Should investors ever prefer dividends (vs buybacks)?

Should investors ever prefer dividends (vs buybacks)?

Reading Rappaport’s “Creating Shareholder Value” made me think about one issue that I have been wondering for a while: why so many (retail) investors look for companies that distribute dividends when generally those distributions diminish economic value for long term shareholders or happen in situations with little economic sense?

Let me first clarify that this is just from a theoretical capital-allocation perspective. I do understand that there are specific situations or purposes that could make dividend distribution desirable: keep ownership percentages unaltered; tax reasons (although share buybacks are generally more tax efficient); preference for a periodic stream of cash flows… Dividends distribution may be a useful tool in some situations, but usually those situations are beneficial for institutional and large investors. Not so much for retail investors.

The idea of this article is just to analyze the (un)convenience of dividends from a capital-allocation perspective. In other words, to try to answer the following question: should investors ever prefer dividends (vs buybacks)?

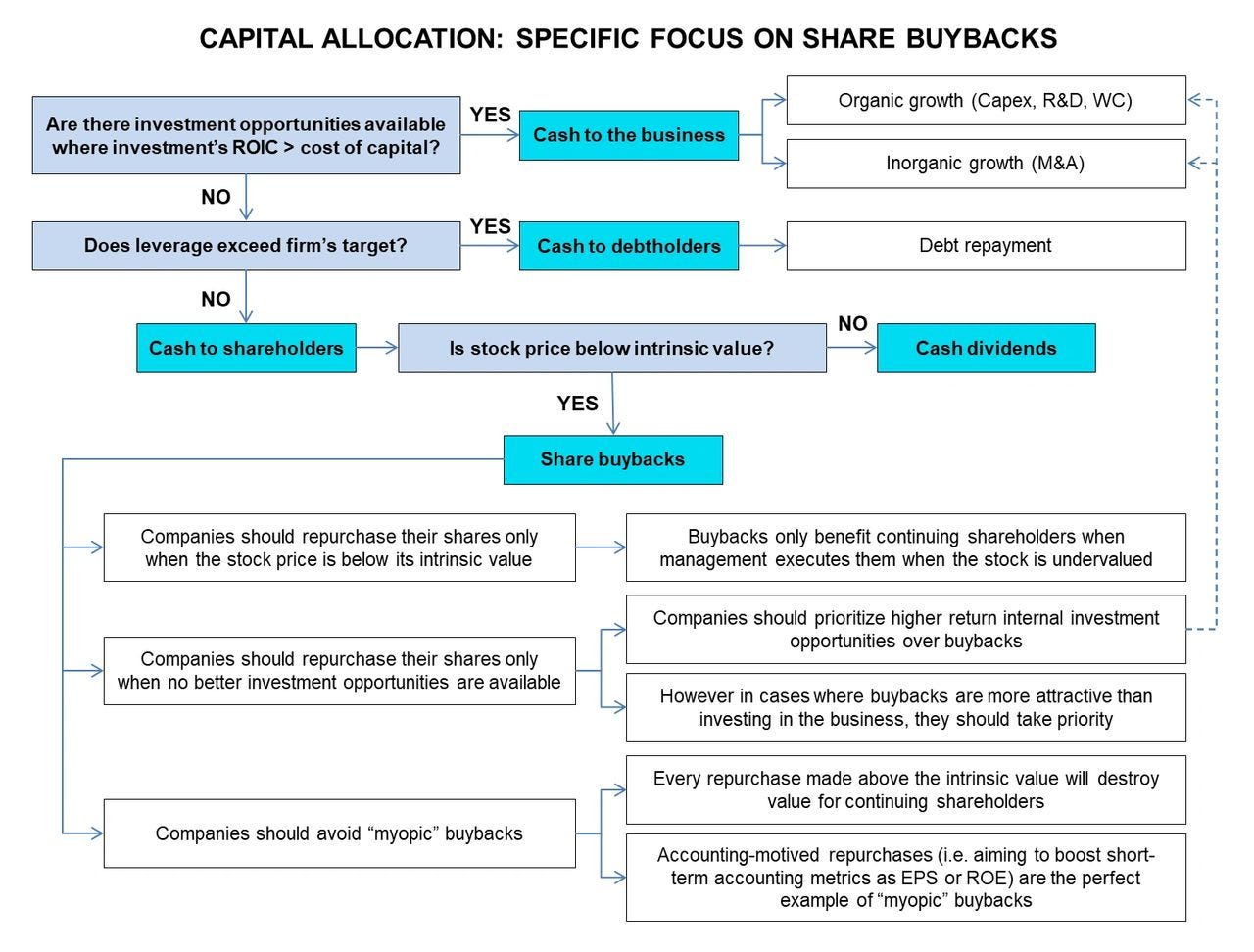

Let’s start with this capital-allocation flowchart:

As it can be observed, a company should, firstly, try to invest in the business (CapEx, Working Capital, M&A…) and, secondly, return cash to debt holders (until their target leverage ratio is reached). Afterwards, the company should decide the best way of giving the money back to its shareholders. This is exactly the starting point of this article: the moment when the company has to decide between dividends and share buybacks.

The right way to proceed is perfectly summarized by Mauboussin (2016): “When assessing a repurchase program, investors and executives should consider the golden rule of share buybacks, which states: A company should repurchase its shares only when its stock is trading below its expected value and when no better investment opportunities are available”. Additionally, also Mauboussin (2014) mentions that: “Only if a stock trades exactly at intrinsic value do buybacks and dividends treat all shareholders the same. If a stock is over- or undervalued, the effect of a buyback is different for selling shareholders than it is for those who continue to hold”.

In that context we can think about three potential situations: the stock is deemed to be overvalued, fairly valued, or undervalued. Let’s assume that when the stock is fairly valued the decision between dividends and buybacks is neutral (although this is only true under certain assumptions (see also Mauboussin, 2014) and so let’s focus on the other two situations.

