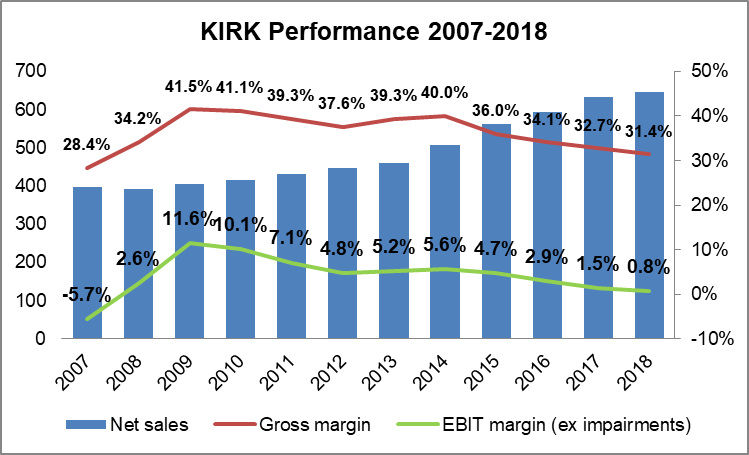

As a result of all these issues and despite the positive evolution of its sales (thanks mainly to a growing store footprint), the Company’s financial metrics were steadily worsening:

In April 2018 KIRK decided to carry out a management transition and hired Steve Woodward as new CEO (effective October 22, 2018). Woodward had been President and Chief Merchandising Officer for three years in Crate and Barrel, a higher-end KIRK’s peer, and previously he was head of the Michael Kors brand of watches and jewelry. He is a well-respected professional and, as he commented in an interview, the main condition he required to accept the position was that he “needed the freedom to make the changes (he) needed to make”. He knew that the transition would be painful but had a clear vision about the changes KIRK required.

What changes did the new management bring?

1. Product revitalization

The new management realized that KIRK had a relevance problem and was not being able to find its place within the home furnishing retail market, fighting a price war with competitors enjoying bigger scales and broader product assortments. They had the feeling that they “were in the wrong place in the spectrum” and that a focus change was needed.

