Citi Trends ($CTRN): A Cinderella among its Peers

Citi Trends ($CTRN): A Cinderella among its Peers

In a nutshell

After a period of underperformance and with the help of an activist investor, Citi Trends (CTRN or the Company) has been able to turn around its struggling situation.

Since 2019 it has been improving its operating metrics and efficiency, renewed its management, reaccelerated its growth, improved its capital allocation and looks at the future with ambition and from a strong financial position.

New management is amazingly delivering and constantly beating Market’s expectations.

However, the Market is yet cautious with the Company and rejects to value CTRN like its peers.

Should new management keeps executing it is just a matter of time to see a re-rating of the Company. This, together with CTRN’s strong financial position, turns the Company into a great investment opportunity with little downside risk and a lot of upside.

Why the opportunity exists?

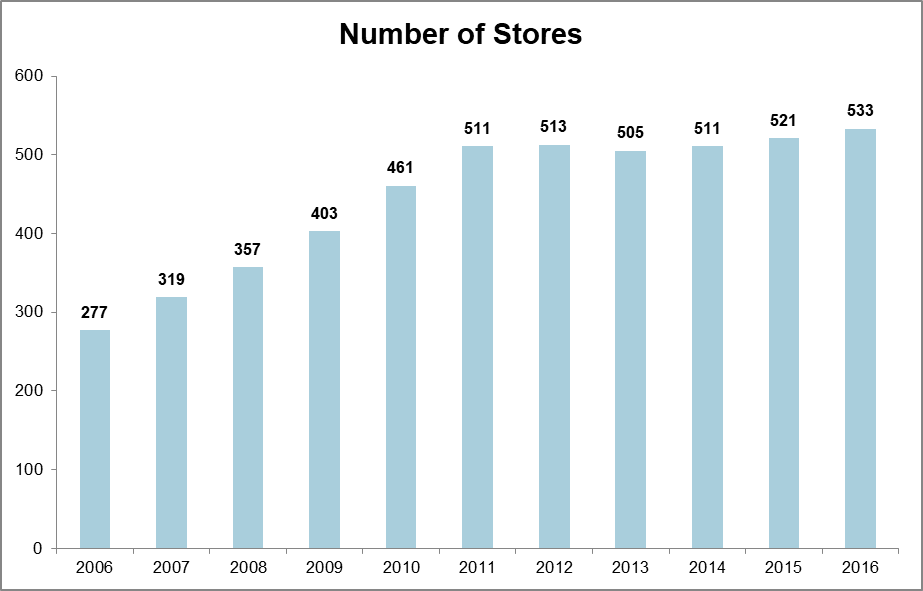

Citi Trends is a “specialty value retailer of apparel, accessories and home trends primarily for African American and Latinx families” (2020 Form 10-K). The Company enjoyed an intense growth period since its IPO in 2005 till 2011, with an average of 40/50 net openings per year but, after that, entered in a period of stagnation coupled with deteriorating metrics:

(Image Source: Author’s chart, Macellum Capital Management documentation)

In 2017, Macellum Capital Management, an activist investment firm, started a campaign as they thought that “with proper guidance and oversight (they) believe there (was) a significant opportunity to create value for all CTRN stockholders” and that “the Company could recover lost sales productivity and margins while generating material cash flow from inventory optimization”. I would suggest anyone interested in CTRN’s struggling situation at that time to read all the documentation related to the activist campaign. Here is the link.

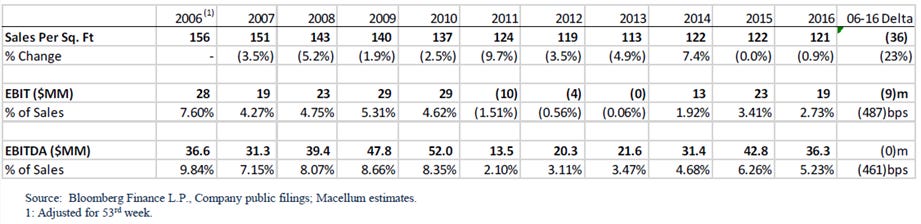

In summary, CTRN was a company with declining operating metrics, poor capital allocation, management misaligned and overpaid, and significant underperformance versus peers.