Should the stock is deemed to be undervalued, from the investor’s perspective, the rational decision would be to prefer the company to buy back stocks. The reason is that “when a company's shares are undervalued by the market, a share repurchase transfers wealth from exiting shareholders to continuing shareholders” (Rappaport, 1998). This is perfectly explained in the following chart (Mauboussin, 2014):

“Whether the company buys under- or overvalued stock or pays a dividend doesn’t make a difference in terms of the value of the disbursement or the subsequent value of the firm. What differs is who wins and who loses as the result of buying stock below or above intrinsic value” (Mauboussin, 2014).

“Buying back overvalued stock benefited sellers at the expense of buyers” (Mauboussin, 2014).

So in this situation clearly buying back stocks should be the preferred option from the investor’s perspective, instead of dividends distribution.

In the opposite direction, should the stock is overvalued, the rational decision would be to prefer the company to distribute dividends. In case the company opts for buying back stocks in this situation, it would be transferring wealth to the exiting shareholders (at the expense of the continuing ones). In that sense, this might be a situation where dividends would be the right option. However, does make any sense, from the investor’s perspective, to hold stocks that are considered overvalued? I guess not. So in this case the rational decision would be to sell the stocks and then it would be irrelevant the dividend vs share buybacks decision. Mauboussin (2014) also mentions this issue in its paper: “Finally, it is logical that you would prefer that the companies you hold in your portfolio buy back stock rather than pay a dividend. It should be reasonable to presume that you own shares of companies that you think are undervalued. If that is the case, buybacks will by definition increase value per share. The only instance where this may not be true is if you believe that a dividend would provide a more powerful signal to the market, hence creating more value than a buyback”.

The conclusion is that, just from the capital-allocation perspective, there are no situations where dividends are distributed and at the same time these are optimal situations for investors.

References:

Rappaport, A. (1998).Creating Shareholder Value. A Guide for Managers and Investors.

Rappaport, A. & Mauboussin, M.J. (2001). Expectations investing. Reading stock prices for better returns.

Mauboussin, M. J. & Callahan, D. (2014). Disbursing Cash to Shareholders. Frequently Asked Questions about Buybacks and Dividends.

Mauboussin, M. J., Callahan, D. & Majd, D. (2016). Capital Allocation. Evidence, Analytical Methods, and Assessment Guidance.