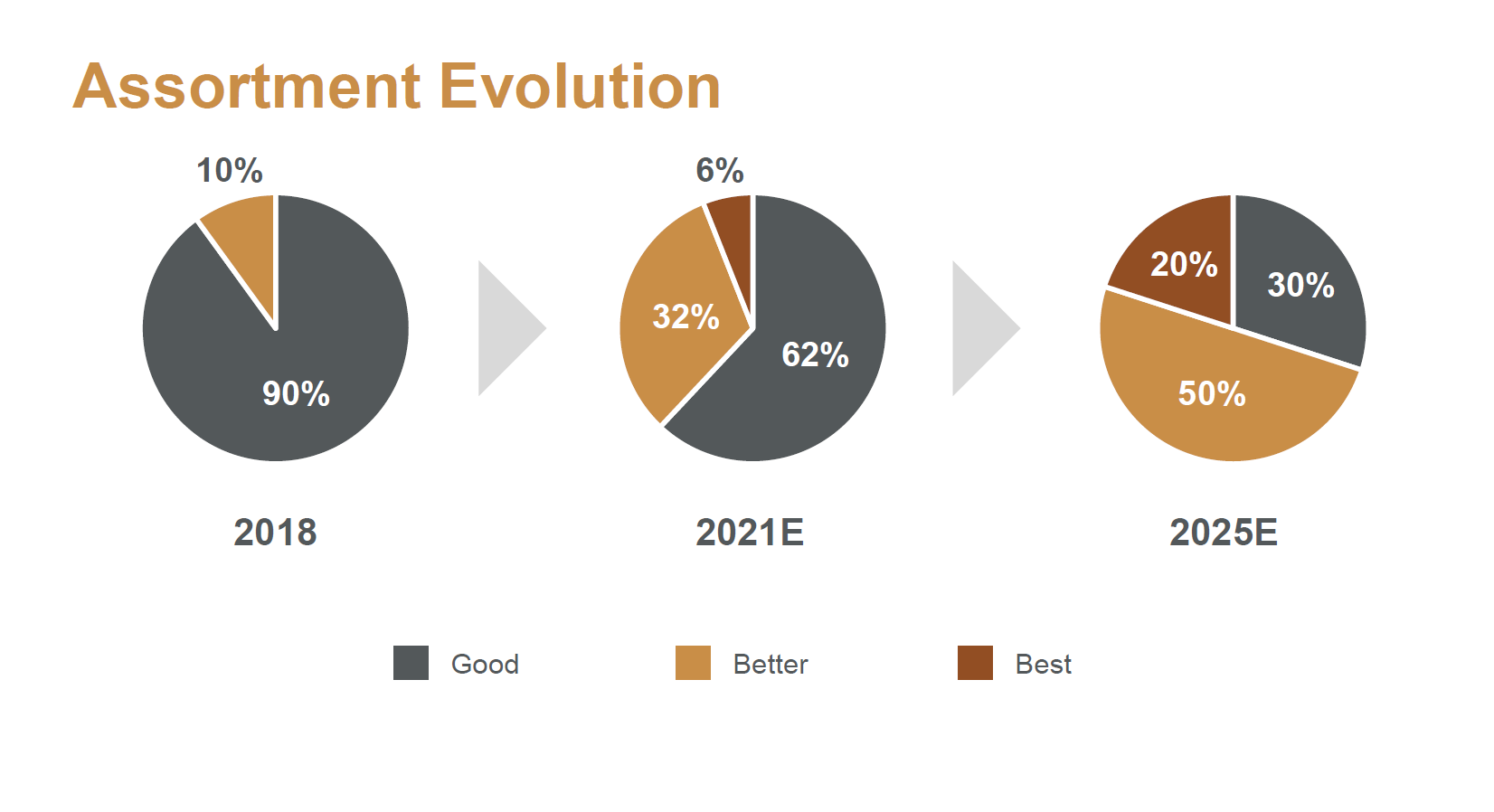

The transformation focused mainly on two strategic goals. On the one hand, product assortment. KIRK had been historically considered as a “seasonal destination category in fall and holiday” where customers go for “final touches”. The new management realized that the Company could thrive in many additional categories and this could hugely expand its addressable markets. They were conscious that there were categories really strong for other retailers that they were not in. In that sense they decided to move the Company from an accessories shop to a one-stop shop for complete home furnishing projects, adding new product categories (e.g. rugs, tabletops, bedding products, larger furniture, upholstery). The idea is to ideally be the place where customers can find everything for their decoration projects and increase the importance of less-discretionary and less-seasonal items. Besides, they carried out a process “of looking at every category and doing a financial look at everything” in order to reduce space in those “oversized” categories and be able to get everything (new and existing categories) within the stores.

On the other hand, the new management wanted to change the customers’ perception of the Company and to transform KIRK into “the best home furnishing in the specialty retailer in the value space”. In CEO’s words: “move away from being coupled with the mass merchant retailers, and fit squarely as the value home retail store within the specialty world”. KIRK was historically considered a low-price retailer where the key attractions were just price and promotions. However, this was an ultracompetitive space filled with big players and where KIRK was becoming irrelevant. New management realized that there could be a much more profitable niche should the company was able to scale through the customer ladder. The idea was simple: without changing the value proposition, try to elevate design and quality, enhancing the relevance to the customer and keeping the value pricing. In other words, try to fill the space that is below the specialty luxury market, but well above big box retailers.

The final objective is to try to keep current loyal customers that look for opening price points, as the Company maintains its value proposition, but at the same time to gradually acquire new high-value customers able to spend bigger amounts and buy higher-ticket items.

These changes should help revitalize the company by increasing its relevance and brand awareness, reverse the customer traffic trend and drive sales and average ticket growth.

2. Merchandise margin expansion

KIRK’s product margins were gradually deteriorating and the management needed to fix this situation. Once again it was decided to work in two different fronts. The first one was the improvement of pricing and promotional efficiency. KIRK was focused on promotional activities regardless of their effectiveness, just with the objective of increasing traffic and top-line growth, but without taking into account the final impact on profitability. KIRK established a price and promotional analytical team in order to “identify the most productive promotions as well as root out the inefficient promotions”. It was important to keep the promotional activity, but it was also important to do it with a systematic approach and as a part of a comprehensive plan to revitalize the company (which in the end meant more targeted promotions). Those measures were expected to have a direct impact on gross margins.

