A Lot To Like About Good Times Restaurants ($GTIM)

A Lot To Like About Good Times Restaurants ($GTIM)

Summary

After years of unprofitable growth, GTIM changed its strategy and was starting an inflection point just before the pandemic began.

During the pandemic GTIM halted its growth projections, but it was able to navigate this period rather well and profitably, and seems to emerge stronger and thinking again about growth.

GTIM is now a profitable company, generating positive EBITDA and FCF, more efficient and with a strong balance sheet.

Some risks require close monitoring (pandemic evolution; tight labor market;commodity/food inflation) but nowadays don’t seem significant enough to derail future expectations.

The stock has rallied since the pandemic trough, but the Company seems to be still rather undervalued (at 5x EV/EBITDA) compared to its peers.

Introduction

Good Times Restaurants Inc. (GTIM) is a restaurant chain that “owns, operates, franchises and/or licenses Good Times Burgers & Frozen Custard and Bad Daddy's Burger Bar restaurants”. These are two different but complementary restaurant concepts:

Good Times Burgers & Frozen Custard is a regional chain of QSRs located primarily in Colorado. There are 24 company-owned Good Times restaurants and 8 franchised/licensed ones (in Colorado, North Carolina, South Carolina and Wyoming).

Bad Daddy's Burger Bar is a full service and more upscale restaurant concept “featuring a chef driven menu of gourmet signature burgers, chopped salads, appetizers and sandwiches with a full bar and featuring a selection of local craft microbrew beers in a high energy atmosphere that appeals to a broad consumer base”. There are currently 37 company-owned Bad Daddy’s restaurants spread across 7 states (Alabama, Colorado, Georgia, North Carolina, Oklahoma, South Carolina and Tennessee) and 2 more franchised/licensed.

The Company started in 1987 just with its Good Times Burgers brand. In 2013 they purchased 48% of Bad Daddy’s and by early 2015 they acquired the remaining 52% to complete the acquisition. Since then the Company started to rapidly develop this Bad Daddy's brand, increasing the company-owned restaurants of this brand from 2 in 2014 to 31 by the end of 2018.

However the Company was unable to grow profitably and by the end of 2018 they decided to reassess its strategy and to reduce its development profile as they sought to stabilize its margins and improve its financial position, together with the appointment of a new CEO in mid-2019. The market didn’t applaud this lower-growth decision and since then the stock has been penalized until the trough of the COVID-19 crisis.

However all these relevant changes carried out during the last years are starting to bear fruits and to prove its new strategy to be correct. Indeed it has navigated this pandemic rather well and profitable, and seems to be emerging stronger and thinking again about growth. However, despite the recent ramp up in the stock price since pandemic lows, the market is not giving the Company the same credit as to its peers and it still appears to remain rather undervalued. All in all there are a lot of things to like about this company.

Key positive points

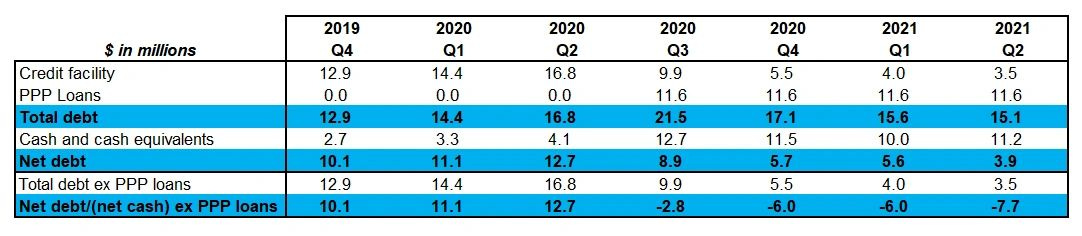

GTIM has been deleveraging and strengthening its balance sheet

As commented above, since 2019 the Company has changed its focus: “our high level organizational focus has temporarily shifted from restaurant growth to stabilization of margins, with the intent to drive earnings growth by improving restaurant level performance at our existing Bad Daddy's and Good Times” (Q4 2019 earnings call). The Company decided to temporarily slow down its growth to improve its margins within its existing restaurants. Additionally in later calls, as it is the case of Q2 2020 one, the Company mentioned that they “expect development to be in a more modest pace out of existing cash flow to maintain a strong balance sheet and to ensure (their) operation teams are not underlie stressed and lose focus on excellent operations in (their) existing restaurants”.