This situation made CTRN to be valued lower than its peers and its stock to underperform, and the Company has been fighting to change Market’s mind since then.

(Image Source: Macellum Capital Management documentation)

What has changed?

In 2019 CTRN and Macellum Capital Management reached an agreement and the Company started to improve.

First of all CTRN initiated an intense renovation of its executive officers, incorporating new blood to key management positions:

Lisa A. Powell as Chief Merchandising Officer (from TJX) in September 2019.

Charles J. Hynes as Senior VP of Supply Chain (from Burlington) in October 2019.

David Makuen as CEO (from Five Below) in March 2020.

Pamela J. Edwards as CFO (from L Brands/Victory Secret’s) in January 2021.

Almost the complete composition of the Board of Directors (7 out of 9 members) has been renovated/incorporated since Macellum’s intervention.

Additionally, the Company clearly stablished its key strategic priorities and, more importantly, started to execute:

Grow the fleet

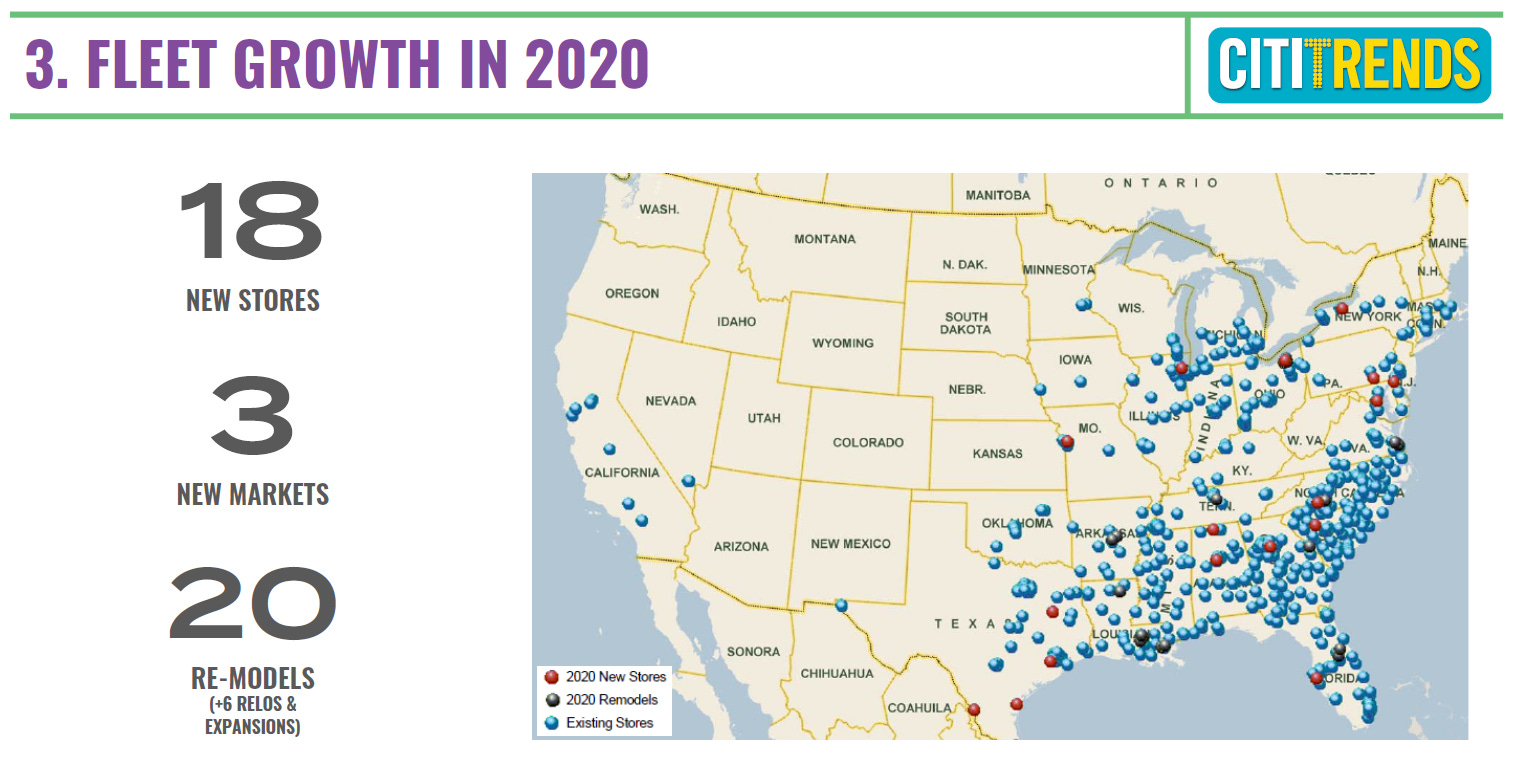

Since the very beginning the new management made clear that there was a “vast runway for growth” and that the Company had at least 1000 store fleet potential. CTRN is currently present in 33 States with 603 stores and so they have much room to densify current markets as well as to enter new ones.

(Image Source: CTRN’s April 2021 Presentation)

The new management also reasserted their intention of accelerating annual store openings with the objective of 30 new stores per year.