The second front was direct sourcing. They realized that they were “one of the very few retailers left that don’t do direct sourcing” and that direct sourcing might help the Company in many senses and specifically to enhance the costing. They hired a new Director of Direct Sourcing and signed with different agents in China, India and Vietnam. They analyzed category by category to see what made sense to bring directly from the factory. The idea was “moving from the vendor base of primarily wholesalers to a worldwide direct sourcing base”. By 2018 direct sourcing accounted for just 12% of merchandise receipts. This percentage has increased to 36% in 2021 and the Company expects to make up 70% of the assortment by 2025. This change should have a relevant impact in terms of margins as “each item moved to direct sourcing gained on average 500 bps of margin improvement”.

Besides, direct sourcing provides many other additional benefits that in the end are expected to help also improve margins:

It allows diversifying buying opportunities across multiple products, factory options and countries. Specifically it helps to reduce KIRK’s dependence on China and this “should give (them) better opportunities to not be so dependent on one port or one supply chain”.

It provides access to more exclusive and more design-oriented merchandise at better price points and this helps to pull back discounts, as this higher quality and style gives better options to sell at the original prices.

It additionally helps to improve prices of wholesale sourcing: domestic vendors need to fine-tune their price points if they want to compete with direct sourcing.

All in all, the new management rapidly understood that it was necessary to work on margin expansion and not think only in terms of top-line growth, and launched different initiatives to row in this direction.

3. Reinforce omni-channel structure and store optimization

The new management also noticed that a relevant part of the traffic was moving from stores to online and decided to make KIRK’s strategy revolve around the omni-channel platform. This has implied basically two strategic objectives: reinforce the omni-channel experience and store footprint optimization.

In terms of the omni-channel experience, KIRK had already implemented different omni-channel possibilities, launching third-party drop shipping in 2015 and buy-online-pick-up-in-store (BOPIS) in 2018, but the new management has reinforced its importance. They implemented curbside pickup and next-day delivery for online purchases in 2020, and they are now introducing furniture white-glove delivery. They expect e-commerce to keep growing its importance and reach around 50% of net sales in the future (from current 27%).

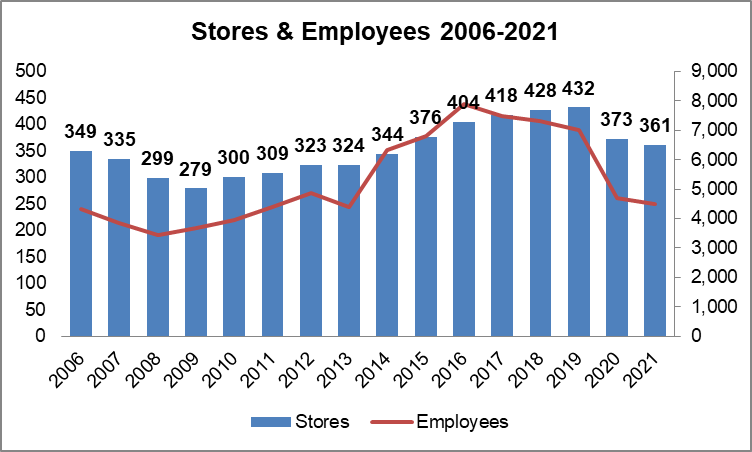

However, maybe the most relevant factor for the omni-channel structure, at least in terms of profitability, is the store footprint optimization. The Company has changed its mind and now thinks about the store as a “critical piece of the fulfillment of ecommerce orders”. This means basically to move the focus and start thinking about the stores not only as points of sale, but also as fulfillment centers for the online orders. This led the Company to carry out a complete review of its store footprint and try to find the structure that better support its omni-channel framework. Simultaneously the Company hired a third-party to renegotiate store leases and reduce the store count by closing underperforming stores and focusing on the profitable ones.

