Airbnb ($ABNB): Wonderful Business But Still Expensive

Airbnb ($ABNB): Wonderful Business But Still Expensive

Introduction

I do know that this is not the best way to start an article but I have to admit that I’m really disappointed. Not with the article itself but with its conclusion: Airbnb (ABNB) is a wonderful business but still expensive.

For those who love quality companies, I think it is rather common to have ABNB always on the radar. Knowing nothing about the company, anyone has the feeling that this is probably a really great business that will have a bright future. However, it is also the kind of company that seems to trade always at “expensive” multiples.

That was my feeling just before starting this article. However one of the main lessons that I have learned during my investment career is that frequently investors make the mistake of rejecting investment opportunities because they are “optically” expensive. This is a rather common error for value investors and it is important to fight against our own prejudices because we may lose many interesting opportunities.

Once I was able to overcome these initial prejudices, I started to read about the company and I fell completely captivated. ABNB is a fascinating company lead by an amazing management team and with features that make the Company one of a kind. Indeed the more I read, the more I realize that the secret sauce of Airbnb is not its business model (at least not only) but two characteristics that make the company rather unique: its resilience and its creative and entrepreneurial culture. I do know that those concepts tend to be overused and even could be considered empty buzzwords, but in the case of ABNB they unfold all their sense and one realizes how these concepts may become real competitive advantages. So the first feeling was correct: we are in front of a huge-quality business.

Unfortunately, the other initial feeling, the expensiveness feeling, seems to be also right in this specific case. The foreseeable return, after the pandemic period, of some key metrics to more normalized levels could have a relevant impact on ABNB’s numbers and so in its valuation. Besides, the pandemic has introduced some distortions in the travel industry that make rather complicated to make a meaningful valuation and so it is advisable to compensate this uncertainty with a higher margin of safety. These two factors, the potential reversion to more normalized levels and the need of a higher margin of safety, make me stay on the sidelines and keep this company in the watchlist at the current levels.

Being said that, I think ABNB is a really interesting case study and I will try to convey throughout this article why I believe this, and why I think this Company will continue thriving in the future and deserves a prominent place in the watchlist. However, at the end of the article I will try also to explain the reasons to think that its current trading levels are too high.

Resilience (or the Art of Surviving)

The history of ABNB is well known: two friends (Joe Gebbia and Brian Chesky) decided in 2007 to rent three air mattresses in their apartment in order to help with their own rent payment. The experience was so successful (for them and for their guests) that they decided to start a business (together with a computer scientist, Nathan Blecharczyk) and since then the Company has been steadily growing until becoming the behemoth that it is today.

However, the most interesting part is not the success of this history in and of itself, but how this success has been achieved. The history of ABNB has been forged on existential moments. It is one of those companies that seem to have lived on a knife-edge on many occasions and it hasn’t been uncommon to find each and every year articles predicting its end.

However, this bumpy road has made the Company to reinforce its resilience as it has been able to overcome each and every hurdle to become the successful organization that it is today. This is what really captivated me about this Company: its adaptability and its capacity to overcome critical moments with creativity. There is a really telling anecdote that perfectly describes the spirit of this Company. In 2008, months before some venture capitalists insufflated initial investments in the Company, ABNB was struggling to keep the company afloat and in order to raise capital they decided to sell cereal boxes with candidates’ faces (Obama O's and Cap'n McCains) during the 2008 Presidential Election campaign:

This gives an idea about the nature of this Company and its founders: people ready and capable of overcoming any critical moment with creativity.

Since then the Company has faced many make-or-break moments but it has been able to reemerge stronger each and every time. This innovation culture and resilience are two characteristics that perfectly define this company and that have completely taken my attention. Let’s review some of those defining moments in order to have a better idea about the idiosyncrasy of this company:

In 2011 the home of a San Francisco host was vandalized and this issue got a lot of press coverage. One of the most relevant hurdles for Airbnb at that moment (and still today) was to convince hosts about the security of listing their homes within the platform. That incident for a still-incipient company was a really critical one. However the company rapidly assumed its responsibility and implemented a “$50,000 Airbnb Guarantee, protecting the property of hosts from damage by Airbnb guests”. The problem was solved and since then hosts and guests protection in one of ABNB’s mantras.

Almost since ABNB started its expansion, it has been battling with many local authorities. As a matter of example, it is rather telling the fight against New York authorities almost since the company started to operate in that city but specifically since 2014, when the General Attorney of the State (Eric T. Schneiderman) published a report stating that “found widespread illegality across New York City listings on the Airbnb website”. ABNB has faced regulatory issues from the start, especially in dense populations with housing affordability problems but (at least until now) has been able to reach agreements with many local authorities in order to find compromise solutions.

Copycats, clones and lookalikes have been another constant nightmare for ABNB. Probably one of the most famous is the case of Wimdu, a German startup backed by Rocket Internet. The company started in 2011 and rapidly “was on track to conquer Europe in the vacation rentals space”, at a time when ABNB didn’t have a strong foothold in the continent. However ABNB rapidly realized that it was critical to move as fast as possible. ABNB opened offices in Europe, acquired some smaller players and made huge advertising campaigns, all at the beginning of 2012. As one of its former executives said: “When competition comes after you, move ridiculously fast. Marketplaces are normally winner-take-all markets. If we had lost ground to European competitors in 2012, we may have never gotten it back”. And this is what ABNB did. Wimdu finally closed its doors in 2018.