(Image Source: Author’s chart, Forms 10-K, Q3 2021 conf call)

As it can be observed the Company tried to speed up the opening pace during the last 2 years but, despite the acceleration, CTRN has not been able to achieve its target. However it is important to take into account that 2020 and 2021 has been “COVID years”. Indeed it is rather impressive that even in 2020 the Company (a brick-and-mortar company!) was able to open 18 new stores, and in 2021 it will probably be able to almost reach its 30-new-stores target ending the year with 611 stores. Additionally, in the last conference call (Q3 2021) they mentioned that they “plan to open approximately 40 new stores in fiscal 2022”.

Optimize product mix

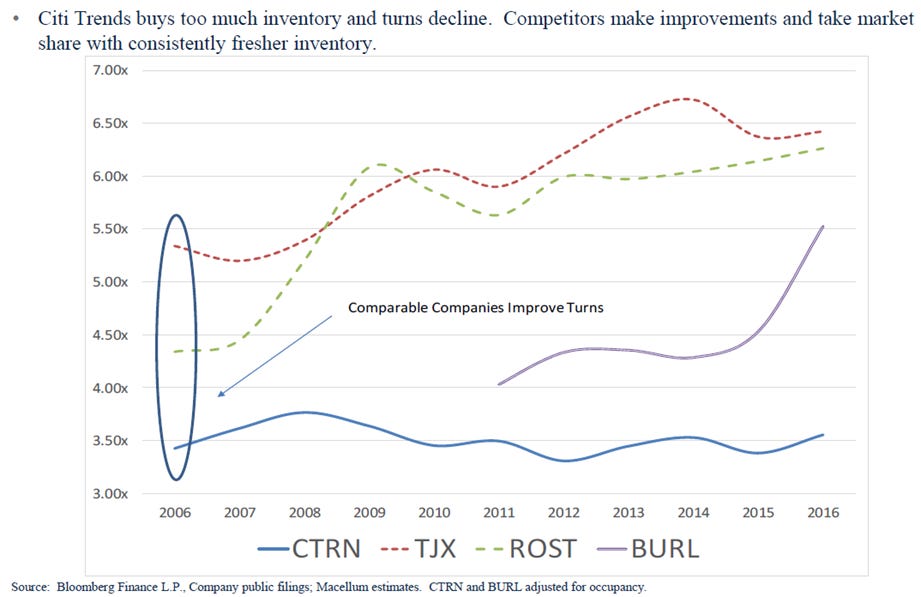

CTRN has historically suffered a slow inventory turn compared with its peers:

(Image Source: Macellum Capital Management documentation)

However, since mid 2019 the Company started to seriously work on inventory optimization through different initiatives: reinforcing its buying team; making strategic efforts to optimize inventory levels and lower weeks of supply; taking advantage of off-price buying opportunities and expanding its vendor base; applying data and analytics to inventory planning; rationalizing inventory to achieve a cleaner inventory position… All these measures are starting to bear fruits and inventory turns are improving:

(Image Source: Author’s chart, Forms 10-K & 10-Q)