All of this has materialized in a steady reduction of its debt levels and interest expenses (specifically the ones related with its credit facility), and a commitment to further reduce leverage.

Source: Forms 10-Q and 10-K

As it can be observed, GTIM would be currently in a net cash position (assuming PPP loans forgiveness) of $7.7 million (or approximately 15% of its market cap).

GTIM has recently resumed its growth plans and has a lot of room to growth

Despite reducing its growth pace in the last years, the Company is committed to keep growing. Its idea is “to finance future development primarily from cash flow generated by the business” (Q1 2021 earnings call) and at this stage this means opening at least 2 restaurants per year (this is the current plan for fiscal years 2021 and 2022).

As they have stated in the last 10-K forms, they are focused in the “unit growth of company-operated Bad Daddy’s Burger Bar restaurants” and they “do not have explicit plans to develop additional Good Times restaurants, as (they) continue to refine the economic model of (their) primarily drive-thru business”. However, the growth pace is stabilizing and balance sheet improvement and FCF generation might accelerate this rhythm in the future. Besides, after the good performance of its Good Times Burgers brand during the pandemic period and its 10-K mention to the “refinement of the economic model”, I would not discard them to resume the growth also on this brand in the future (but this is just a guess, as until now they have only mentioned the intention of growing Bad Daddy’s brand).

GTIM has been improving its two brands during the pandemic and its numbers are promising

During the pandemic the Company has been able to be profitable (ex impairment charges), to generate strong FCF and, as commented above, to delever and reinforce its balance sheet. Additionally it has continued working on operational efficiencies and it will probably emerge from this crisis much more efficient.

Source: Forms 10-Q and 10-K, Company's earnings releases

Last quarters’ numbers might be slightly distorted by this unprecedented period but there are many signs that invite to optimism and to think that the Company might continue with its inflection point (that seemed to have started just before the pandemic):

Its Bad Daddy’s brand has been hit hard during this period, being much more exposed to indoor dining restrictions. However, it was able to be profitable at restaurant level thanks to outdoor dining, deliveries, menu engineering, cost reductions and operational efficiencies. These first months of (gradually) reopening Bad Daddy’s restaurants are experiencing a strong recovery.

Good Times Burgers brand has been able to take advantage of its drive-thru capabilities and it has outperformed during the whole pandemic. The good news is that this brand “continues to post impressive sales in spite of reduced pandemic-related restrictions and increased consumer confidence in on-premise dining, which (they) attribute to improved awareness generated during the pandemic, and (their) laser-focus on accuracy and speed of service”, according to one of the Company’s last press releases.

GTIM has been dealing with high labor costs during the last years and it is probably better prepared to deal with the current labor market situation than some of its peers.

Its main market, Colorado, is one of the most expensive markets in terms of labor costs. In that sense the Company is used to deal with this kind of environment and in recent quarters has been working on labor productivity (staffing for volume; focus on speed of execution; reduction of management staffing levels; lowering multi-unit supervision costs through greater spans of control). The Company is expected to be able to overcome these labor-cost issues in a better way than other peers working in more favorable States.

GTIM restaurants are loved by their customers

Customers’ reviews are something to take always with a grain of salt, but in general terms Good Times Restaurants receive really great comments by its customers and specifically its Bad Daddy’s brand. Customers tend to praise the quality and freshness of its food which in the end is the most relevant aspect of a restaurant chain.