COVID-19 has been another critical moment (“when borders closed and travel stopped, our business declined by nearly 80%”). However, as we will see, the Company was able to make rapid and difficult decisions in order to underpin the business, reorganize its priorities and make the organization much more efficient, and as a result has emerged stronger than ever.

In summary, ABNB is a company that has been facing many “defining moments” along its history and has been able to overcome each and every one. This has made the company much more resilient and stronger, but also has served to expand this way of thinking and working across the organization, making resilience a structural feature.

Creativity and Entrepreneurial Culture (or the Art of Innovating)

Another defining feature of ABNB is the innovative and entrepreneurial culture that spreads throughout the organization. Since the very beginning the founders focused on hiring people with entrepreneurial skills, people who could create. The idea was to set up a collaborative environment for people to be ready to solve complex problems and find creative solutions.

ABNB fosters the utilization of iterative processes where new ideas are steadily purposed and refined. Indeed it is really interesting to see how, as a result of those processes, ABNB is able to both constantly innovate and launch new products, and at the same time to rapidly discard those that don’t perform as expected or reprioritize when circumstances change. This culture keeps ABNB constantly adapting and improving its services, making its customers to come back to its platform.

A perfect example of this way of working is how ABNB faced the pandemic period. Just before the pandemic started, ABNB was trying to boost services like Airbnb Experiences, transportation services and business travels. However the COVID-19 supposed the complete standstill of the travel industry and the need for ABNB to review all its plans. The company rapidly reorganized its priorities focusing on its core activities, launching new products that could better fit with the new reality (e.g. pivoting in-person Airbnb Experiences to Online Experiences) and making the organization much leaner.

This capacity to innovate and constantly adapt to new circumstances is a really powerful skill for an organization and one really difficult to achieve.

Business Model: Airbnb as a Marketplace

For me those characteristics commented in the previous paragraphs may be enough to make me love ABNB, but fortunately it is also a great business model. Let’s dive into it a bit.