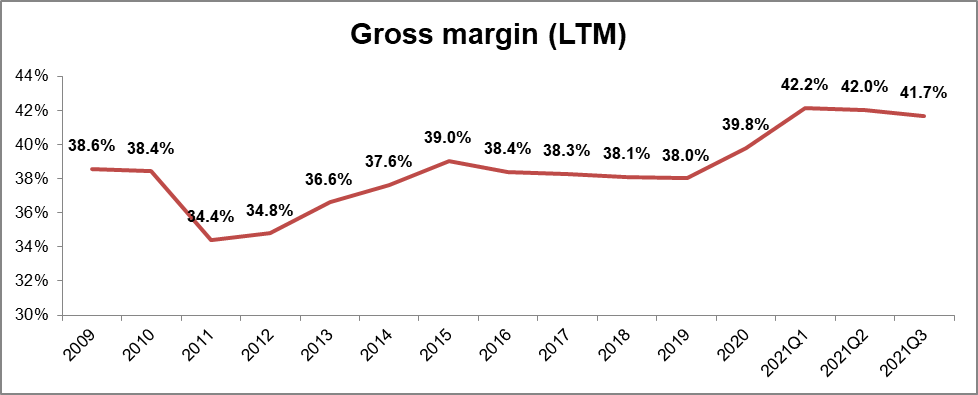

Additionally all these efforts are also having a positive impact on CTRN’s gross margins as better buying and inventory management processes ultimately mean lower markdowns and higher margins:

(Image Source: Author’s chart, Forms 10-K & 10-Q)