Main risks/uncertainties

Tight labor market

This is the main risk the Company faces (together with all the companies within the sector and within many other industries). In the last call the Company specifically mentioned that “the labor market has become very tight” and that they “do see some level of margin compression in future quarters as (they) adjust pay and provide incentives to remain competitive, while at the same time, providing meaningful roles and development opportunities for all of (their) employees”. The company expects these competitive pressures to stay during the following months.

The relevance of this risk resides also in the possibility of becoming a structural change for the industry. Indeed some companies are announcing movements on this direction with wage increases (e.g. Amazon, McDonalds). Besides this situation could additionally trigger some regulatory changes in order to increase minimum wage (specifically taking into account the current US Federal Administration's political color).

However many experts foresee that this might be a temporary risk as once COVID-specific unemployment benefits start to cease, pressure on labor markets should lower. Besides, as mentioned previously, the Company has been already working in a very tight labor environment during the last years so it is expected to lever its expertise and keep making the Company more efficient.

Commodity/food inflation

This is another relevant risk. Within this inflationary and supply-chain-disruptive environment it is certainly possible to have some food pricing increase. Indeed in the Q1 2021 call the Company specifically mentioned that they “anticipate some commodity pressures later in the year”. But again the acceleration in inflation might be also transitory and the short-term effect of the combination of reopening, stimulus packages and supply-chain issues. Once we have recovered a more normal situation, some (or hopefully all) of this pressure should take down.

Lower-than-expected growth

The company has communicated that is resuming its growth with the opening of 2 new restaurants in fiscal year 2021 and at least 2 more in fiscal year 2022. However there are some uncertainties that could delay its expectations, as for instance: resurgence/evolution of the pandemic; non-forgiveness of PPP loans; difficulties to find appropriate new locations... It is not expected this uncertainties to materialize but these are for sure contingencies to closely monitor. In case the Company reduces its growth projections again, the market would surely penalize it.

Valuation

In order to have an idea about the potential undervaluation of this Company, let’s have a look from two different perspectives: market valuations and market transactions.