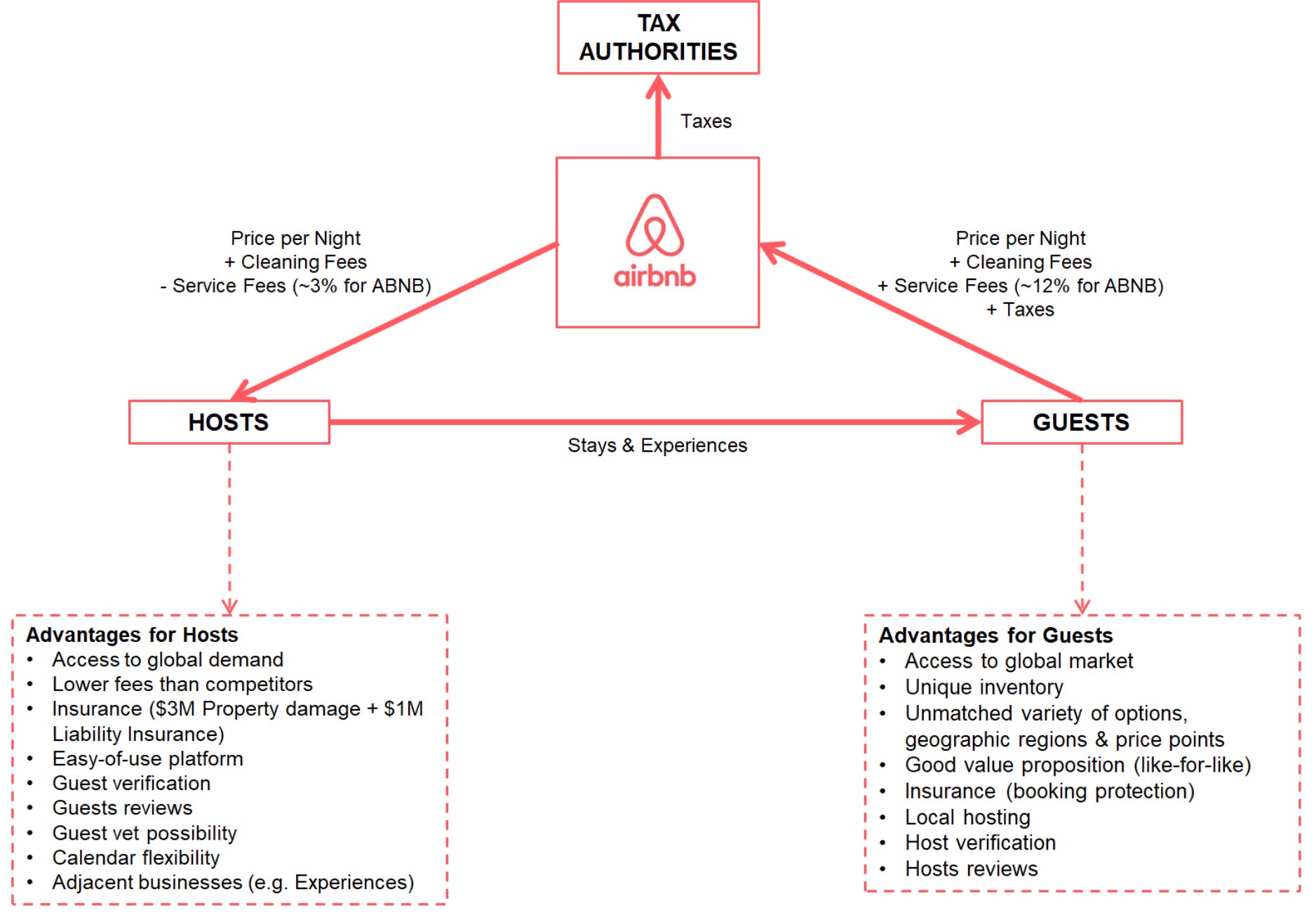

This Company is a two-sided marketplace where guests can book accommodations or experiences and hosts can list properties available for rental and offer activities, earning ABNB a commission for each of the bookings made:

This is a powerful business for all the stakeholders. Guests and hosts have instant access to a global network across more than 220 countries, through an easy-to-use platform and protected by many features that make the experience safe and convenient. Besides, ABNB provides tax authorities in many jurisdictions with agreements to collect taxes on behalf of hosts, making much easier for those hosts and authorities tax collection and remittance.

From ABNB’s perspective, this is also a business with many inherent benefits (e.g. asset light model, scalability, no properties owned, etc.) but probably the most relevant one is its capacity to generate network effects. Most profitable marketplaces are those able to create a flywheel in which higher demand brings higher supply, and higher supply in turn fosters demand. Reaching these dynamics is rather difficult at the beginning because there is a lack of both supply and demand, and so neither the hosts nor the guests, in the case of ABNB, have any incentive to jump into the marketplace. ABNB was absolutely aware of this issue from the beginning and was working location by location till achieving the number of listings needed to make the growth take off. Once a minimum listings threshold was reached, the flywheel started to spin and the marketplace to grow almost by itself.

And I say “almost” on purpose because, although flywheels spin by themselves, it is really important to work constantly in those features that keep the mechanism perfectly oiled, and here resides one of the main characteristics of this company. ABNB has been steadily working on both sides of the marketplace in order to improve the user experience and has been able to identify the key friction points that could constrain supply and demand, removing or at least reducing them as much as possible over time.

In the case of the supply side the most relevant issues are trust and convenience. Many potential hosts have to overcome the fear of inviting strangers to stay in their own homes and of suffering any damage on their properties. ABNB rapidly realized about this issue and has been constantly working to improve trustworthiness through the implementation of different innovations: an insurance policy (unmatched by any other industry player), verified identification, secure payment structure and 24/7 customer service. Additionally ABNB knew that the process to become a host needed to be as smooth as possible, as in the end convenience means higher conversion. In that sense the Company continually seeks to improve the hosting process, trying to reduce as much as possible the steps and time required to list properties within the platform.

With regard to the demand side, the most relevant points are uniqueness and value. Travelers come to Airbnb because the platform offers “the largest and most diverse range of unique accommodation options” and provides greater value than hotels. In that sense, ABNB has been also working tirelessly to improve the browsing and booking experiences, constantly refining the way guests interact with the platform and making them easier to be aware of those uniqueness and value features. In the end it is again all about convenience and ABNB has absolutely internalized the idea that the experience should be several orders of magnitude better than the alternative in order to keep customers coming back.

In summary, ABNB is a powerful marketplace with an organization at the back that keeps this marketplace well-oiled and that creates the dynamics that help supply and demand to steadily grow.

Finally it is important to mention some interesting features that the Company has recently launched and that I think could have a relevant impact in the future. I am talking about functionalities like Airbnb Categories, I’m flexible or the possibility of booking split stays. These new features intend to move the company to the top of the funnel by not only supporting travelers finding accommodation in specific locations, but also helping them to decide where and when to go. In other words, create a more inspirational experience. But let me provide some context in order to explain why I consider this could suppose a game changer.

As commented above, until now the company was reinforcing separately the two sides of the marketplace, fostering demand and supply as separate vectors. The problem with a marketplace like ABNB is that sometimes increases in both supply and demand don’t necessarily mean higher bookings. The reason is that, for the bookings to increase, the platform needs higher supply and demand, but also needs them to match. In other words, demand needs to be directed where the supply is and this is exactly the raison d'être of these new features. These recent additions reflect ABNB’s new way of thinking and the adoption of a more proactive approach that will probably generate multiple benefits for all the stakeholders: hosts outside most touristic places will get higher visibility for their listings; guests will get inspired and discover new places; and even communities will benefit for more evenly distributed tourism outside crowded places and for lower seasonality. Once all these new functionalities are working on all cylinders, the impact may be really relevant.