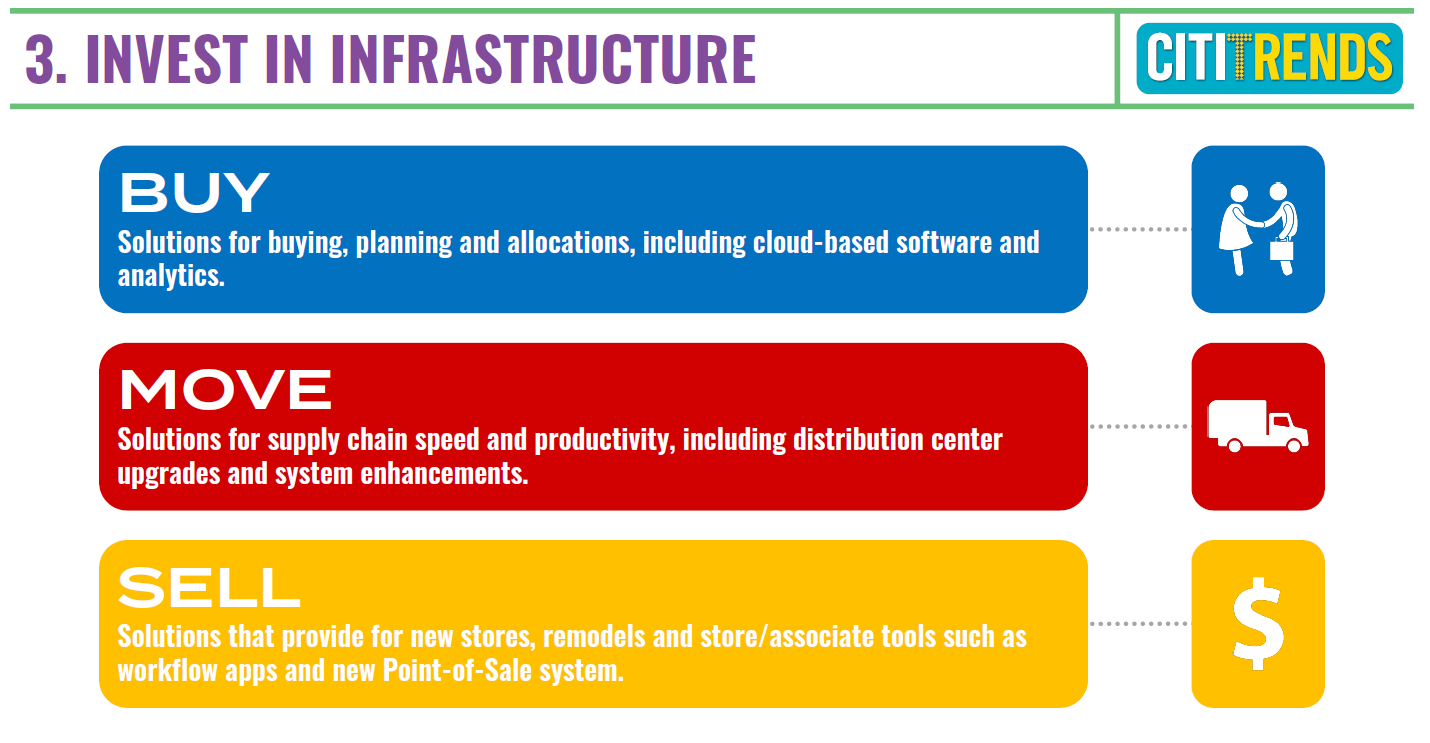

Reinvest in infrastructure

CTRN is committed to invest in their infrastructure and systems across what they call “the three pillars”:

(Image Source: CTRN’s January 2021 ICR Presentation)

“Buy” pillar’s objective is to keep pushing the use of data and analytic tools for buying, inventory planning and allocation process.

“Move” pillar’s idea is to reduce bottlenecks and the impact of labor and freight costs.

“Sell” pillar comprises real estate and stores divisions and, right now, beside stores openings, its key project is CTRN Experience (CTX). CTX is the new store format that was presented by the Company in Q1 2021 (and more broadly explained in Q2 2021 earnings call) and that, after some testing and promising results, the Company has decided to rollout to all new stores and remodels (Q3 2021 earnings call)

This is maybe (together with the next point 4) one of the objectives that is less observable in the short term but that will be for sure accretive to the performance and profitability of the company in the future.

Make a difference in their communities

CTRN is committed to make an impact in the communities they serve and has the objective to promote social initiatives in order to enhance the relationship with its customers. In that sense it has created the Corporate Social Responsibility Committee and the CitiCARES Council to promote and oversee initiatives around ESG and social responsibility; and it has launched the Black History Makers Program to help Black entrepreneurs.

The idea is to integrate CTRN within the local environment helping the customers not only in their purchase decisions but also make store managers and team members be part of their customers’ lives and communities.

What else?

I have already mentioned many aspects that give an idea of how CTRN has changed during the last years. Currently CTRN is a growing company with a “vast runway for growth” and store openings acceleration; improving its operational metrics; modernizing its infrastructure; investing in new management… However, there are even more aspects that can make CTRN to be considered indeed a quality company or at least a much better company that it was in the past:

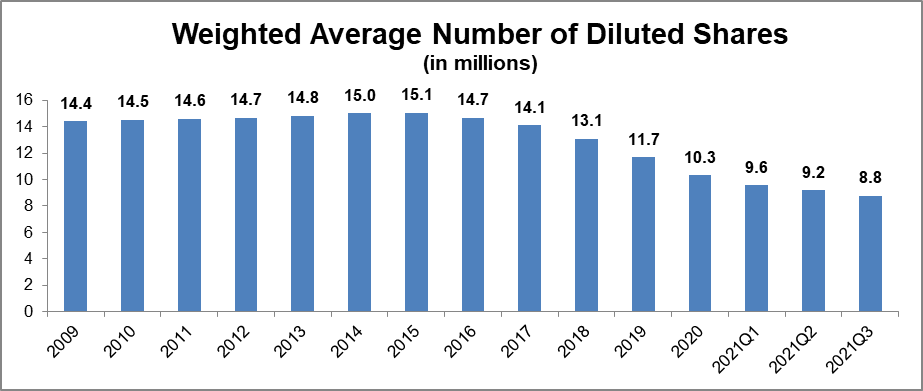

CTRN has improved its capital allocation.

CTRN promotes a shareholders-friendly capital allocation: operating cash flows are firstly allocated to the business (growth and maintenance capex) and the rest is mainly devoted to share repurchases. Since 2015 the Company has almost halved its shares number:

(Image Source: Author’s chart, Forms 10-K & 10-Q)

CTRN temporarily suspended repurchases in March 2020 but the stock repurchase program was reinstated in September 2020. Since then the program has been especially intense with the reduction of CTRN’s shares count by more than 1.5 million shares during the last year. Besides its management seems to be committed with the idea of keep repurchasing its undervalued stock and seamlessly approves new repurchase programs quarter by quarter.