As a result of this process, which is still in progress, the Company has carried out an aggressive rationalization and a reduction of the store count to 361 stores by end 2021 (from 428 by the end of 2018). The final objective is to reduce the store footprint to around 350 stores.

All those measures, together with a new store labor model implemented at the beginning of 2020, have considerably lowered store occupancy costs (included as part of cost of sales) and operating expenses.

4. Supply chain optimization

In line with the previous point, it was also necessary a logistic reorganization. KIRK was working basically with just one single distribution center (DC) in Tennessee and this created inefficient routes that, together with rising transportation costs, were severely impacting its margins. Besides, as traffic started to move from stores to online and the focus moved to the omni-channel platform, KIRK decided to carry out a complete overhaul of its distribution centers and logistics. The final goal was to more efficiently flow the goods through the supply chain and move the e-commerce distribution closer to the consumer.

Currently, apart from the Tennessee DC, it operates with a DC in Texas, two e-commerce order fulfillment centers in Nevada and Virginia, and a third-party operated West Coast distribution operation. These changes have helped to reduce miles to deliver product to stores and customers and improve speed of delivery, and so to lower outbound freight, shipping and distribution center costs.

What has been the impact of all these changes?

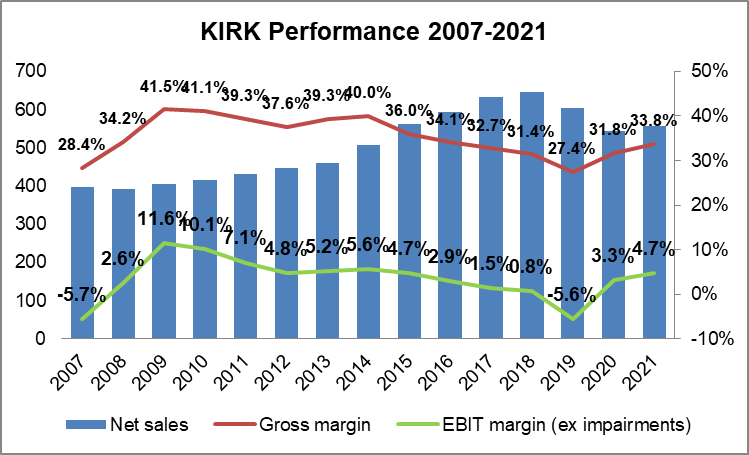

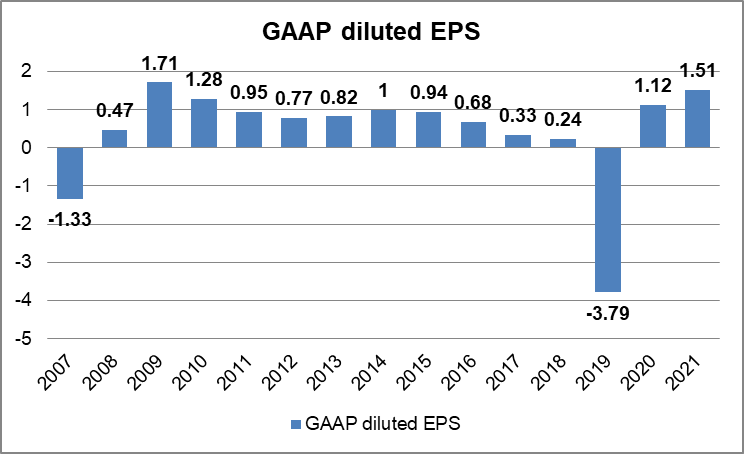

Since the very beginning they were conscious that “the path to sustainable growth will take time” and indeed 2019 was a really difficult year where many of the changes commented above were being implemented but the benefits were not yet visible. The management started to introduce their plans to expand Kirkland’s assortment and reduce operating costs but its full realization would require more time. Let’s have a look again to the chart introduced at the beginning of this article but this time adding the period 2019-2021:

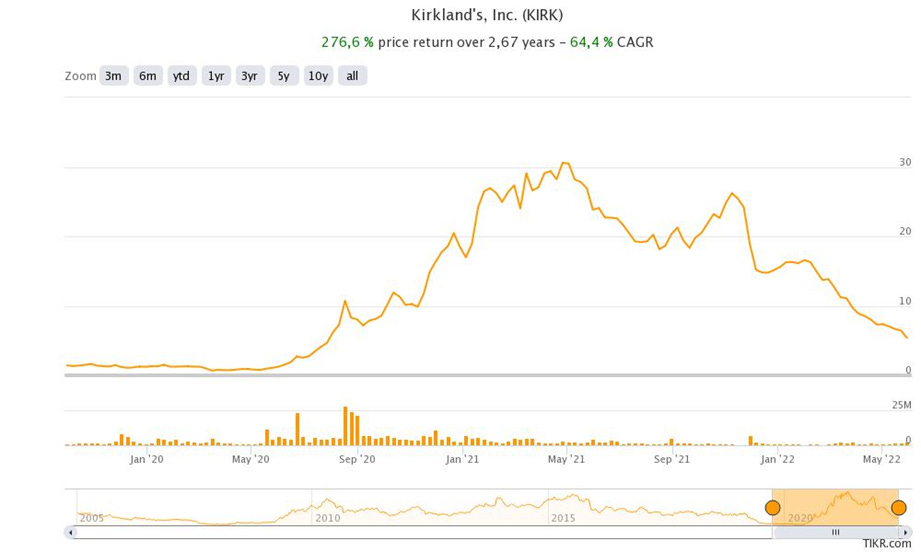

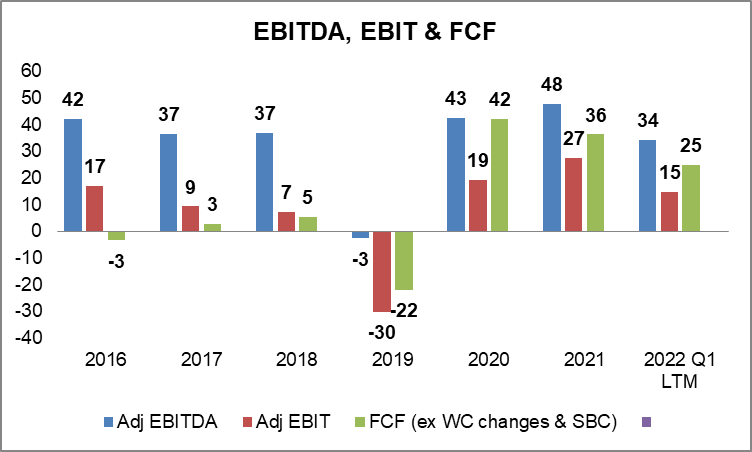

It can be clearly observed that 2019, though a transformational year, was really difficult. Indeed, it is in 2020 when changes seem to have started to make effect and things to head in the right direction. KIRK is now a much more diversified company, in terms of vendors and customers; it has aggressively rationalized its store footprint and employee base; it has renovated its logistic structure and reinforced its supply chain; and it is successfully implementing its direct sourcing strategy. All these measures have had a relevant impact on its financial metrics, both in terms of gross margin and operating expenses, and this have been finally reflected in its earnings and stock price (two aspects that are usually highly correlated):

However, it is important to highlight the recent behavior of the stock price. As it can be observed, after an excellent 2020 and first half of 2021 (with a movement from $1 to above $30!), the stock price started to go down again. I don’t really care where the stock is heading in the short term, but it is important to not underestimate the market as frequently there is a reason behind market movements and those are probably anticipating something. In other words, should the stock price is heading down, it is important to dig into the company in order to see if there is something relevant behind. And indeed this is exactly the case with KIRK and the reason for me to stay currently on the sidelines.

What’s happening since mid-2021?