Additional Positive Points

Apart from the powerful business model presented in the previous paragraph, ABNB presents some other additional characteristics that make the Company a really attractive business and invites to think that there are many possibilities for them to keep thriving in the future. Let’s have a look to some of them:

Global leadership

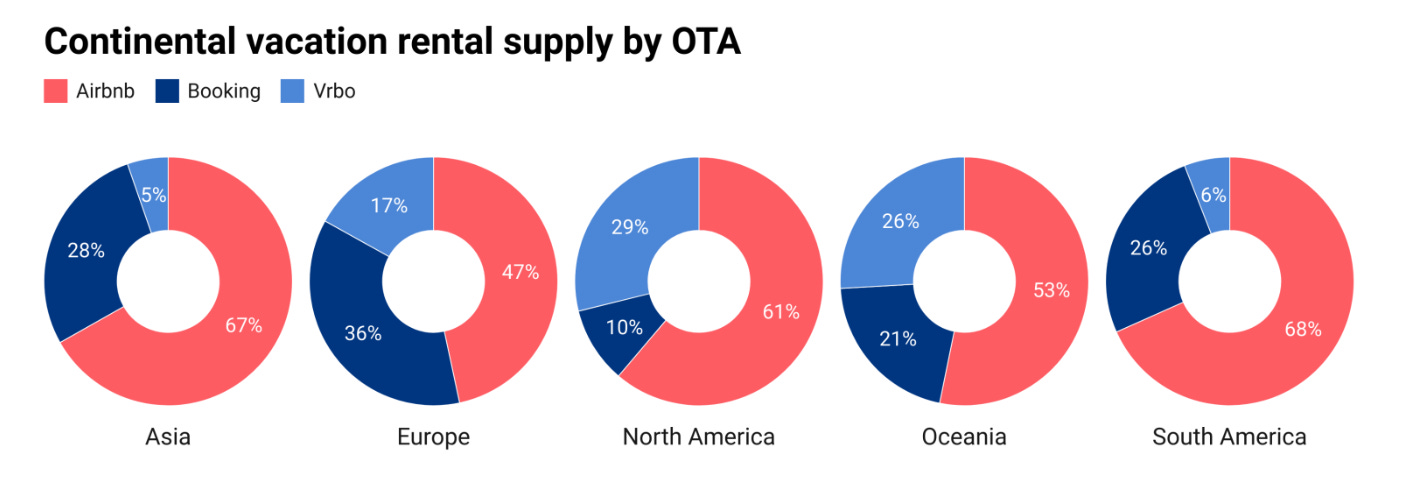

ABNB is the clear leader in the short-term vacation rental market, with a “strong quota in every world region”:

As it can be observed it dominates each and every region, being particularly strong in North and South America and Asia.