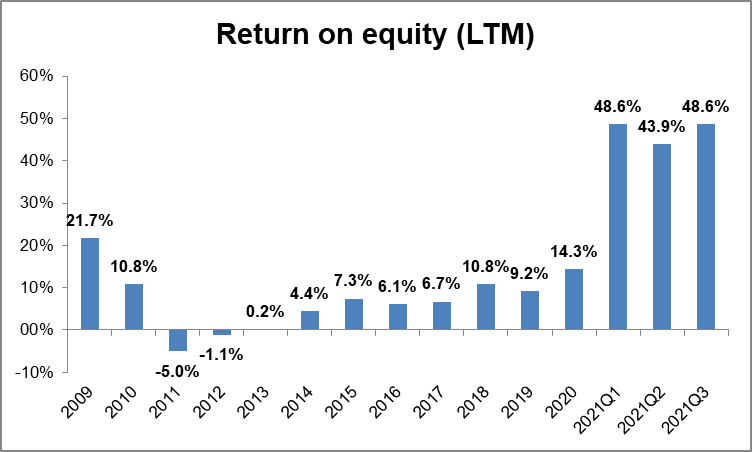

This aggressive shares count reduction (together with margins and profitability improvements) has made return ratios to explode:

(Image Source: Author’s chart, Forms 10-K & 10-Q)

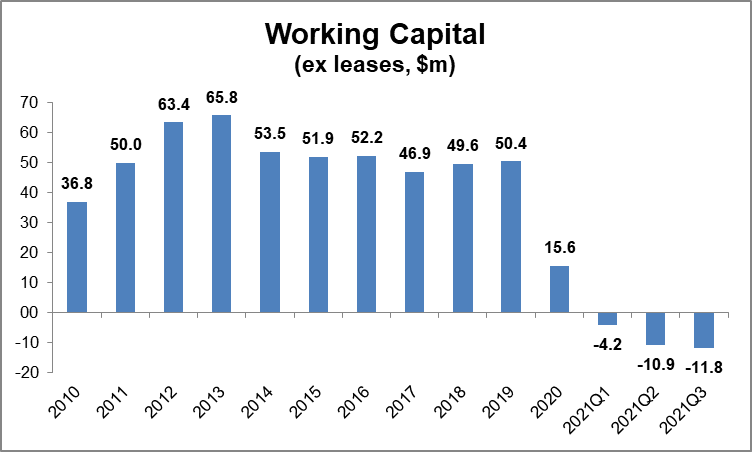

CTRN presents a strong financial position, with net cash and zero debt.

The principal source of CTRN’s liquidity is the cash flows generated from operations and has no outstanding debt and more than $47 million in cash by the end of Q3 2021. Additionally, thanks to the improvement of its inventory management and to its shortened cash conversion cycle, the Company is right now in this enviable situation where it can use the money of its vendors to fund its inventory (i.e. negative working capital):

(Image Source: Author’s chart, Forms 10-K & 10-Q)

All in all CTRN has become a company with much room for growth, minimal capital needs and high-return reinvestment opportunities.

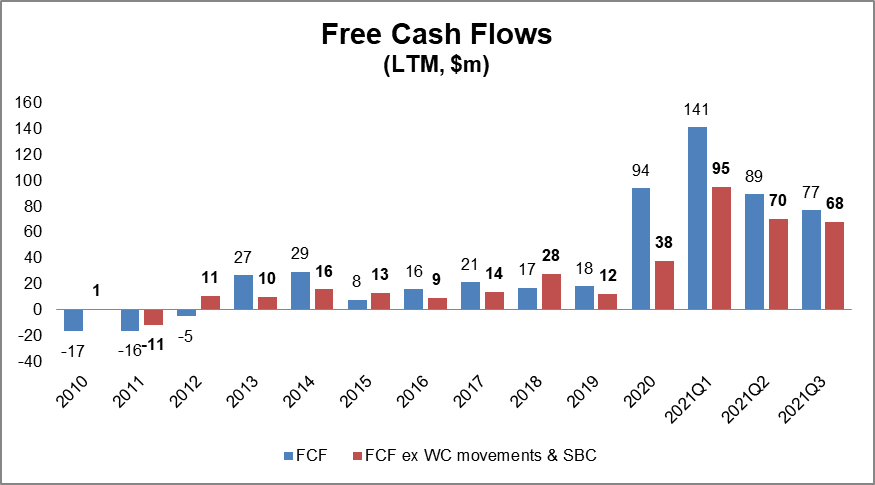

CTRN generates strong and increasing FCF.