Peers’ market valuations

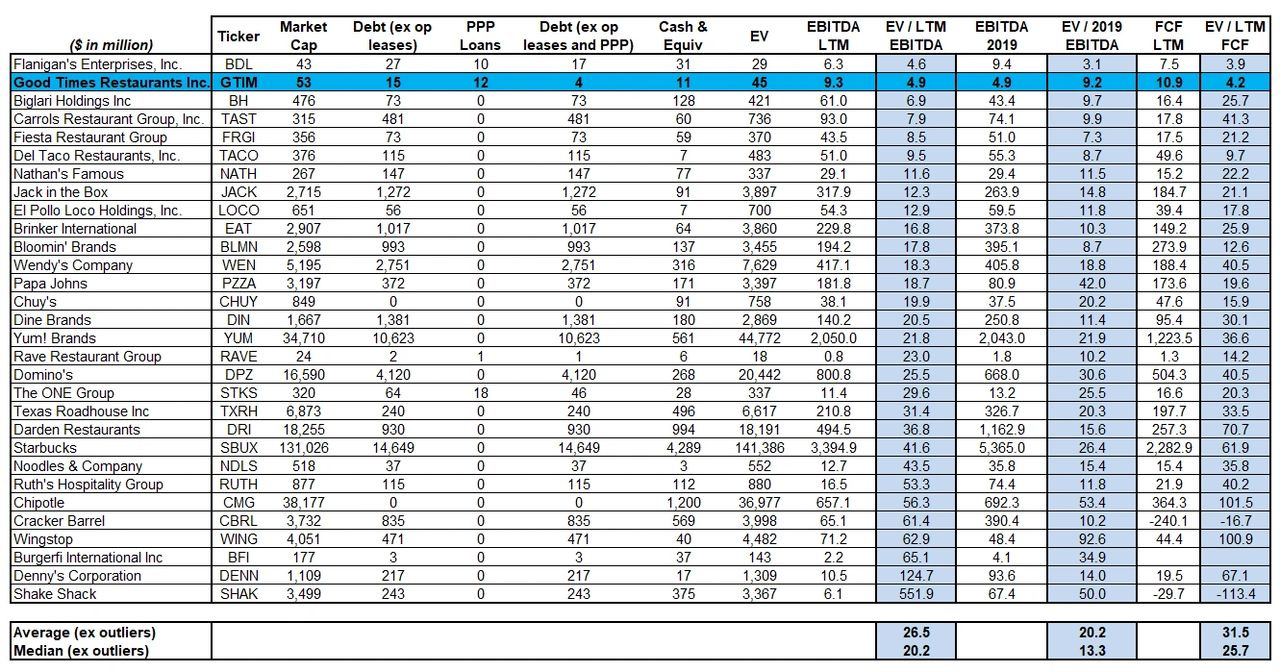

How is the market valuing GTIM’s peers? Let’s check the current valuations within the restaurant public-companies space:

Source: Forms 10-Q, forms 10-K and Seeking Alpha; companies with negative EBITDA are excluded; "outliers" means EBITDA multiple > 100.

This restaurants public-companies space comprises many players with different business models and geographic scopes. In order to refine the peers group let’s just keep those restaurant chains that mainly operate company-owned restaurants (i.e. at least half of the restaurants are owned by the company and not franchised/licensed) which might be better compared with GTIM's business model:

Source: Forms 10-Q, forms 10-K and Seeking Alpha; companies with negative EBITDA trading multiples are excluded; "outliers" means EBITDA multiple > 100.

The picture is rather similar in both cases but even more favorable using this last more-refined version.

As it can be observed, there is just only one restaurant chain that appears better placed in the list than GTIM: Flanigan’s (BDL). However Flanigan’s might not be considered a relevant peer and its multiples might be misleading due to the specificities of its situation (i.e. complicated ownership structure, related party transactions and huge illiquidity).

Anyway it seems pretty clear that, despite the recent stock-price performance of GTIM, the market is not given the Company the valuation that, in my opinion, deserves and this is probably because GTIM is a tiny company and absolutely under the radar (indeed there were no analysts and/or questions in some of the last earnings calls!).

Market transactions

Let’s have a look now at recent market transactions in the restaurant industry in order to have a flavor about what has happened in the M&A market. These are some of the most recent and relevant operations:

Goldman Sachs's majority stake acquisition of Zaxby's for a multiple of 18x to 20x EBITDA in 2020

Inspire Brands buys out Dunkin' Brands in 2020 for an estimated 18.5x 2019 EBITDA

Yum! Brands buys The Habit Restaurants in early 2020 for 9x EBITDA

Catterton acquires Del Frisco’s in 2019 for an estimated 13.3x EBITDA

Let’s also observe the figures provided by some of the companies working in this M&A field in relation to the multiples paid in the recent years:

Besides, it is important to mention that, in the case of GTIM, the analysis of market transactions gains importance as the possibility of being acquired or taken private is specifically probable. During the last year its two main shareholders have been steadily buying new shares (open-market transactions) and one of them (Mr. Jobson) is known for making bids to bring companies private. This situation, together with its probable undervaluation, makes GTIM a good candidate to participate in a M&A process.