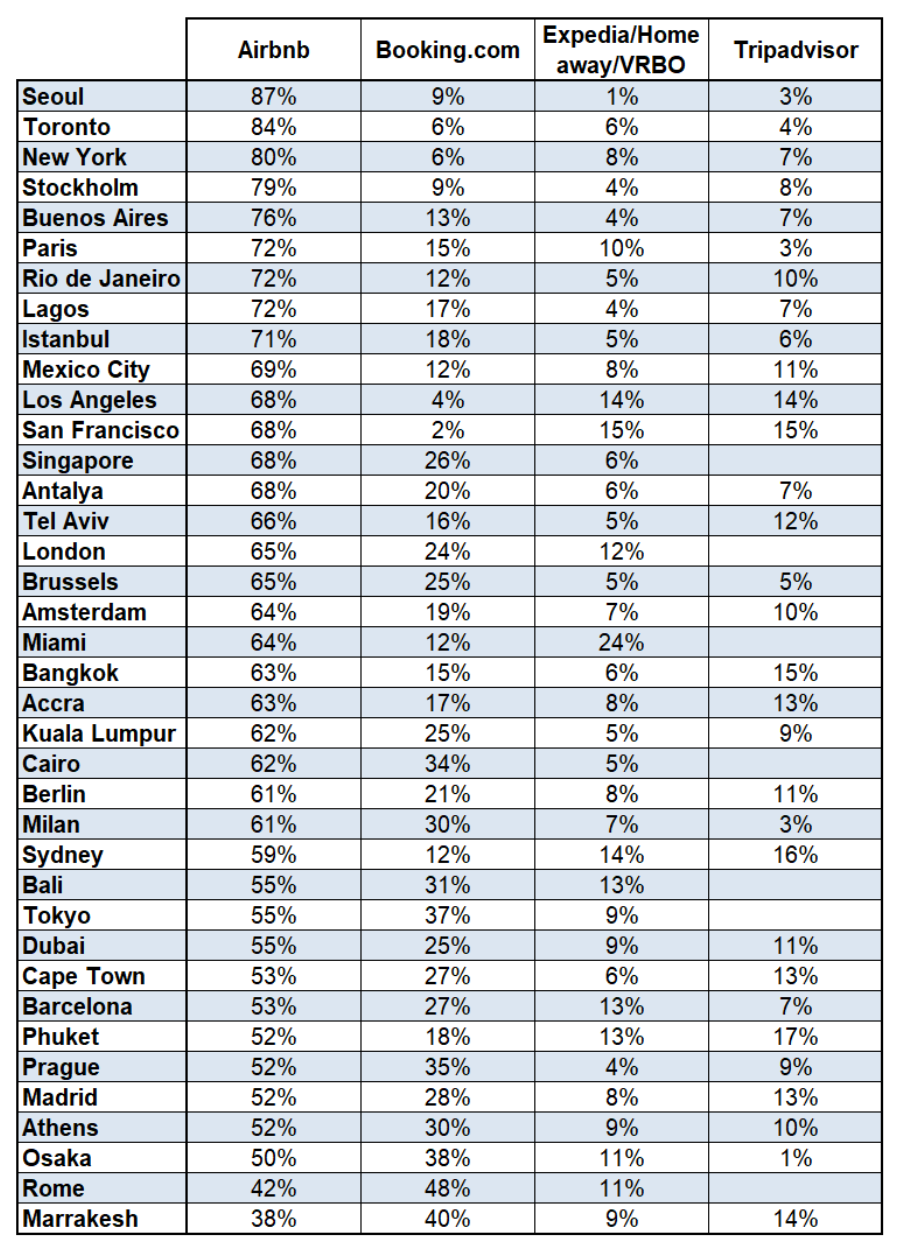

Similar picture can be observed if we look at the main touristic destinations across the world:

Nowadays there is no doubt that ABNB is the most famous and widely-used travel platform in the world.

Optionality

As explained in previous paragraphs, ABNB is an innovative company steadily creating new products. During the pandemic period the Company reorganized its priorities and focused in its core business, putting on hold many projects. However, now that the Company is navigating again more stable waters, it is expected those projects to resume the march.

One of those projects is Experiences. 2020 was expected to be the year for Experiences to really take off but with the pandemic “people were not comfortable gathering in person let alone meeting strangers”. But now the Company is again thinking about including this product among its main priorities and expects this to be a “big part of (their) story in 2023 and beyond, over really the next five years”.

Business travels are in a similar situation. This is a part of the business that was completely paralyzed but that ABNB thinks that now could take advantage of the new trends that have arisen during the pandemic. Despite some return to normalcy in business travels patterns, communication tools used during the pandemic have demonstrated that many of these travels can be substituted by a Zoom call, so it might be possible to never go back to pre-pandemic business travel levels. However, new business travels, although fewer, will probably imply longer stays in order to keep people personally connected. Should this is the case, this would probably benefit a company like ABNB.

Besides there are other different new dynamics created during the pandemic, like work-from-everywhere trends, that will probably keep expanding and also imply longer stays that will benefit ABNB (compared to hotels).

All these are just some examples of the huge optionality that ABNB presents. Should the company is able to take advantage of any of these opportunities, its addressable market will keep expanding.

Adaptability and contra-cyclicality

The travel industry is considered a consumer discretionary sector and, as part of leisure, is comprised of non-essential products and services that individuals might postpone or reduce in difficult times. However ABNB presents many characteristics that could make the Company rather resilient in case of a downturn and even contra-cyclical.

First of all, ABNB covers “nearly every type of space and nearly every type of price point”. This means that the platform offers a huge diversity of listings and prices, making possible to adapt to different budget situations. Besides, ABNB could benefit from some trade-down effect in case of a deterioration of the economic environment due to those diversified price points.

Additionally its nature of global network with operations all around the world makes ABNB also rather resilient, as in case of deterioration of some specific geographic areas, the damage could be offset (at least partially) by other outperforming regions.

Finally, ABNB is a highly adaptable business that it is able to rapidly adjust to changing consumers behaviors (e.g. urban vs suburban vs rural trips, different trip lengths, national vs cross border trips, etc.) and modify its cost structure and its organization depending on the environment (as it was demonstrated during the pandemic period).

Diversification

In close relation with the previous point, ABNB is a well-diversified business from each and every perspective. From a geographic perspective there is no doubt that ABNB is a global network with businesses all around the world and with an international focus. It has presence in 7 continents and more than 220 countries.

But it is also well-diversified looking to many other perspectives: it can provide different types of properties depending on the budget (i.e. low, mid-tier or luxury properties), or the kind of traveler (e.g. singles, families, elder people, couples), or the season (e.g. beachfront, skiing), etc. As commented in the previous paragraph, this diversified nature provides the Company with a special resilience, as in case of underperforming of some specific geographic area or market niche, the economic pressure may be offset by other outperforming regions or sectors.

Under-penetration

Despite being ABNB the clear leader in the sector, one of the most interesting points of this Company is that the short-term rental market is still rather unpenetrated. It is considered that there are more than 1.3 million homes listing in the short-term rental market in the U.S., while there are over 6 million second homes and the proportion is much lower in many other parts of the world:

And all these statistics refer only to entire homes and don’t include private rooms, other alternative accommodations or adjacent businesses.

ABNB has a lot of room to expand its global network in the areas in which they already have a deep presence (e.g. North America and Europe), as well as into those where the penetration is lower (e.g. India, Latin America, Southeast Asia).

What about the numbers?