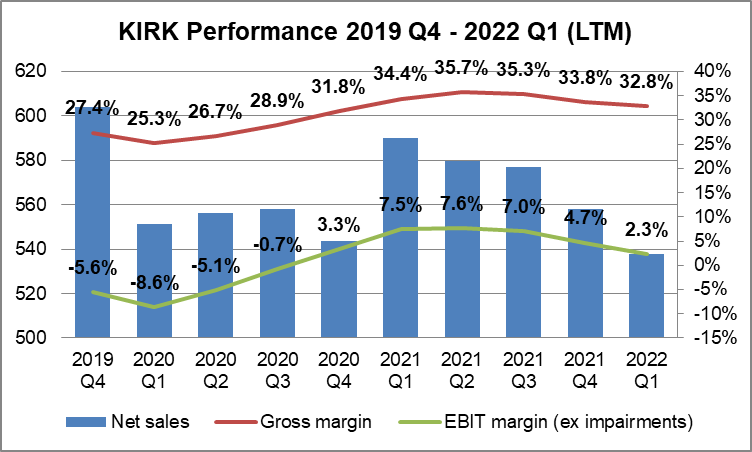

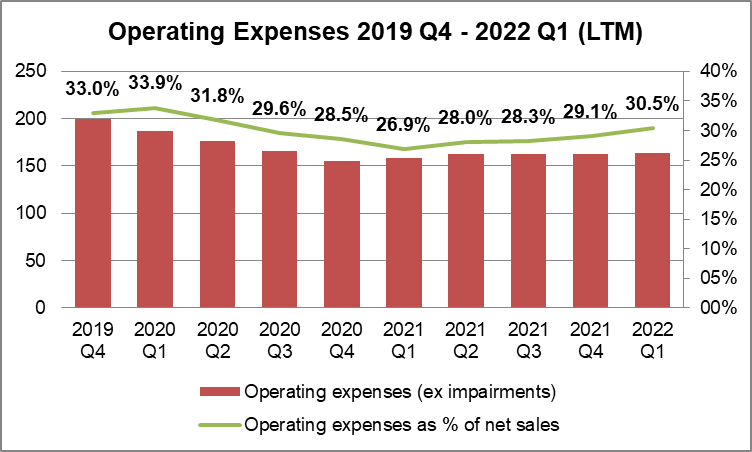

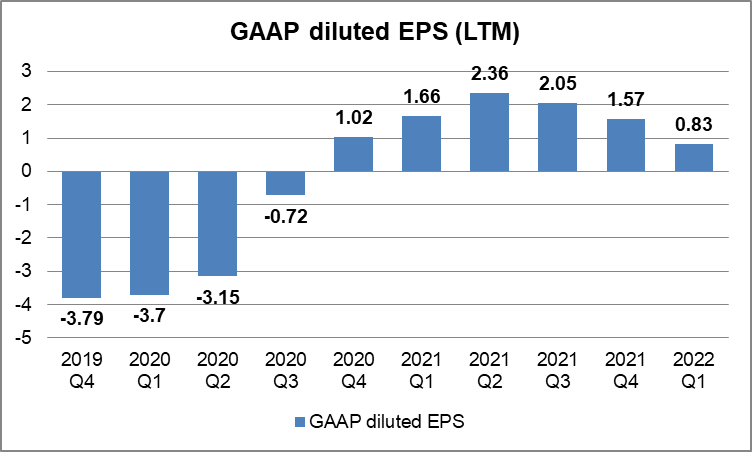

Till now I have provided many charts that depicts KIRK’s story on an annual basis. Let’s look again at some charts, but this time zooming in a little bit in order to see the most recent evolution quarter by quarter (though using LTM data):

Looking at these charts we can observe that the most recent evolution of the company in the last quarters is less promising than the picture provided by the annual figures of the previous paragraph. Margins are starting to suffer again, operating expenses are increasing and EPS are deteriorating.

There are basically two main reasons for this worsening, but in my opinion with different relevance from an investor perspective. The first reason is the general macroeconomic environment. KIRK is not at all immune to the economic headwinds emerging all across the economy and indeed is perhaps one of the companies that could suffer the most. This highly uncertain and inflationary environment, caused by the mix of the still-in-progress COVID effects, an extremely and decade-long easing monetary policy and now the Ukraine war, are strongly affecting KIRK’s customer base, composed of low-to-mid income clients. Lower customer demand and higher supply chain costs and constraints are impacting KIRK’s operational metrics and, to make things worse, this occurs in the midst of some sort of post-COVID hangover within the home furnishing space. All these aspects are of course really worrisome, but in the end are external factors outside the company’s control and presumably temporary. After all the operational changes carried out in the last years and taking into account KIRK’s rather-healthy balance sheet, the Company should be able to bridge over these troubled waters without relevant problems.