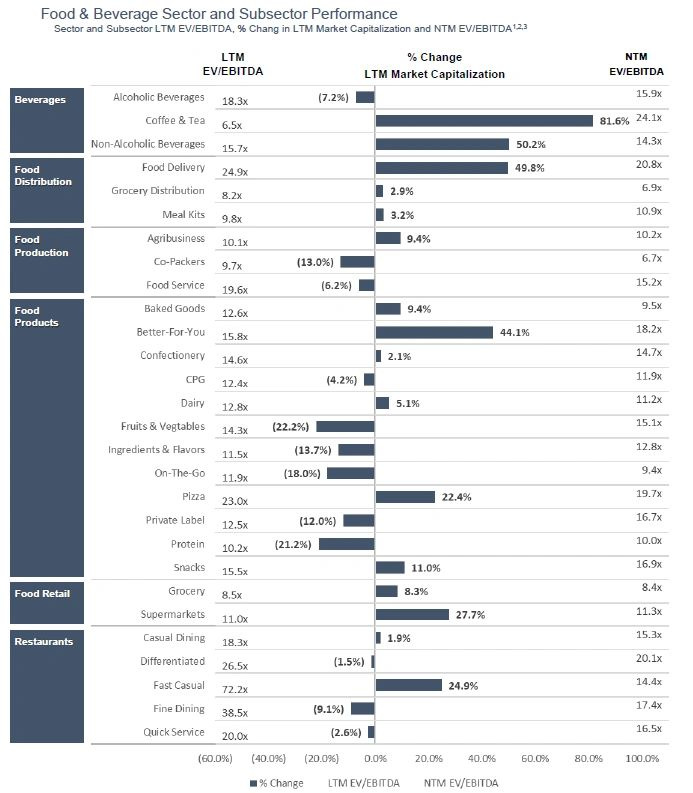

In general terms, there is a lot of variance depending on the kind of restaurant, being probably the most relevant multiples for GTIM the ones related to fast and mass casual. However what seems again pretty clear is that the Company (with a current 5x EV/EBITDA) is undervalued regardless of the multiple we compare with.

GTIM's valuation

There are two relevant issues here: one the one hand, if the company will be able to keep its current earnings levels; and on the other hand, what could we consider as a reasonable and sufficiently conservative multiple.

In terms of earnings levels, lets start with the current FCF/EBITDA levels of around $10 million. Would be reasonable to think that this could be GTIM minimum level in the foreseeable future? There are some specific issues that might put pressure on earnings levels in the near future (many of them previously commented): tighter labor costs; (front-of-house) staff brought back to normal levels; commodity/food inflation; potential lower activity in Good Times Burgers brand (in case of being unable to keep pandemic levels); tax burden increase (just in terms of FCF, not EBITDA levels) as currently the Company enjoys net operating loss carry-forwards; etc.

However, there are many other issues that will probably more than offset those potential hurdles:

It is expected a strong recovery in its Bad Daddy’s brand (it is important to recall that in the end this $10 million FCF/EBITDA that we are assuming are pandemic numbers!).

First hints from Good Times Burgers brand's post-pandemic behavior are encouraging.

The Company is opening 2 restaurants in the next 4 months and 2 more during the next fiscal year, and its idea is to keep growing in line with FCF strengthening.

Interest expenses will reduce as the Company keeps its deleveraging strategy (just in terms of FCF, not EBITDA levels)

All in all it could be considered rather conservative to assume that the company will be able to keep this FCF/EBITDA levels.

So now what could be a reasonable and sufficiently conservative multiple? After checking the current market valuations of its peers and the recent market transactions, I would be rather comfortable with a minimum 10x valuation. This valuation is well below market valuations (even using 2019 EBITDA numbers) and in line with market transactions. This would mean a minimum estimated EV of $100 million and an upside of above 100% in a rather conservative scenario (taking into account its current EV of $45 million ex PPP loans).

Conclusion

After years of unprofitable growth, GTIM reassessed and changed its strategy and indeed it seemed to be starting an inflection point just before the pandemic began.

During the pandemic the Company halted its growth projections, but it was able to navigate this period rather well and profitably (and much better than many of its peers).

GTIM is now a profitable company, generating positive EBITDA and FCF, and with a strong balance sheet. Indeed the Company emerges stronger, more efficient and thinking again about its future growth, and, more importantly, even though stock price’s strong performance since the pandemic trough, it seems to be still rather undervalued compared with its peers.

Of course there are some risks that will require closely monitoring (e.g. pandemic evolution; tight labor market; commodity/food inflation) but nowadays they don’t seem significant enough to derail future expectations.