The financial evolution of the Company is rather impressive, there is no doubt:

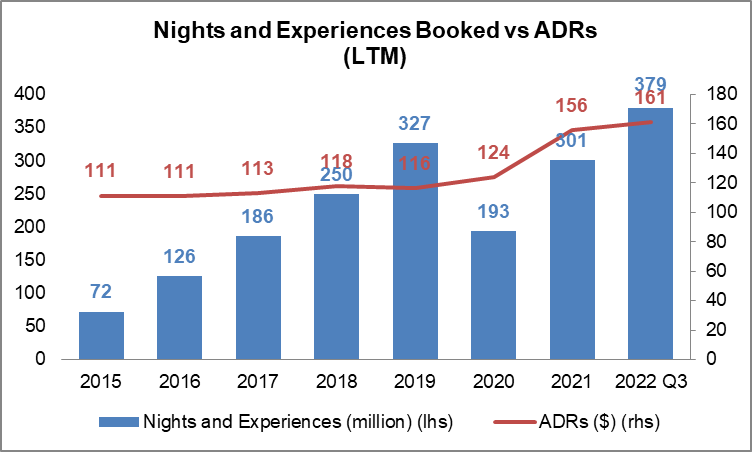

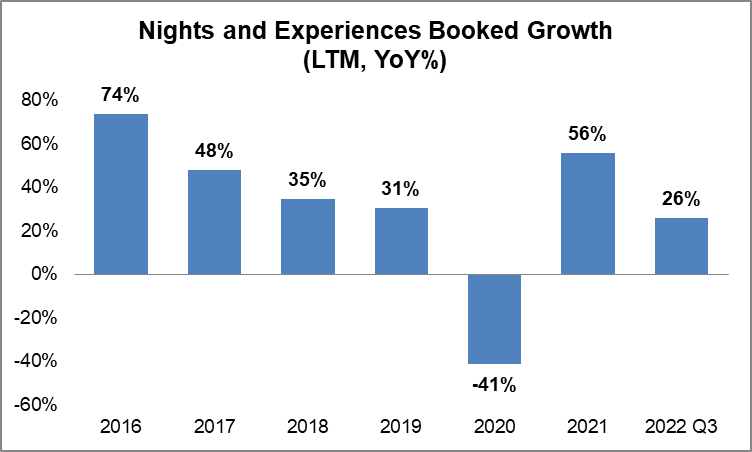

However, in order to have a better understanding of the recent performance, it is important to have a closer look at the breakdown between Nights and Experiences Booked and Average Daily Rates (ADRs):

As it can be observed, the increase in revenues during pre-pandemic years was mainly due to the astonishing increase in Nights and Experiences Booked (46% 2015-2019 CAGR), while ADRs remained rather flat (1% 2015-2019 CAGR). However, since the beginning of the “COVID-19 era”, ADRs have started to increase rapidly (13% 2019-2022Q3 CAGR) while Nights and Experiences Booked suffered an impressive decline in 2020 and finally were able to slightly overcome 2019 levels in 2022 (6% 2019-2022Q3 CAGR). Besides during all this period ABNB service fees has remained relatively flat (as % of booking value).

While the Company is expected to keep thriving in the future, as the COVID-19 recedes it would also be expected some ADRs reversion to the previous trend as a consequence of lower inflationary pressures and changes in the business mix (i.e. reopen of cross-border markets with lower ADRs) (see Valuation paragraph below). Additionally, as the business matures, the growth of Nights and Experiences Booked will probably moderate. Indeed this tendency was already in place before the pandemic period:

These two effects combined could mean a headwind in the short term. However, once ADRs stabilize, the steady increase of Nights and Experiences Booked, albeit with lower growth rates, will probably keep the company growing in the future (even without taking into account potential new products or adjacent businesses).

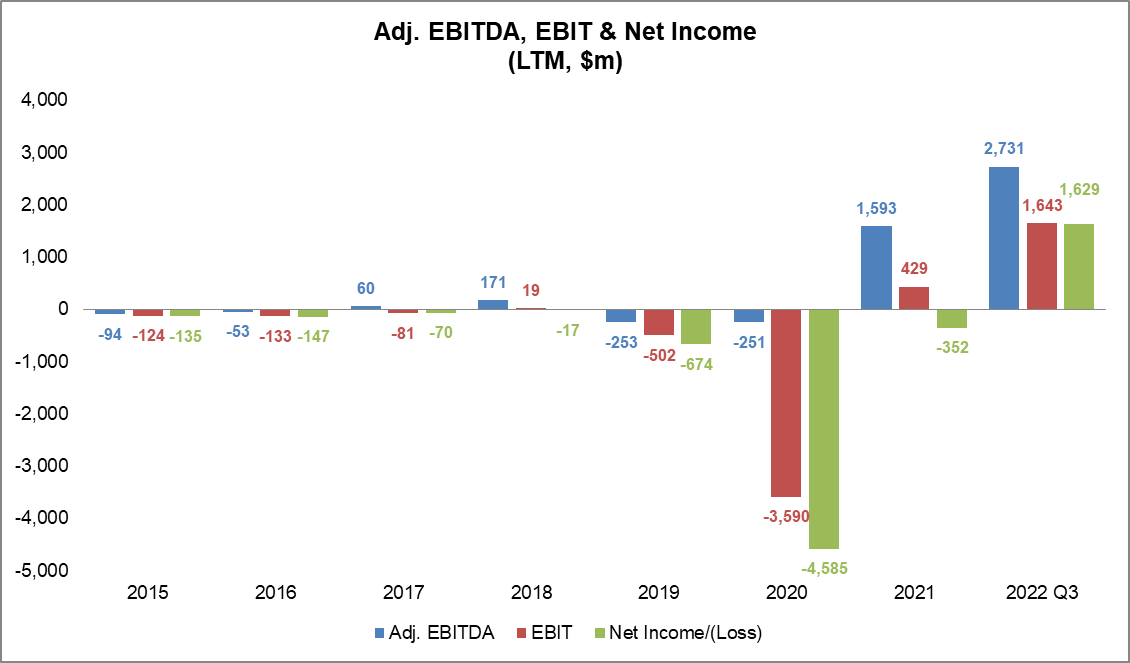

In terms of efficiency and profitability there is a clear differentiation between pre- and post-COVID periods:

During the pre-pandemic period ABNB had been gradually improving its operating leverage as the business grew. There was just some variability from period to period due mainly to product development activities and marketing expenses. That was the case of 2019 when the Company launched many new initiatives (“including our China offering, Airbnb Experiences, Airbnb Plus, hotels, and Airbnb Luxe, and platform enhancements”) and increased its marketing efforts to support this expansion.

However, with the COVID-19 impact, ABNB undertook a comprehensive review of its cost structure to align the Company with the depressed business levels and keep the organization afloat. This review materialized basically in a significant workforce reduction (~25%), the standstill of new investment projects and the elimination of almost all discretionary marketing spending. Those measures were able to stop the hemorrhage but also produced a secondary effect that will probably be much more relevant for the future: as the business started to recover, the Company realized that they were able to maintain the new cost structure. On the marketing side, it is really telling the comment made in the 2020 Q4 call: “In 2019, we had elevated spending of performance marketing. And then 2020 occurred, our business drops by 80% in eight weeks, and we pulled back all marketing, including performance marketing. But something remarkable happened. Even before we started resuming our marketing spend, our traffic levels came back to 95% of the traffic levels of 2019 without any marketing spend”. In that sense, ABNB has decided “to focus more of (their) spend on brand marketing and less on the search engine marketing”, which is more fixed (and so subject to operating leverage) and they “don't intend to ever again spend the amount of money as a percentage of revenue on marketing in the future as we did in 2019”.

In terms of employee structure, the Company carried out a complete overhaul of its organization (it wasn’t just a temporary layoff process). ABNB has “shifted from a divisional business unit structure to a functional organization and this reduced lots of duplications of functions. Instead of having multiple marketing departments, multiple product departments, multiple operations groups, (they) now have one technology group, one marketing group, one operations group, and this made (them) not only more efficient, being able to turn on a dime much more quickly”. There are some areas that will probably have to scale as the business returns to normalcy (e.g. customer service) but the Company is committed to keep a lean structure and now expects to significantly slow the growth of its employee base regardless of the economic situation (it is not a temporary decision, but a structural one).

The costs chart above (omitting 2020 that has been heavily impacted by COVID-19 and the IPO process) shows a company progressively improving its efficiency and becoming profitable:

As COVID-19 recedes and the business returns to more normal patterns it might be expected some pressure on parts of the cost structure (e.g. product development or marketing expenses) that could impact profitability levels in the short term. Indeed the Company has made rather clear that, although they are really happy with the reduction of their fixed costs and the rationalization of variable costs, they “are no in profit maximization mode”. They are really thrilled with the impressive recent margin expansion but they are committed with growth and they will continue to invest in growth. However the Company emerges from this COVID-19 period stronger and much more resilient, and there is no specific hints that invites to think that they will not achieve their longer term EBITDA margins target of 30%+.

Risks

Regulatory risks

Since the very beginning ABNB has been struggling with state and local regulations that try to restrict the short-term rental activity. Hotels, homeowners, local communities and neighborhood associations have been claiming the potential problems that this activity could bring: illegal listings, less affordable housing, rising prices or excessive tourism flows.

However, also from the start, ABNB has demonstrated being capable of negotiating with those authorities and with different stakeholders in order to reach agreements and look for compromise solutions. Its approach to regulation is perfectly defined by Jonathan Golden, former ABNB Director of Product: “Regulation serves a purpose. Startups must work with regulators to help define new policy structures, and governments must be open to innovation. It’s a two-way street, and everyone wins when we work together”.

Anyway it is important to be aware of any new regulation aimed at limiting the short-term rental activity, as those could have a relevant and structural impact on the Company. However, it is also important to highlight the economic relevance of ABNB for the local communities, especially for those communities outside the most touristic areas, and for the tax authorities, with ABNB’s tax collection and tax reporting activities. Taking into account this importance, the most probable scenario might be a balanced approach with the adoption of new regulations but also with participation of and agreements with ABNB and its peers.

Competition

There is a lot of competition within the sector: online travel agencies (OTAs), hotels, internet platforms, search engines, meta-search websites… and indeed there are no real obstacles for hosts to list their properties in different platforms.

However ABNB possesses many features that convert them in a very special platform and the preferred one for individual hosts: it is focused on them (“of those 4 million hosts, 90% are individuals”); its brand awareness is huge; it has global reach; its platform is really easy to use; it provides unmatched insurance protection; and guarantees a trustful and safety experience. This uniqueness makes them to be rather protected from the competition and almost a category of one.

Economic environment

As we mentioned in previous paragraphs, as part of the consumer discretionary sector, the travel industry is rather cyclical and dependent on the economic environment. However, as it has been also commented, ABNB possesses many features that make the Company resilient and adaptable.