For me it is much more relevant the second aspect: KIRK is having serious problems trying to reach its customer base and finding its new niche market. As commented at the beginning of this article, one of the key KIRK’s strategic objectives was product revitalization, consisting basically on climbing the customer ladder (abandoning its low-price low-quality niche) and moving from seasonal stuff to a one-stop shop for complete home furnishing projects. In that sense, the Company implemented many initiatives in order to broad its product assortment and elevate design and quality. The problem is that the Company is not being capable of reversing its customer traffic trend.

Indeed KIRK, during the last quarters, seems to be entering into a dangerous no man's land where it is not being able to gain new customers and is losing ground within its historical customer base. Looking at the net sales evolution by quarters in the last years is rather telling:

It can be observed that there has not been a real improvement in terms of seasonality and clearly Q4 still remains the most relevant quarter for KIRK. Besides, apart from not being any relevant increase in the other quarters, Q4s have been progressively deteriorating.

The Company has relaunched its loyalty program and has increased its advertising expenses, but it is not yet being able to increase its customer base. This problematic situation might be probably exacerbated by the difficult moment for the sector, but there is no doubt that KIRK has a lot for work ahead.

During Q4 2021 call KIRK had to communicate its intention to slow down its strategy (and to extend the timeline to achieve its long-term financial targets):

“As we look back at the progress we have made, we realize we may have driven our merchandise transformation efforts faster than our ability to migrate customer base and make the necessary changes to our customer experience and infrastructure. While we have no intention of going backwards from here or wavering on our overall strategy, we do intend to alter the pace of change within our merchandise mix and style elevation. We believe this will allow our customer acquisition efforts time to catch up. The persistent macro environment constraints seem to be having a tangible effect on our consumer and we believe the impact is exaggerated since we are evolving our target customer, product sets, sourcing and customer experience in an already difficult environment.”

In Q1 2022 call they again reiterated their intention of slowing down the pace and directly suspended the expected timelines to achieve the long-term financial targets. Besides, during this last call they also communicated the many problems that they are still facing with labor, freight and transportation costs; their excess of inventory and their intention to return to a more promotional approach to liquidate it; the never-ending supply chain constraints; lower traffic and customer demand… All in all KIRK’s current situation is far from being a normal one.

Final thoughts

KIRK is a company that clearly is facing difficult times. The economic environment is directly affecting its customer base and making really difficult to keep costs under control. Besides, after three years driving the Company, the new management is not yet being able to succeed in bringing customers back.

At the same time it is fair to highlight the many improvements carried out during this period. The Company has aggressively reduced structural costs, optimized its store footprint and employees base, reorganized in a more efficient way its logistic structure and omni-channel platform… all these changes have made the company to be profitable again and to recover from a lackluster period.

However, financial metrics have been rapidly deteriorating in the last quarters and the short-term perspectives are worrisome. The macro environment is especially difficult for KIRK and there are some idiosyncratic issues that need to be fixed.

For the mid-to-long run the Company has ambitious financial goals: gross profit margin in the mid-to-high 30% range, EBITDA margin in the low-to-mid double-digit range and EBIT margin in the high-single-digit range. As commented, the timelines of these financial targets have been postponed sine die (initially the expectation was one-to-two years from Q2 2021) but the objectives remain unchanged. Indeed, those are targets reasonably achievable should the Company is able to revert the customer traffic situation. If finally the Company would be able to reach its financial targets, doing a back-of-the-envelope calculation and assuming no growth, we would be talking about an EBITDA over $60m and an EBIT over $40m, for a company with an enterprise value of approximately $95m.

In spite of the many positive points, nowadays the negative circumstances outweigh and have made me to decide staying on the sidelines and include this company as part of my watchlist. I do think that this is an interesting turnaround story with skilled and experienced management at the helm, and that, once they are capable of fixing its customer traffic problem and find their niche market, this could be a really successful play.