CTRN has historically generated positive FCF, even during its stagnation period:

(Image Source: Author’s chart, Forms 10-K & 10-Q)

This chart depicts the evolution of FCF and FCF before Working Capital changes and Stock Based Compensation. This second measure is a smoother cash flow metric that eliminates jumps in current assets/liabilities and that tend to offset each other quarter by quarter, being more stable in the long run.

In any case, whatever the FCF metric, it is clear that CTRN has been able to steadily generate FCF and has been clearly improving its cash generation during the last year. It is true that it is still early to see what will be the impact of eliminating the disruptions caused by the COVID pandemic and all the stimuli provided during this period, but CTRN’s growth trajectory invites to be optimistic.

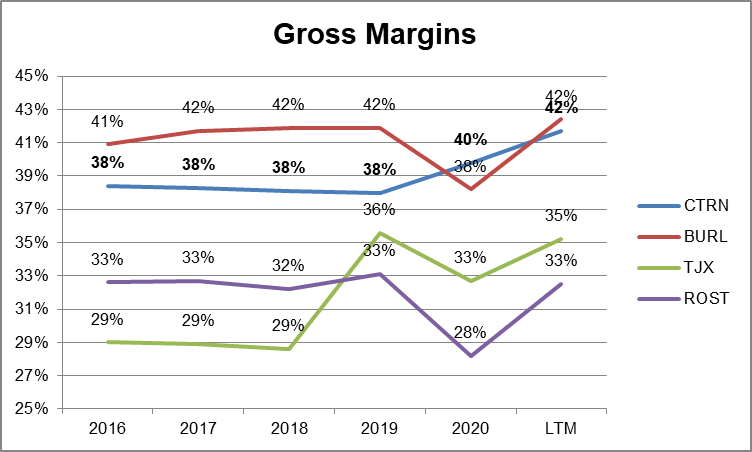

CTRN is improving all its margins (and not only Gross margins).

Besides Gross margin improvement, and despite the many actual costs headwinds, CTRN has been capable of translating this improvement to the bottom line. The company has been working on many efficiency initiatives of their internal operations and processes (see previous point 3. Reinvest in infrastructure) and this is gradually being reflected in its EBITDA and EBIT margins:

(Image Source: Author’s chart, Forms 10-K & 10-Q)

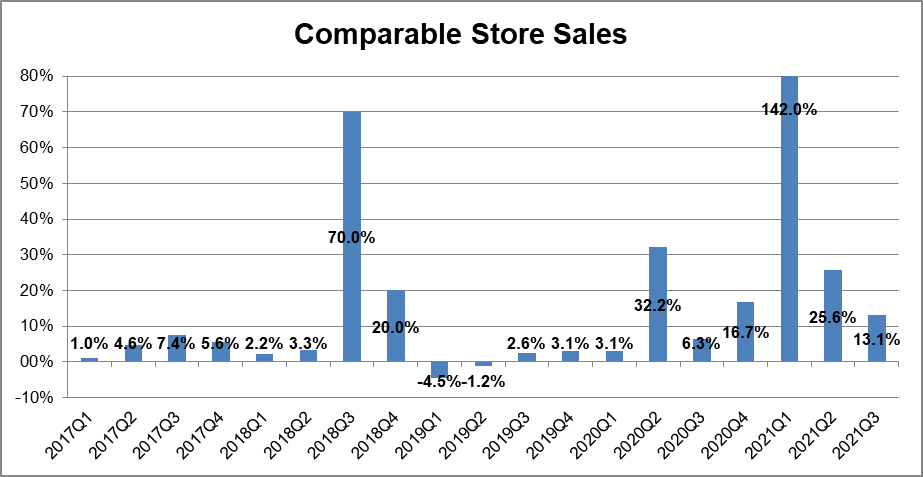

CTRN is increasing its Comparable Store Sales quarter by quarter.

This Q3 2021 has been the 9th consecutive quarter of positive open-only Comparable Store Sales for CTRN.

(Image Source: Author’s chart, Forms 10-K & 10-Q, CTRN’s April 2021 Presentation)

CTRN is expanding its customer base, and not only growing its fleet.