There is no doubt that in case of a recession the Company will suffer, but there are some intrinsic characteristics that could help to offset an economic downturn.

Disintermediation

ABNB is a marketplace and as such it could be subject of disintermediation: hosts and guests could find a way of directly communicate and eliminate the need to use the platform. This is a real risk affecting every platform or intermediary, but in the case of ABNB it seems rather improbable (at least nowadays).

The main reason for this risk not to be a critical risk for ABNB is basically because this company provides a service that it is rather difficult to replace. Due to the kind of ABNB’s customer base and its way of travelling, the interaction through the platform seems to be the most efficient way to connect. As previously commented, ABNB is mainly composed of individual hosts, frequently making cross-border travelling, and so it is rather difficult for guests to communicate with them outside the platform. It’s completely different from the hotel experience, where it is rather easy to look for the telephone number and communicate directly with them (which is the case of the OTAs). In that sense, there are currently no specific hints of a near-term disintermediation.

Valuation

The more I read about ABNB, the more I like the company and its management, and I do expect to have the opportunity to own this company in the future. However there are two main issues that deter me from jumping right now into the Company: the lack of clearer visibility about the near future and the Company’s current valuation.

With regard to the lack of clearer visibility I’m mainly referring to the visibility in relation with valuation issues. I do believe that this Company will probably lead the travel sector in the long run and will probably keep growing in the future, gaining market share and expanding its addressable market. The problem is that this pandemic period has seriously distorted the travel industry, making rather difficult to establish a clear baseline and so to make estimations and meaningful valuations. In the case of ABNB, ADRs are far from their historical trends, some markets are still under pandemic circumstances or pending to recover (e.g. China or APAC) and it is rather unclear how different “pandemic behaviors” will evolve in the future (e.g. work-from-home, business travel, urban vs suburban vs rural travelling, etc.). Besides we are also under the sword of Damocles of falling into a recessionary period. All these issues make rather difficult to establish a starting point for a meaningful valuation and make advisable to expand the margin of safety.

However, let’s try to carry out a rather simple exercise in order to have at least a reference point. Look at the following matrix:

This matrix provides a static view of different EV/EBITDA multiples for different combinations of stock prices and ADRs. This model considers that probably, among the key metrics affecting ABNB, ADRs are the ones that might be further away from their historical trend and could return to more normalized levels. Other metrics might remain more stable or at least take advantage of offsetting factors (e.g. potential reductions of nights booked in some areas could be offset by increases in other areas; service fees will probably remain unchanged; new cost structure might also persist, etc.) and this is the reason to use ADRs as the variable for the model.

Additionally, in order to choose an appropriate multiple, we have to take into account that ABNB is the leader in its sector, with room to keep growing its core business and also with a lot of optionality. In that sense it would be expected this Company to trade at high-quality-company multiples and we could consider as interesting entry points those from 20x down (in green within the chart). Why 20x? I have just taken as reference the 10-year average of Booking Holdings ($BKNG), which is 25x, and applied a 20% haircut in order to take into account the lack of visibility in the current environment (commented at the beginning of this paragraph). In that sense, should we consider that ADRs could remain stable or even increase, the current valuation of 17.4x EV/EBITDA might be considered an interesting entry point.

However, with regard to ADRs’ recent increase, according to ABNB “about two-thirds of that increase has been price appreciation and about a third due to mix”. In that sense, within the current environment, the appreciation related with inflationary pressures could be considered as stickier, unless we enter into a deflationary period. But the business mix will probably return gradually to more balanced levels and so its impact on ADRs is expected to vanish. So if we take the difference between the current ADR (~$160) and the one at the end of 2019 (~$116) we could think that a normalized ADR, after adjusting for the business mix impact, might be in the range of $140-$150. At those ADRs levels, the Company would be trading above 20x, which I consider too high under the current scenario, as we are just taking into account a partial reduction on ADRs. The many uncertainties in the current environment suggest being much more conservative and in that sense, from a valuation perspective, I would start to be interested in this company at stock prices below $75 and even around to IPO prices ($68) to be much comfortable.

In summary, although this is a rather simplified exercise, it can provide an overview about why, due to the distortions introduced by the COVID19 and the uncertainties of the current environment, I think actual trading levels are in my opinion still expensive or at least don’t provide enough protection, and which price levels I consider could make the Company start to be interesting from a valuation perspective.

Conclusion

As explained throughout this article, ABNB is a resilient and adaptable company that has already demonstrated that is capable of thriving in different economic environments, that it is steadily innovating and improving the hosting experience, that is capable of providing profitability at scale and that is emerging stronger from the pandemic period. There is no doubt that we are in front of a unique company that will probably keep growing in the future, gaining market share and expanding its addressable market.

The problem is that the pandemic period has completely distorted the travel industry and this situation makes rather difficult to make a meaningful valuation. This circumstance, together with the uncertainties of the current environment, invites to be especially cautious and to increase the margin of safety.

Anyway, I’ve tried to carry out a simplified exercise in order to value the Company under more normalized KPI levels and my conclusion is that current trading levels are still expensive, so I will keep the Company in the watchlist until levels around the IPO price ($68).

I am very intrigued by Airbnb as well, both for the business model and its culture, but I still struggle to fully capture its dynamics and valuation.

Great article, thanks for sharing!