CTRN has historically been focused on African-American markets but in 2019 they started their first testing stores in markets that were predominantly Hispanic. CTRN has realized about the Hispanic community potential and now is making a relevant effort on this front.

(Image Source: CTRN’s April 2021 Presentation)

This could be a game changer as the Hispanic community represents even a bigger opportunity than the African-American market, as they account for the 18.7% of the US population (by 2020 Census) versus 12.4% of African Americans.

CTRN has been steadily expanding its merchandise mix.

CTRN made the strategic decision of accelerating non-apparel penetration (i.e. home and accessories) and has morphed its merchandise composition from an 80% apparel/20% non-apparel company 10 years ago to a 60%/40% today. Their intention is to keep pushing in this direction to reach something similar to a 50%/50% situation, with the idea of creating a more diversified company and become closer to a one-stop shop.

What about its peers?

CTRN operates within the retail sector where we could choose many companies to compare with, but there are 3 companies that can be considered its main peers:

Burlington Stores, Inc. ($BURL)

TJX Companies, Inc. ($TJX)

Ross Stores, Inc. ($ROST)

Let’s have a look at some of the main indicators related to these companies:

(Images Source: Author’s chart, TIKR.com)

CTRN has been historically below its peers’ performance in many operational metrics but, as commented in the previous section, it has been improving all its margins and finally has been able to achieve its peers’ profitability levels.

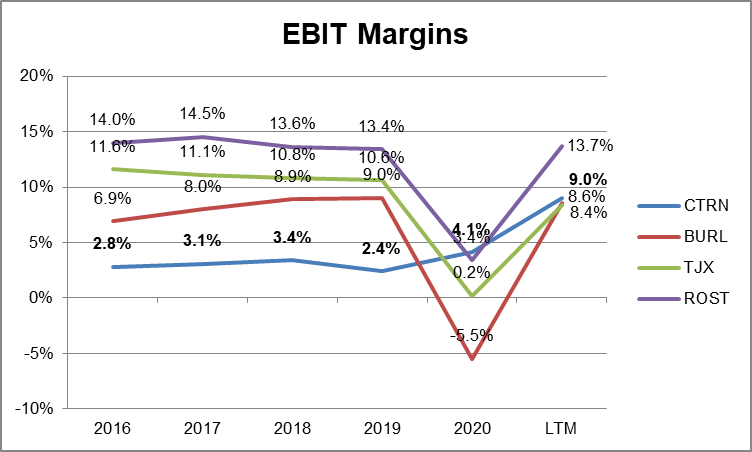

A similar picture can be observed if we look at return ratios. For instance, this is the situation with regard to Return on Capital:

(Image Source: Author’s chart, TIKR.com)

CTRN has been lagging during the last years, but has finally achieved the best Return on capital among its peers group.

And again, if we analyze inventory turns we can observe how CTRN has been able to turn its inventory management around and position itself at the same level as its peers:

(Image Source: Author’s chart, TIKR.com)

But what about valuation? As CTRN is approaching its peers’ levels in terms of operational metrics and profitability levels, it could be expected the Market to assign a similar valuation to theirs. In that sense, let´s now look at the different valuation multiples for all these companies:

(Image Source: Author’s chart, Seeking Alpha)

As it is pretty clear, whatever the multiple, the market is still reluctant to assign CTRN the same valuation as to its peers. It seems that there are still doubts about the Company being able to keep this positive trajectory. However, the reality is that CTRN has been clearly over-delivering and beating market expectations since 2019, and specifically during this pandemic period. Should CTRN keeps executing it is just a matter of time to see a rerating of the Company and a rerating to just the level of its lower-valued peer ($ROST) would imply a huge upside. All in all this is a company with little downside risk due to its strong financial position and a lot of upside.

Getting a re-rating is hard to do in normal times let alone now. What's your confidence that it could get a re-rating to peers?

Had a question for you regarding the 2022 icr slides presented on 1/10/22. The net investment for new stores on slide 25, doesn’t jive with the new store capex allocation for 2022. I assumed the net investment per store is a combination of capex and net working capital. If I then look at the capex allocated for new stores from slide 28 and assuming 45 new stores, I get a per store number higher than the net investment of 380k. What am I missing?